Europe Solar Thermal Market Size 2026-2030

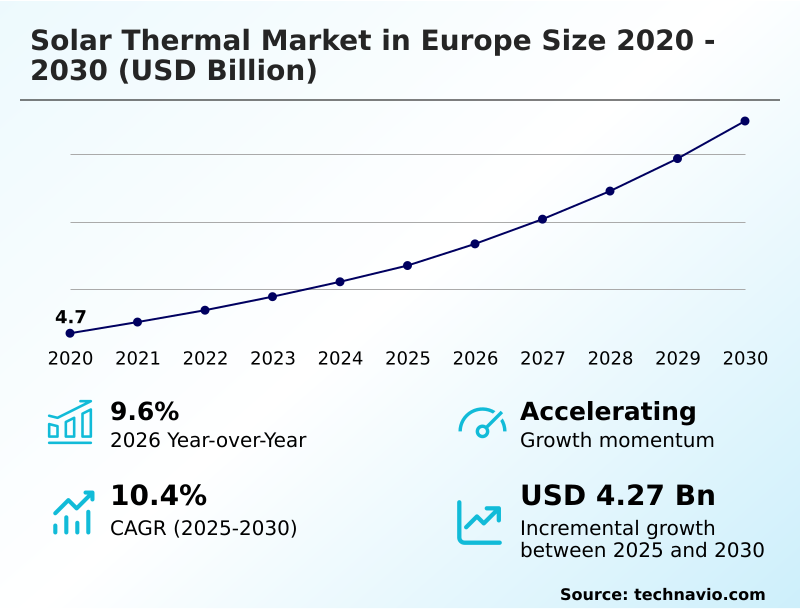

The Europe Solar Thermal Market size was valued at USD 6.70 billion in 2025, growing at a CAGR of 10.4% during the forecast period 2026-2030.

