Telecom Analytics Market Size and Growth Forecast 2026-2030

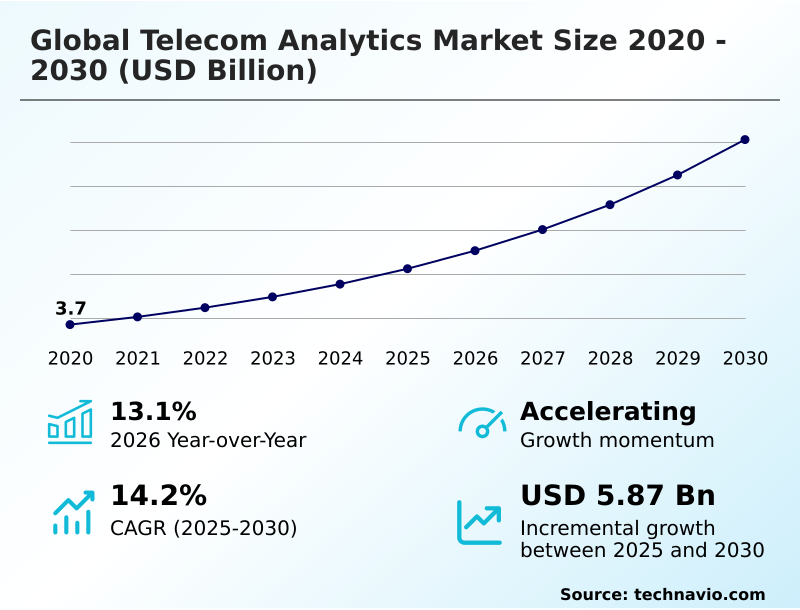

The Telecom Analytics Market size was valued at USD 6.24 billion in 2025 growing at a CAGR of 14.2% during the forecast period 2026-2030.

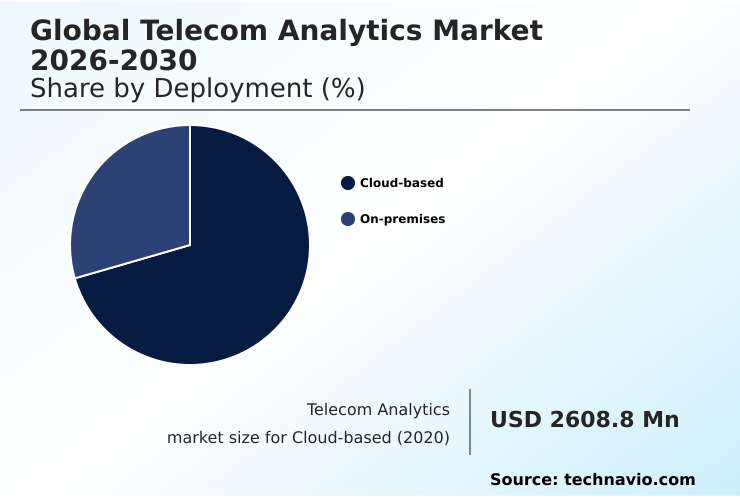

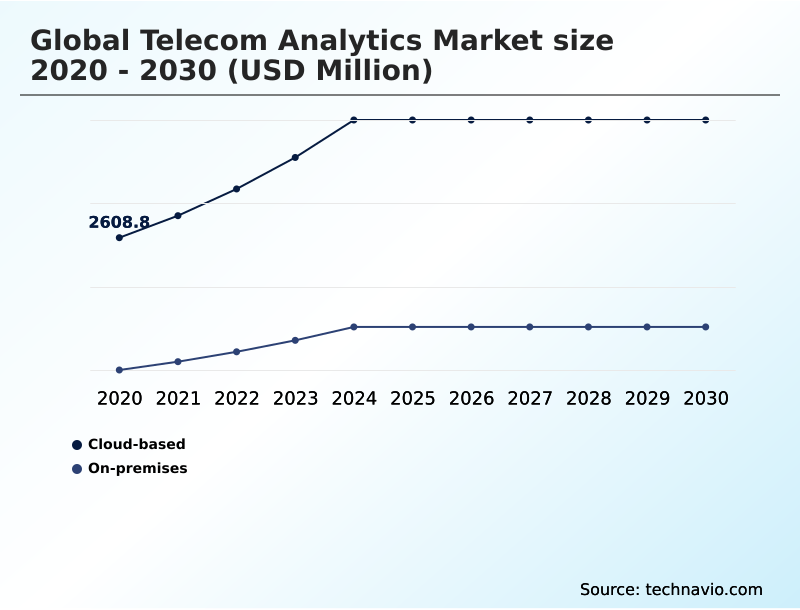

APAC accounts for 36.9% of incremental growth during the forecast period. The Cloud-based segment by Deployment was valued at USD 3.96 billion in 2024, while the Customer management segment holds the largest revenue share by Application.

