Saudi Arabia Healthcare IT Market Size 2026-2030

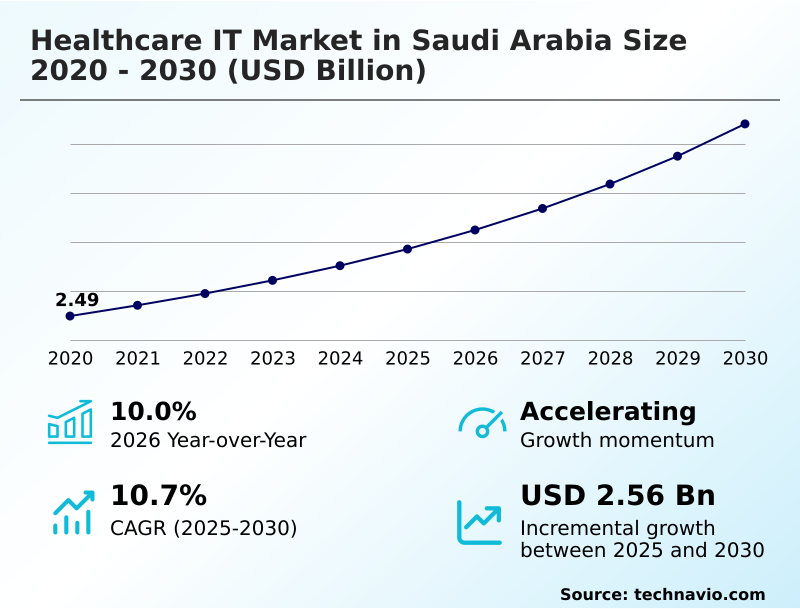

The Saudi Arabia Healthcare IT Market size was valued at USD 3.86 billion in 2025, growing at a CAGR of 10.7% during the forecast period 2026-2030.

Major Market Trends & Insights

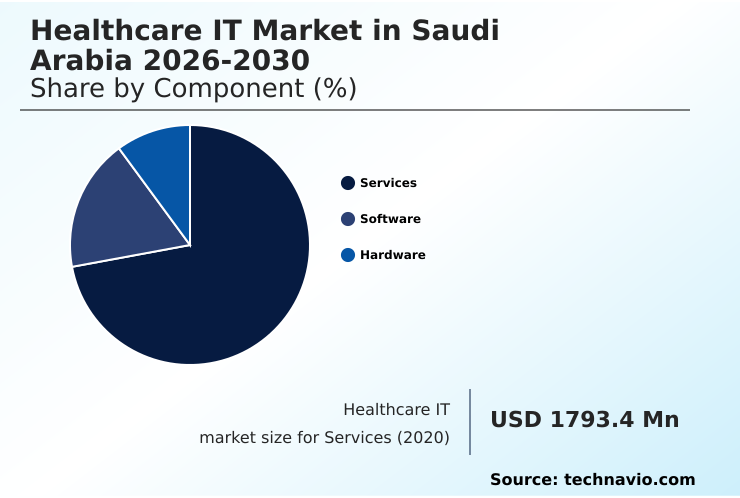

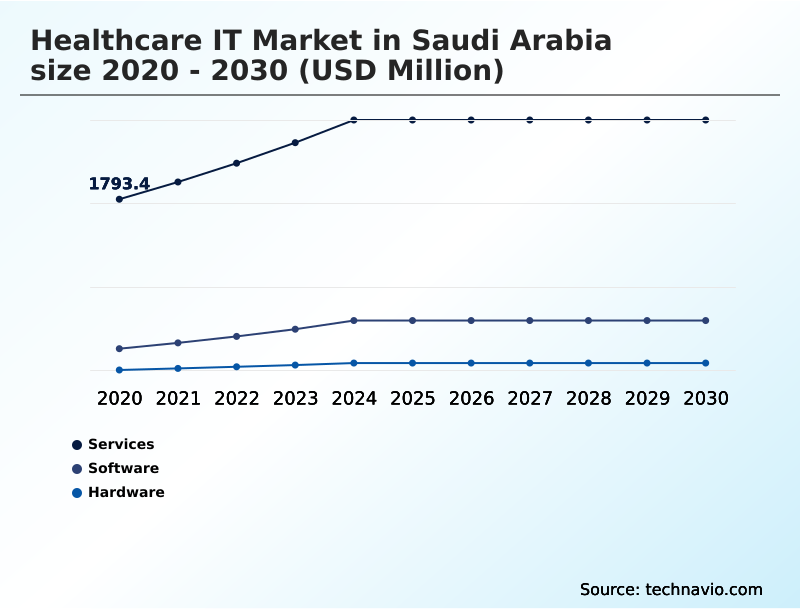

- By Component - Services segment was valued at USD 2.51 billion in 2024

- By End-user - Healthcare providers segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 3.93 billion