Major Market Trends & Insights

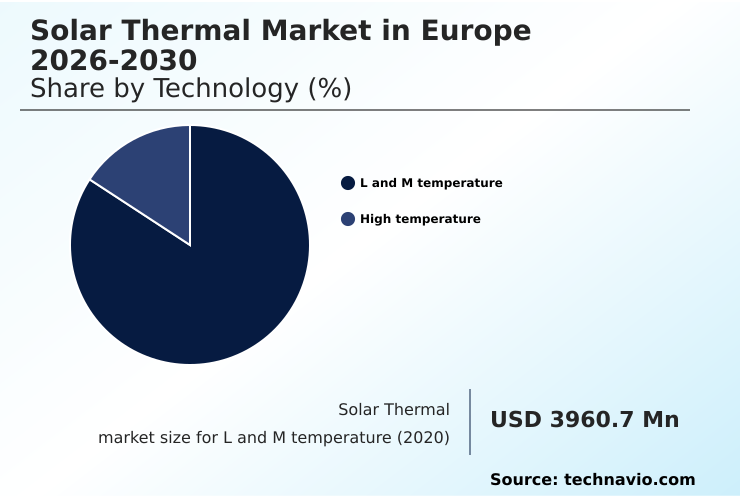

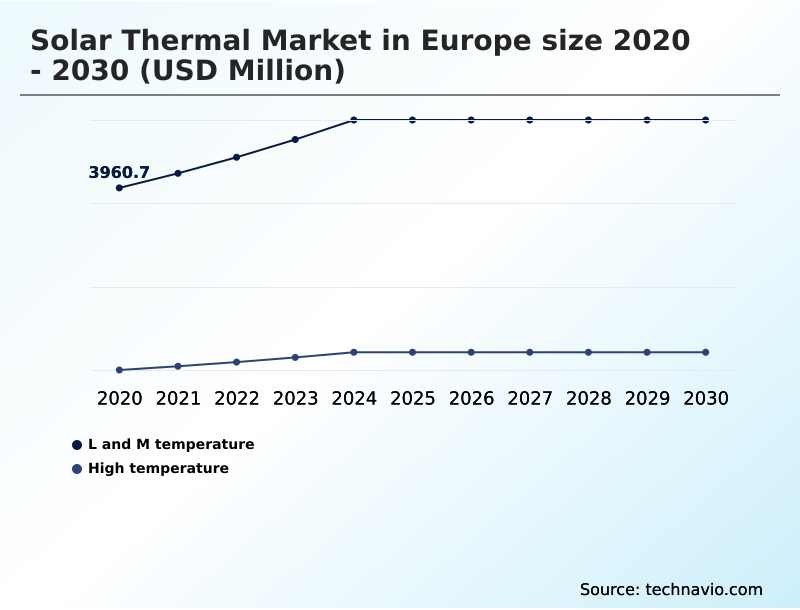

- By Technology - L and M temperature segment was valued at USD 5.16 billion in 2024

- By Application - Heat generation segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 6.27 billion

- Market Future Opportunities 2025-2030: USD 4.27 billion

- CAGR from 2025 to 2030 : 10.4%

Market Summary

- The solar thermal market in Europe is experiencing strategic realignment, with installations for district heating growing by over 15% annually, outpacing the traditional residential segment. This shift is a direct response to continent-wide decarbonization mandates that incentivize large-scale, high-impact projects.

- A key driver is the pursuit of energy security, compelling municipalities to adopt technologies that reduce reliance on volatile fossil fuel imports, thereby stabilizing long-term energy costs for consumers.

- For instance, a typical operational scenario involves a utility company integrating a large solar thermal field with seasonal thermal energy storage, reducing its natural gas consumption for district heating by up to 50%. However, the market faces a significant challenge from the lower upfront cost and perceived versatility of solar photovoltaic systems paired with heat pumps.

- This competitive pressure forces solar thermal providers to focus on applications like industrial process heat and large-scale district heating, where their high thermal efficiency offers a distinct, undeniable advantage.

What will be the Size of the Europe Solar Thermal Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Europe Solar Thermal Market Segmented?

The europe solar thermal industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Technology

- L and M temperature

- High temperature

- Application

- Heat generation

- Power generation

- Type

- Glazed collector

- Unglazed collector

- Geography

- Europe

- Germany

- Spain

- France

- Europe

How is the Europe Solar Thermal Market Segmented by Technology?

The l and m temperature segment is estimated to witness significant growth during the forecast period.

The L and M temperature segment, accounting for over 83% of the solar thermal market, is primarily driven by applications in domestic hot water and space heating.

Systems in this category, such as flat plate collectors with an average efficiency of 75%, directly address building-level decarbonization mandates. Unlike high-temperature applications, this segment’s growth is closely tied to residential and commercial construction cycles and renovation incentives.

The competitive landscape is shaped by the need for cost-effective, reliable solutions, leading to innovations like polymer based collectors and integrated solar combi-systems.

Consequently, system performance in varied climates and compatibility with hybrid heating systems are critical differentiators for manufacturers navigating this mature yet evolving market space.

The L and M temperature segment was valued at USD 5.16 billion in 2024 and showed a gradual increase during the forecast period.

What are the key Drivers, Trends, and Challenges in the Europe Solar Thermal Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the complexities of the solar thermal market in Europe requires a detailed analysis of specific applications, as a one-size-fits-all approach is no longer viable. For industrial stakeholders, the critical question is how solar thermal for industrial process heat compares to conventional energy sources.

- These systems can reduce natural gas consumption by up to 70% for low-to-medium temperature applications, offering a clear path to decarbonization and a hedge against volatile fuel prices. In the municipal sector, evaluating the large scale solar district heating cost is paramount.

- While the initial investment is higher than for individual systems, the levelized cost of heat can be 20-30% lower over the project's lifespan due to economies of scale. A frequent point of contention is the solar thermal vs heat pump efficiency debate.

- While a heat pump offers versatility, a solar thermal system boasts a much higher direct energy conversion efficiency, often exceeding 70%, making it superior for dedicated heating loads. The viability of concentrating solar power with thermal storage is also a key consideration for utility-scale projects, offering dispatchable renewable energy that enhances grid stability.

