Renewable Energy Storage For Ai Data Centers Market Size and Growth Forecast 2026-2030

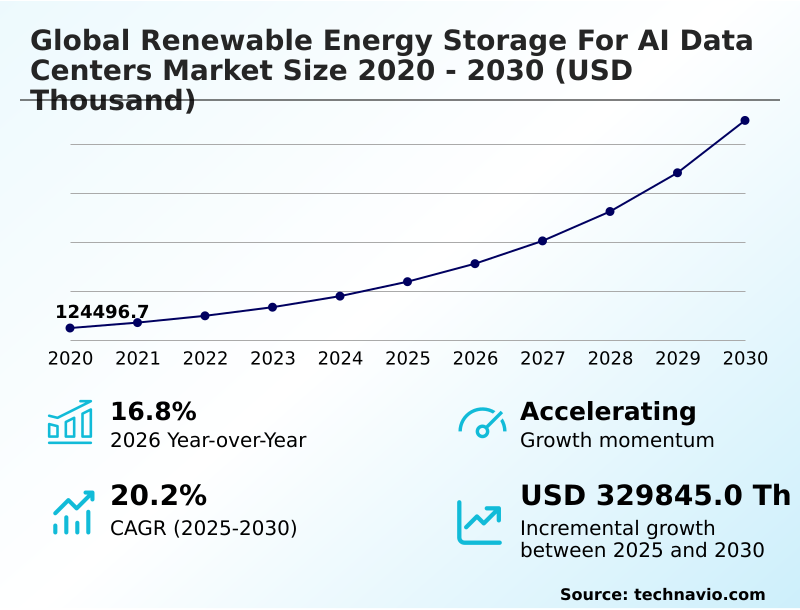

The Renewable Energy Storage For Ai Data Centers Market size was valued at USD 219.28 million in 2025 growing at a CAGR of 20.2% during the forecast period 2026-2030.