- Market Future Opportunities 2025-2030: USD 2.56 billion

- CAGR from 2025 to 2030 : 10.7%

Market Summary

- The healthcare IT market in Saudi Arabia is undergoing a profound structural transformation, with chronic diseases accounting for approximately 74% of all annual deaths, compelling a shift toward technology-driven care. This transition is steered by a national strategy mandating the comprehensive digitalization of patient records and integrating AI into clinical workflows to enhance efficiency and patient outcomes.

- As a result, the market has matured beyond basic electronic records to large-scale infrastructure projects supporting high-performance computing and predictive analytics, with platforms like the Sehhaty app serving over 31 million users. A key operational scenario involves using unified health data to manage hospital resources, where predictive models can forecast patient admission surges, improving bed allocation by over 20%.

- While the drive for digital transformation fuels growth, it is tempered by the formidable challenge of ensuring data security across an increasingly interconnected and fragmented data ecosystem, demanding significant investment in advanced cybersecurity measures.

What will be the Size of the Saudi Arabia Healthcare IT Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Saudi Arabia Healthcare IT Market Segmented?

The saudi arabia healthcare it industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Services

- Software

- Hardware

- End-user

- Healthcare providers

- Healthcare payers

- Method

- Acute care

- Post-acute care

- Ambulatory care

- Geography

- Middle East and Africa

- Saudi Arabia

- Middle East and Africa

How is the Saudi Arabia Healthcare IT Market Segmented by Component?

The services segment is estimated to witness significant growth during the forecast period.

The healthcare IT market in Saudi Arabia is segmented by component, with services comprising over 71% of the total market, reflecting massive investment in digital transformation.

This dominance is driven by the complexity of integrating new systems, which requires extensive professional consulting and system integration services.

The software segment, which includes cloud applications and patient flow management tools, is expanding as providers adopt more sophisticated clinical workflow automation, while the hardware segment supports this expansion.

For instance, implementing robotic process automation can increase administrative efficiency by up to 35% compared to manual processes.

End-user segmentation shows healthcare providers accounting for approximately 66% of the market as they are the primary adopters of these technologies to deliver value-based care and support the use of consumer wellness applications.

The Services segment was valued at USD 2.51 billion in 2024 and showed a gradual increase during the forecast period.

What are the key Drivers, Trends, and Challenges in the Saudi Arabia Healthcare IT Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic implementation of healthcare IT in Saudi Arabia pivots on establishing robust ehr interoperability framework standards to unify a historically fragmented data landscape. Achieving this requires a clear understanding of the clinical workflow automation impact, which promises to enhance efficiency but also necessitates significant investment in new systems and training.

- As the demand for virtual care grows, addressing telehealth infrastructure scalability requirements becomes a primary concern for providers aiming to deliver consistent service quality. Central to this digital transformation is the adherence to patient data protection law compliance, a non-negotiable factor that shapes system architecture and data governance policies.

- The industry's use of AI in medical diagnostics accuracy is another critical focus, with advanced algorithms demonstrating a 15% improvement in early detection for certain conditions compared to traditional methods. For stakeholders evaluating the healthcare it market in saudi arabia 2026-2030, success hinges on navigating these technical and regulatory complexities.

- The integration of sophisticated analytics has also been shown to reduce administrative errors by over 25%, reinforcing the financial and clinical case for accelerated technology adoption.

What are the key market drivers leading to the rise in the adoption of Saudi Arabia Healthcare IT Industry?