The market is projected to grow by USD 8.41 billion from 2020 to 2030, with USD 5.87 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Telecom Analytics Market Overview

The telecom analytics market is defined by the strategic imperative for communication service providers to manage network complexity and enhance customer value. The proliferation of 5G infrastructure drives an immense volume of network telemetry data, making advanced analytics essential for functions like network performance management and autonomous network orchestration. A dominant trend is the adoption of cloud-based telecom analytics platforms, which offer the scalability needed for real-time data processing and AI-driven customer experience management. APAC is a key region, contributing nearly 37% of the incremental growth, fueled by rapid 5G deployment. For instance, a tier-one operator implementing predictive analytics for telecom churn can reduce subscriber attrition by proactively identifying at-risk accounts through behavior analysis. This involves leveraging big data platforms to analyze call detail records and usage patterns, enabling targeted retention campaigns. However, operators face challenges in ensuring data governance and compliance with regulations like GDPR, which affects how subscriber data is used for network optimization and fraud detection. Successfully navigating these dynamics through a unified data fabric is critical for achieving a high return on infrastructure investments.

Drivers, Trends, and Challenges in the Telecom Analytics Market

The strategic implementation of telecom analytics is reshaping operator business models, moving beyond basic connectivity to value-added services. The ability to perform real-time network traffic analysis is foundational for managing the complexities of 5G, where dynamic resource allocation is essential.

For instance, a key operational scenario is 5G network slice performance monitoring, which allows carriers to guarantee quality of service for enterprise clients in manufacturing or logistics, a segment with significantly higher revenue potential than consumer mobile broadband. Success hinges on AI-driven customer experience management, which leverages subscriber data to personalize offerings and reduce churn.

This is directly linked to optimizing RAN with machine learning, a practice that can improve network efficiency by over 15% compared to static configurations. Cloud-based telecom analytics platforms are becoming the standard for deployment, offering the scalability required for these intensive computational tasks. However, all telecom data monetization strategies must be executed within strict regulatory boundaries.

For example, compliance analytics for telecom data is a non-negotiable requirement under frameworks like GDPR, governing how personal information is used. This has driven the adoption of advanced techniques for automating network operations with AI, ensuring that efficiency gains do not compromise privacy.

Ultimately, the market's trajectory is defined by the successful application of predictive analytics for telecom churn and the development of secure, efficient platforms.

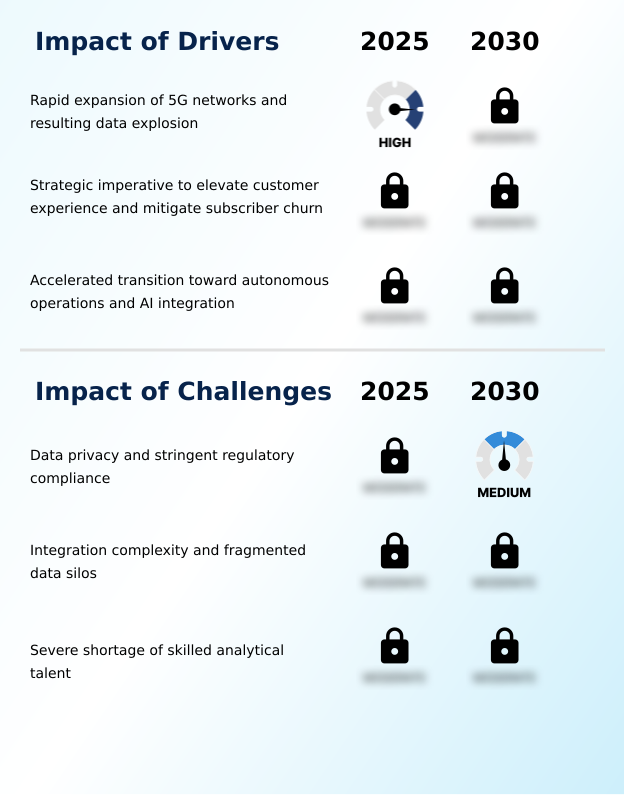

Primary Growth Driver: The rapid expansion of 5G networks and the resulting data explosion are key drivers for the adoption of advanced telecom analytics solutions.