- Ultimately, success in this market depends on understanding the nuances of advanced solar collector materials innovation and selecting the right technology for the right application, moving beyond simple cost comparisons to a more holistic assessment of long-term value and energy resilience.

What are the key market drivers leading to the rise in the adoption of Europe Solar Thermal Industry?

- Supportive government policies and stringent regulatory frameworks are the most influential drivers propelling the solar thermal market in Europe.

- Supportive government policies are the primary driver for the solar thermal market in Europe, contributing to a projected year-over-year growth of 9.6%.

- Mandates such as renewable energy obligations in building codes and direct capital grants, which can cover up to 40% of installation costs, create a powerful and sustained impetus for adoption.

- This top-down approach provides the long-term investment security necessary for market expansion. This is compounded by the strategic need for energy security, as each solar thermal system directly displaces imported fossil fuels, enhancing energy resilience.

- The volatility of fossil fuel prices makes the predictable, near-zero operational cost of a solar thermal system an increasingly compelling economic proposition for both residential and commercial end-users.

- This convergence of policy, economic, and security imperatives establishes a robust foundation for market growth.

What are the market trends shaping the Europe Solar Thermal Industry?

- The solar thermal market is increasingly defined by the systemic integration of its technologies into hybrid heating systems and large-scale district heating architectures.

- A defining trend in Europe's solar thermal market is the strategic shift from standalone residential units to integrated, large-scale energy systems, with solar district heating projects showing a 15% year-over-year increase in capacity.

- This evolution is driven by the urgent need to decarbonize municipal heating networks, where large solar fields coupled with seasonal thermal energy storage can replace a significant portion of fossil fuel consumption. This integration allows for economies of scale previously unattainable, reducing the levelized cost of heat by up to 30% compared to individual systems.

- This trend impacts the value chain by prioritizing expertise in advanced system modeling and long-term heat purchase agreements over simple component sales. The expansion into solar heat for industrial processes, or SHIP, further broadens the market's scope, targeting the vast energy demands of the manufacturing sector with technologies like advanced concentrating solar thermal collectors.

What challenges does the Europe Solar Thermal Industry face during its growth?

- Intense competition from alternative renewable heating technologies, particularly PV-heat pump combinations, presents a primary challenge to the solar thermal market's growth.

- The most significant challenge for the solar thermal market is the intense competition from alternative technologies, primarily the combination of solar photovoltaics and electric heat pumps, which have seen a 50% cost reduction over the past decade. This competing solution benefits from the versatility of electricity and widespread consumer familiarity with PV panels.

- Consequently, solar thermal systems, which exclusively produce heat, are often overlooked, despite their higher thermal efficiency, which can be over 70%. Another major hurdle is the high upfront capital investment required for solar thermal installations. Although long-term operational costs are negligible, the initial financial barrier and payback periods of 5 to 10 years can deter potential customers.

- This forces the solar thermal industry to focus on applications such as large-scale district heating and industrial process heat, where its unique advantages in high-efficiency heat generation are most pronounced and economically viable.