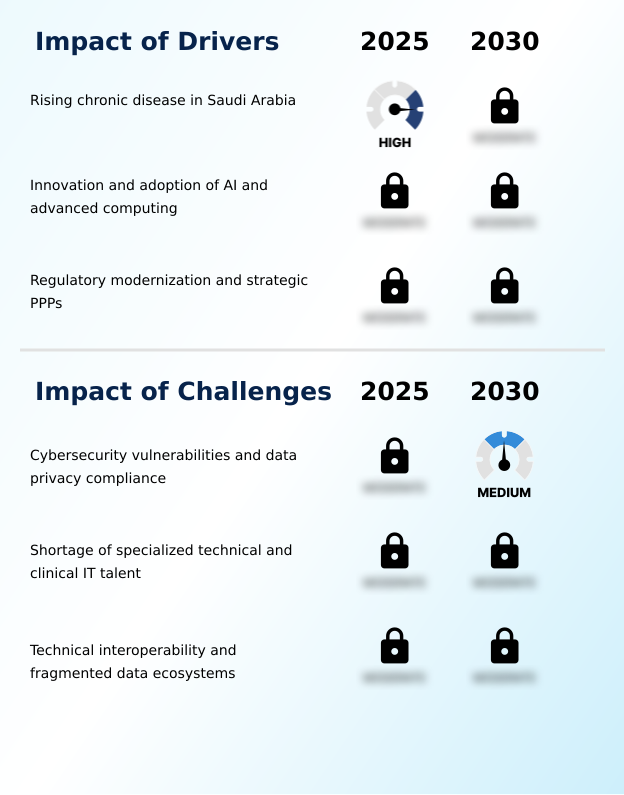

- The rising prevalence of chronic diseases in Saudi Arabia is a significant driver for the rapid adoption of sophisticated medical technologies and digital health solutions.

- The rapid adoption of sophisticated healthcare IT is primarily driven by the escalating prevalence of chronic diseases, which are responsible for approximately 74% of all deaths in Saudi Arabia.

- This public health challenge necessitates a move toward proactive population health management, leveraging advanced computing and healthcare data analytics.

- The government's 'Health in All Policies' approach and the success of platforms offering virtual consultations have accelerated the use of remote patient monitoring and clinical decision support systems.

- For example, a national predictive analytics platform now utilizes data from over 31 million users to identify at-risk individuals, enabling targeted interventions that support data-driven wellness and reduce the strain on hospital resources, demonstrating a clear cause-and-effect relationship between technology investment and public health outcomes.

What are the market trends shaping the Saudi Arabia Healthcare IT Industry?

- The mandatory integration of all healthcare providers and insurers into the National Platform for Health and Insurance Exchange Services is a key market trend, creating significant demand for interoperable software solutions.

- A primary trend shaping the market is the mandatory integration with the national health information exchange, which is driving a 40% increase in demand for cloud-based software-as-a-service (SaaS) models. This regulatory push compels healthcare providers to modernize their legacy hospital information systems to ensure digital compliance and support the creation of a unified health record.

- This shift toward national interoperability standards facilitates the proliferation of home-first care models and enhances the functionality of patient engagement platforms. Consequently, investment in scalable cloud architecture has accelerated, with providers seeking flexible solutions that can connect seamlessly to the national network, which has already completed its first phase of linking with a 95% success rate for initial participants.

What challenges does the Saudi Arabia Healthcare IT Industry face during its growth?

- Escalating cybersecurity vulnerabilities and the rigorous demands of data privacy compliance present a key challenge to the growth of the healthcare IT industry.

- The foremost challenge is navigating the dual pressures of escalating cybersecurity threats, which have seen a surge of over 40% in targeted attacks, and the rigorous demands of new data protection frameworks.

- The mandatory implementation of a national data governance platform requires significant re-engineering of legacy electronic health records to meet strict data residency and patient data privacy standards, creating a formidable barrier for smaller entities. This situation is compounded by a persistent shortage of specialized clinical IT talent capable of managing the complex cybersecurity framework.

- Failure to balance rapid technological deployment with these stringent security and data sovereignty mandates carries severe penalties, intensifying pressure on IT departments and slowing the pace of digital adoption for facilities with fragmented data ecosystems.

Exclusive Technavio Analysis on Customer Landscape

The saudi arabia healthcare it market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the saudi arabia healthcare it market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Saudi Arabia Healthcare IT Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, saudi arabia healthcare it market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture Plc - Key offerings focus on enterprise-grade software, cloud services, and integration solutions that enable digital transformation, data analytics, and enhanced patient care.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Carestream Health Inc.

- Cisco Systems Inc.

- Dell Technologies Inc.