The inexorable expansion of 5G networks and the corresponding explosion in data volume are the primary drivers of the market.

With networks becoming exponentially more complex, traditional management tools are inadequate, compelling operators to adopt advanced analytics for network performance management. The year-over-year market growth of over 13% reflects this urgency.

Communication service providers are investing in big data platforms capable of ingesting and analyzing network telemetry data in real-time to enable predictive maintenance and prevent service degradation.

Furthermore, the strategic imperative to improve customer experience and reduce churn is a powerful catalyst.

Analytics focused on subscriber behavior and quality of service are critical for retaining customers in competitive markets, making investment in these platforms a strategic necessity for sustainable revenue.

Emerging Market Trend: A key market trend is the shift toward edge analytics to process data closer to the source. This supports the ultra-low latency required for advanced applications like IoT and autonomous systems.

A primary trend is the decentralization of analytical processing power toward the network edge. This shift to edge analytics is driven by the need to support ultra-low latency applications, such as industrial IoT and autonomous systems, where real-time data processing is critical.

Rather than backhauling massive data volumes to a central cloud, operators are deploying AI and machine learning models at base stations and local data centers. This approach facilitates instantaneous anomaly detection and autonomous network orchestration, which are essential for maintaining service level agreements.

The customer management segment, which accounts for the largest share of applications at over 35%, benefits significantly, as localized processing enables faster, more responsive personalization and proactive support. This architectural evolution is fundamental for operators to monetize new 5G use cases.

Key Industry Challenge: Navigating data privacy concerns and stringent regulatory compliance frameworks presents a significant challenge to market growth.

A formidable challenge confronting the market is the intersection of data privacy and stringent regulatory compliance. As operators collect vast amounts of sensitive subscriber behavior data for analytics, they must navigate a complex web of regulations like GDPR and CCPA.

Adherence to these data governance frameworks requires significant investment in technologies for data anonymization and security, which can add computational overhead and slow down real-time data processing. The challenge is amplified by the fact that the risk and compliance management application segment is growing rapidly.

A single data breach can lead to severe financial penalties and irreparable reputational damage, creating a constant tension between maximizing data utility for subscriber churn prediction and ensuring foolproof privacy protection, which can divert resources from core network innovation.

Explore Full Market Dynamics Analysis Request Free Sample

Telecom Analytics Market Segmentation

The telecom analytics industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Deployment Segment Analysis

The cloud-based segment is estimated to witness significant growth during the forecast period.

The cloud-based deployment model is central to the telecom analytics market, driven by the operational necessity for scalable and agile solutions.

Communication service providers are shifting from on-premises infrastructure to leverage cloud environments for real-time data processing and to manage the complexities of 5G network analytics.

This transition supports advanced functions like subscriber churn prediction and autonomous network orchestration, which are essential for competitive differentiation.

The inherent flexibility of cloud-native architecture allows for the seamless integration of AI and machine learning algorithms, facilitating predictive maintenance and enhancing network performance management.

This segment, representing over 70% of deployments, relies on a unified data fabric to monetize massive data volumes from IoT ecosystems while maintaining service level agreement compliance.

The Cloud-based segment was valued at USD 3.96 billion in 2024 and showed a gradual increase during the forecast period.

Telecom Analytics Market by Region: APAC Leads with 36.9% Growth Share

APAC is estimated to contribute 36.9% to the growth of the global market during the forecast period.

The geographic landscape of the telecom analytics market is diverse, with regional adoption patterns reflecting technological maturity and investment priorities.

North America, accounting for over 30% of the market, is characterized by advanced deployments of AI-driven customer experience management and predictive maintenance to manage highly saturated markets.

In contrast, APAC is the fastest-growing region, projected to contribute nearly 37% of the market's incremental growth, driven by massive 5G network analytics rollouts and a focus on data monetization strategies in countries like China and India.

In Europe, the emphasis is on regulatory compliance, with GDPR shaping data governance frameworks for any subscriber behavior analysis. This necessitates robust solutions for data anonymization and security within big data platforms.

The Middle East and Africa show strong growth potential, with investments in network optimization and service assurance to support expanding digital economies.