Exclusive Technavio Analysis on Customer Landscape

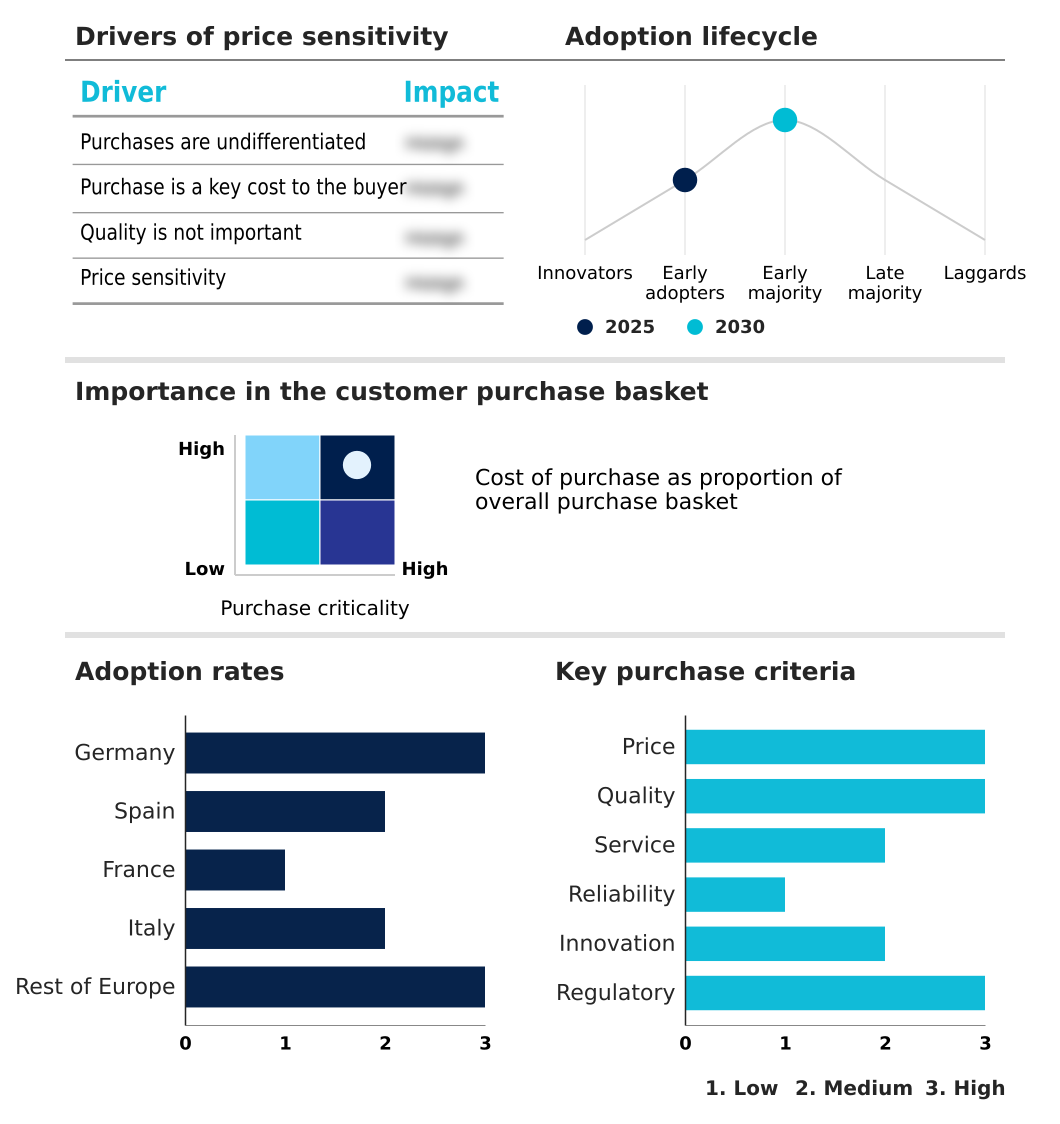

The europe solar thermal market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the europe solar thermal market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Europe Solar Thermal Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, europe solar thermal market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Absolicon Solar Collector AB - Key solutions encompass a range of technologies, including concentrated solar collectors, industrial heat systems, solar water heaters, and advanced thermal storage units designed for efficient decarbonization.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Absolicon Solar Collector AB

- Ariston Holding NV

- BDR Thermea Group

- Calpak Cicero Hellas SA

- Cosmogas Srl

- GREENoneTEC Solarindustrie

- Hewalex Sp zoo Spk

- Industrial Solar GmbH

- NES Ltd.

- Newheat

- Roth Werke GmbH

- Solar Heat Europe

- Soltigua

- TVP Solar SA

- Vaillant Group

- Viessmann Group

- Wolf GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Renewable Electricity industry, stringent policies like the Energy Performance of Buildings Directive (EPBD) mandate nearly zero energy buildings, which directly creates a non-discretionary demand for solar thermal installations to meet renewable energy obligations for heating.