- Epic Systems Corp.

- GE HealthCare Technologies

- Hewlett Packard Enterprise Co.

- Hyland Software Inc.

- IBM Corp.

- Infor Inc.

- InterSystems Corp.

- IQVIA Holdings Inc.

- Koninklijke Philips NV

- Microsoft Corp.

- Oracle Corp.

- Salesforce Inc.

- SAP SE

- Sectra AB

- ServiceNow Inc.

- Siemens Healthineers AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Health Care Technology industry, the strategic shift from reactive treatment to proactive, data-driven wellness and prevention is accelerating the adoption of predictive analytics platforms and AI governance frameworks within the healthcare IT market.

- The proliferation of the Internet of Healthcare Things (IoHT), including advanced wearables and remote sensors, has created a surge in demand for robust telehealth infrastructure and data sovereignty solutions to manage the influx of patient-generated data securely.

- Heightened cybersecurity risks have led to the mandatory implementation of more stringent data protection frameworks across the sector, compelling healthcare IT vendors to integrate real-time threat intelligence and advanced security features into their core offerings.

- The widespread adoption of Robotic Process Automation (RPA) and cognitive automation to streamline administrative tasks like billing and scheduling has driven demand for system integration services that can connect these automated workflows with existing clinical IT talent and fragmented data ecosystems.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Saudi Arabia Healthcare IT Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 186 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.7% |

| Market growth 2026-2030 | USD 2556.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.0% |

| Key countries | Saudi Arabia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The healthcare IT ecosystem in Saudi Arabia involves a complex interplay of stakeholders, where technology suppliers provide core platforms like electronic health records that improve data accessibility by over 60%. These solutions are implemented by system integrators and are used by healthcare providers and payers, who represent the primary end-user segments.

- Regulatory bodies mandate stringent data security and interoperability standards, shaping product development and deployment strategies. For instance, the adoption of robotic process automation for administrative tasks has been shown to reduce operational costs by up to 25%.

- This entire value chain is supported by ongoing R&D in areas like AI and data analytics, creating a dynamic environment focused on enhancing clinical outcomes and operational efficiency through technology.

What are the Key Data Covered in this Saudi Arabia Healthcare IT Market Research and Growth Report?

-

What is the expected growth of the Saudi Arabia Healthcare IT Market between 2026 and 2030?

-

The Saudi Arabia Healthcare IT Market is expected to grow by USD 2.56 billion during 2026-2030, registering a CAGR of 10.7%. Year-over-year growth in 2026 is estimated at 10.0%%. This acceleration is shaped by rising chronic disease in saudi arabia, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Services, Software, and Hardware), End-user (Healthcare providers, and Healthcare payers), Method (Acute care, Post-acute care, and Ambulatory care) and Geography (Middle East and Africa). Among these, the Services segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers Middle East and Africa. Country-level analysis includes Saudi Arabia, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is rising chronic disease in saudi arabia, which is accelerating investment and industry demand. The main challenge is cybersecurity vulnerabilities and data privacy compliance, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Saudi Arabia Healthcare IT Market?

-

Key vendors include Accenture Plc, Carestream Health Inc., Cisco Systems Inc., Dell Technologies Inc., Epic Systems Corp., GE HealthCare Technologies, Hewlett Packard Enterprise Co., Hyland Software Inc., IBM Corp., Infor Inc., InterSystems Corp., IQVIA Holdings Inc., Koninklijke Philips NV, Microsoft Corp., Oracle Corp., Salesforce Inc., SAP SE, Sectra AB, ServiceNow Inc. and Siemens Healthineers AG. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive vendor landscape is highly active, with high capex requirements shaping company strategies, where differentiation is achieved through localized partnerships and advanced AI integration rather than price alone. International entities like Oracle and Philips are aligning their software suites with the Kingdom's data residency and clinical goals.

- For instance, the deployment of an AI-driven patient flow management system aims to reduce emergency room wait times by up to 20%, showcasing the tangible impact of these technologies. Success is increasingly determined by a vendor's ability to localize global technology and contribute to the overarching objectives of the national digital health strategy.

- This environment is further shaped by the persistent challenge of recruiting and retaining specialized clinical and IT talent capable of managing these complex, large-scale systems.

We can help! Our analysts can customize this saudi arabia healthcare it market research report to meet your requirements.

RIA -

RIA -