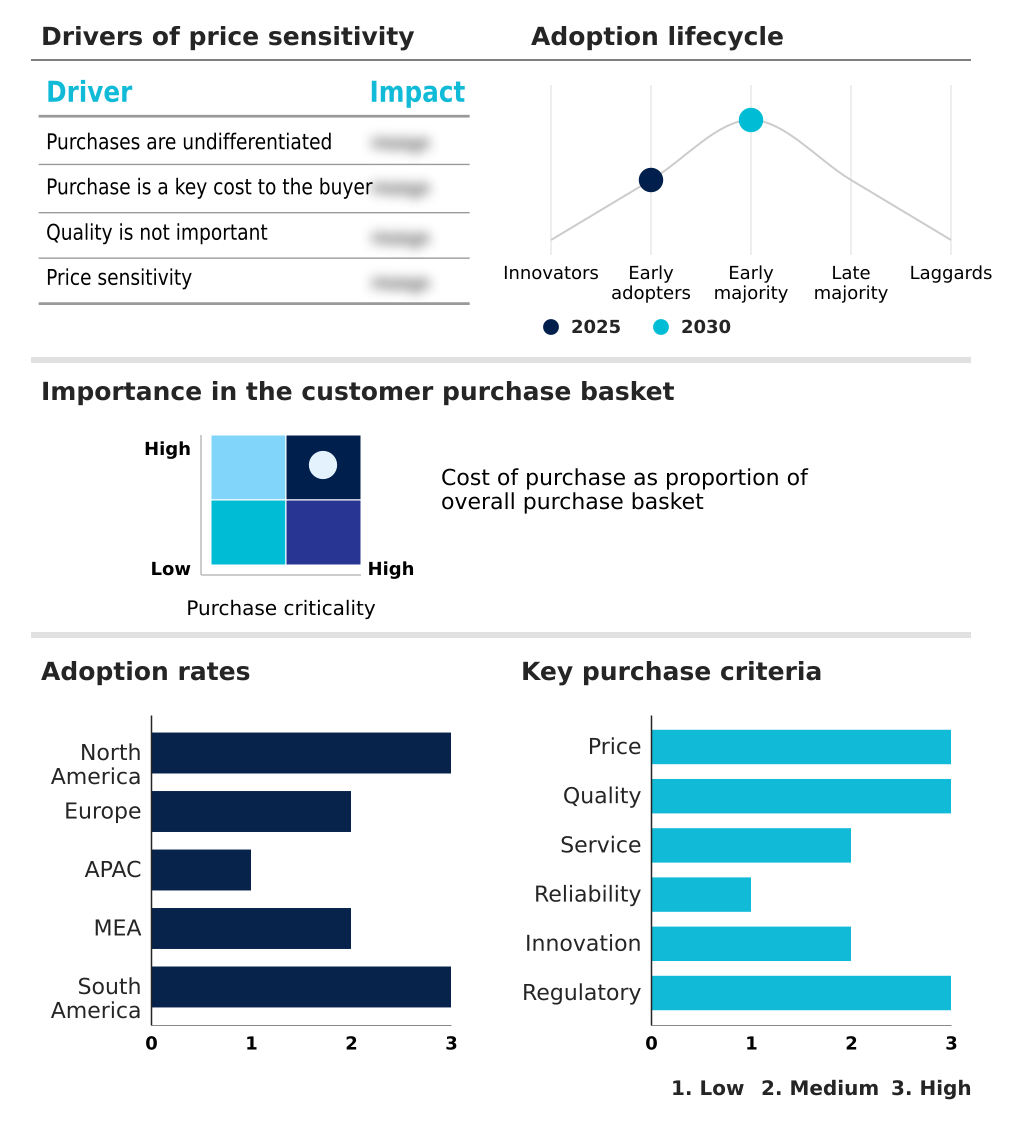

Customer Landscape Analysis for the Telecom Analytics Market

The telecom analytics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the telecom analytics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Telecom Analytics Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the telecom analytics market industry.

Adobe Inc. - Providers deliver analytics platforms for network optimization, customer experience management, and data monetization, leveraging AI-driven insights for modern telecommunication infrastructures.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adobe Inc.

- Alteryx Inc.

- Cisco Systems Inc.

- Huawei Technologies Co. Ltd.

- IBM Corp.

- Idera Inc.

- Macrometa Corp.

- Microsoft Corp.

- Nokia Corp.

- Oracle Corp.

- Panorama Software Inc.