- The imperative for grid stability in the Renewable Electricity industry, driven by the high penetration of intermittent sources, elevates the value of dispatchable renewable energy, creating a strategic niche for Concentrating Solar Power (CSP) plants with thermal energy storage.

- A significant push for corporate decarbonization within the broader Renewable Electricity industry has led companies to adopt on-site generation, directly boosting demand for solar thermal systems to supply industrial process heat and reduce reliance on fossil fuels.

- Across the Renewable Electricity industry, a systemic shift toward decentralized energy source models to enhance energy resilience has increased interest in building-integrated solar solutions, benefiting solar thermal as a key technology for local heat generation.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Europe Solar Thermal Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 203 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.4% |

| Market growth 2026-2030 | USD 4269.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.6% |

| Key countries | Germany, Spain, France, Italy and Rest of Europe |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The solar thermal market in Europe operates within a complex ecosystem where technology suppliers and regulatory bodies heavily influence market dynamics, with the L and M temperature segment comprising over 83% of the market. Raw material suppliers providing specialized glass and copper for flat plate collectors and evacuated tube collectors form the base of the value chain.

- Manufacturers, ranging from large heating corporations to specialized firms, depend on certification bodies like Solar Keymark to ensure product quality and market access, a process which can add up to 10% to development costs. Distribution occurs through a network of wholesalers and specialized installers whose training and expertise are critical for system performance.

- End-users, influenced by government incentives and rising energy costs, are shifting from small residential systems to larger, integrated solutions for industrial and district heating applications. This entire system is underpinned by research institutions and ESCOs that drive innovation and develop new financial models.

What are the Key Data Covered in this Europe Solar Thermal Market Research and Growth Report?

-

What is the expected growth of the Europe Solar Thermal Market between 2026 and 2030?

-

The Europe Solar Thermal Market is expected to grow by USD 4.27 billion during 2026-2030, registering a CAGR of 10.4%. Year-over-year growth in 2026 is estimated at 9.6%%. This acceleration is shaped by supportive government policies and stringent regulatory frameworks, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (L and M temperature, and High temperature), Application (Heat generation, and Power generation), Type (Glazed collector, and Unglazed collector) and Geography (Europe). Among these, the L and M temperature segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers Europe. Country-level analysis includes Germany, Spain, France, Italy and Rest of Europe, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is supportive government policies and stringent regulatory frameworks, which is accelerating investment and industry demand. The main challenge is intense competition from alternative renewable heating technologies, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Europe Solar Thermal Market?

-

Key vendors include Absolicon Solar Collector AB, Ariston Holding NV, BDR Thermea Group, Calpak Cicero Hellas SA, Cosmogas Srl, GREENoneTEC Solarindustrie, Hewalex Sp zoo Spk, Industrial Solar GmbH, NES Ltd., Newheat, Roth Werke GmbH, Solar Heat Europe, Soltigua, TVP Solar SA, Vaillant Group, Viessmann Group and Wolf GmbH. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape of the solar thermal market in Europe, which is forecast to grow at a CAGR of 10.4%, is increasingly defined by large-scale projects and strategic innovation from key vendors. Major players like the Viessmann Group are driving this trend, exemplified by the construction of Germany's third-largest solar thermal system, which will supply a local district heating network.

- Similarly, specialists such as Newheat are advancing the sector's capabilities, with projects focused on high-capacity pit thermal energy storage systems that enhance the viability of urban heating networks by over 30%. These developments reflect a market-wide pivot from smaller residential applications to complex, infrastructure-level solutions.

- This strategic shift directly addresses the urgent need for industrial and municipal decarbonization, a primary demand driver. Companies are adapting by building expertise in project financing and long-term energy service contracts.

We can help! Our analysts can customize this europe solar thermal market research report to meet your requirements.

RIA -

RIA -