- QlikTech International AB

- SAP SE

- SAS Institute Inc.

- Sisense Ltd.

- Tableau Software LLC

- Telefonaktiebolaget Ericsson

- Teradata Corp.

- Thales Group

- TIBCO Software Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Telecom Analytics Market

- In February 2025, Amdocs and Google Cloud announced a collaboration to launch the Amdocs Network AIOps solution, which utilizes generative AI and advanced data query platforms to help telecommunications providers automate network operations.

- In March 2025, Adobe introduced updated Adobe Experience Cloud solutions with enhanced telecom analytics capabilities, enabling communication service providers to unify disconnected workflows and improve customer journeys.

- In May 2025, Orange Business Services deployed AI-Orchestrator, a generative artificial intelligence service aimed at automating network management and resource allocation to optimize operational efficiency for enterprise clients.

- In May 2025, International Business Machines Corporation and AT&T announced an extended multi-year collaboration focused on leveraging generative AI and advanced analytics to autonomously optimize network operations and enhance customer experience.

Research Analyst Overview: Telecom Analytics Market

The operational paradigm for telecommunications is shifting toward data-centric automation, where telecom analytics serves as the core intelligence layer. The deployment of 5G network analytics is no longer a forward-looking strategy but a current operational necessity for managing network performance and enabling services like network slicing.

This has direct boardroom implications, as capital expenditure decisions for network upgrades are now intrinsically tied to the capabilities of the organization's predictive maintenance and autonomous network orchestration platforms. A critical focus area is AI-driven customer experience management, as operators in mature markets where subscriber growth has plateaued pivot to maximizing average revenue per user.

For instance, leveraging big data platforms for real-time data processing allows operators to preemptively address issues impacting quality of service, a key factor in subscriber churn prediction.

This is conducted within a tight regulatory environment, with compliance with standards like the California Consumer Privacy Act influencing the architecture of any unified data fabric and data governance framework, particularly in the cloud-based segment, which accounts for over 70% of deployments.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Telecom Analytics Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 300 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 14.2% |

| Market growth 2026-2030 | USD 5869.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 13.1% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Telecom Analytics Market: Key Questions Answered in This Report

-

What is the expected growth of the Telecom Analytics Market between 2026 and 2030?

-

The Telecom Analytics Market is expected to grow by USD 5.87 billion during 2026-2030, registering a CAGR of 14.2%. Year-over-year growth in 2026 is estimated at 13.1%%. This acceleration is shaped by rapid expansion of 5g networks and resulting data explosion, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud-based, and On-premises), Application (Customer management, Network management, Sales and marketing management, Risk and compliance management, and Workforce management), End-user (Large enterprises, and SMEs) and Geography (North America, Europe, APAC, Middle East and Africa, South America). Among these, the Cloud-based segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, Middle East and Africa and South America. APAC is estimated to contribute 36.9% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is rapid expansion of 5g networks and resulting data explosion, which is accelerating investment and industry demand. The main challenge is data privacy and stringent regulatory compliance, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Telecom Analytics Market?

-

Key vendors include Adobe Inc., Alteryx Inc., Cisco Systems Inc., Huawei Technologies Co. Ltd., IBM Corp., Idera Inc., Macrometa Corp., Microsoft Corp., Nokia Corp., Oracle Corp., Panorama Software Inc., QlikTech International AB, SAP SE, SAS Institute Inc., Sisense Ltd., Tableau Software LLC, Telefonaktiebolaget Ericsson, Teradata Corp., Thales Group and TIBCO Software Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Telecom Analytics Market Research Insights

Market dynamics are shaped by the dual pressures of technological advancement and regulatory oversight. The strategic need to elevate customer experience and mitigate churn compels investment in sophisticated analytics. Operators are deploying solutions for subscriber behavior analysis to personalize services and improve retention.

For example, in a large enterprise deployment, quality of service monitoring across a sliced 5G network is crucial for maintaining strict service level agreements, a process governed by technical standards. At the same time, adherence to data privacy mandates, such as the stringent requirements outlined in the General Data Protection Regulation, dictates the architecture of data governance frameworks.

This requires a balance between data utilization for business intelligence and strict compliance, impacting everything from network traffic analysis to customer relationship management. The on-premises segment, while smaller, remains relevant for use cases with specific data sovereignty requirements.

We can help! Our analysts can customize this telecom analytics market research report to meet your requirements.

RIA -

RIA -