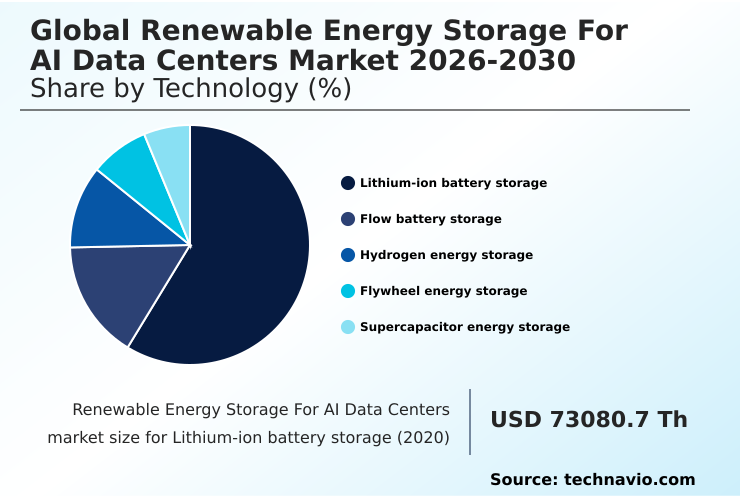

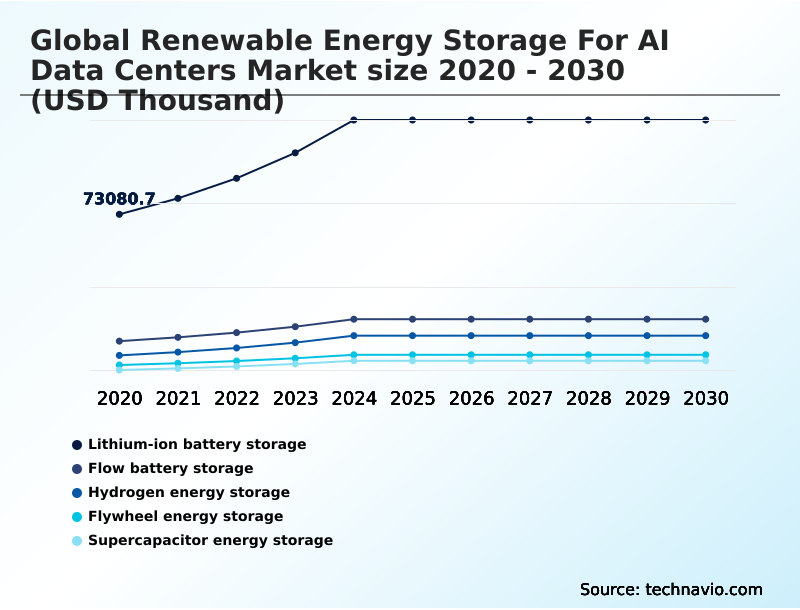

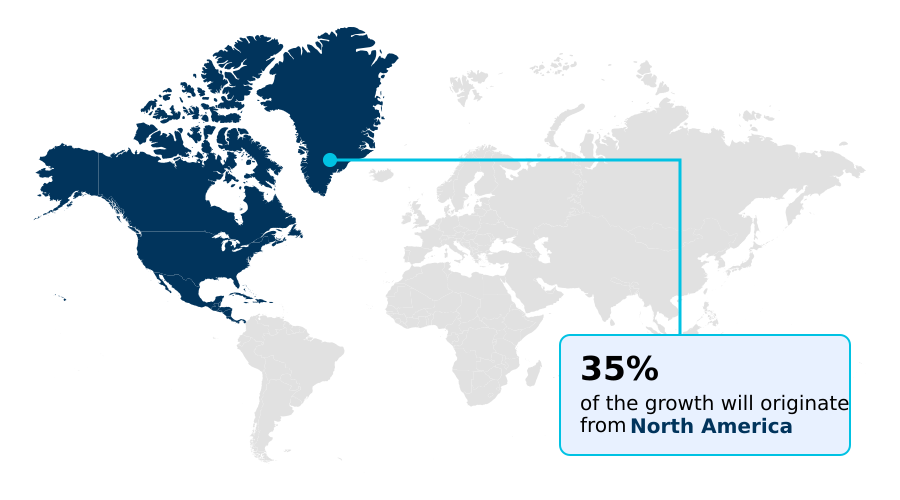

North America accounts for 34.9% of incremental growth during the forecast period. The Lithium-ion battery storage segment by Technology was valued at USD 112.65 million in 2024, while the Hyperscale data centers segment holds the largest revenue share by End-user.

The market is projected to grow by from 2020 to 2030, with USD 329.85 million of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Renewable Energy Storage For Ai Data Centers Market Overview

The renewable energy storage for AI data centers market is defined by the critical need for power resilience to support escalating computational demands. North America is set to capture over 34% of the market's incremental growth, driven by massive investments in hyperscale data center energy infrastructure. Key trends include the deployment of long-duration energy storage and AI-driven energy management to optimize costs and meet corporate sustainability goals. A typical business scenario involves a colocation facility installing a behind-the-meter battery energy storage system to perform peak shaving, reducing its electricity costs by avoiding high demand charges while offering tenants a premium for renewably-powered, uninterruptible power supply. This strategy not only lowers operational energy expenditure but also provides ancillary grid services, creating an additional revenue stream. The market's trajectory is shaped by a dual push for performance and sustainability, forcing operators to innovate beyond traditional power backup solutions toward integrated, intelligent energy hubs using solid oxide fuel cells and software-defined power.

Drivers, Trends, and Challenges in the Renewable Energy Storage For Ai Data Centers Market

Strategic deployment within the renewable energy storage for AI data centers market requires a comprehensive cost-benefit analysis of data center microgrids, moving beyond simple backup to full energy market participation. An essential first step is navigating grid interconnection for data centers, a process often hampered by multi-year queues and complex technical requirements under standards like IEEE 1547.

Once approved, the focus shifts to the hardware, with an LFP versus NMC for stationary storage decision weighing the former's safety and longevity against the latter's energy density. For instance, a hyperscale operator in a water-scarce region might select a closed-loop thermal management for containerized BESS to minimize water use, a critical factor in achieving sustainability targets.

The operational phase necessitates AI software for energy storage optimization to maximize the ROI of behind-the-meter battery storage and ensure power reliability for LLM training.

Finally, end-of-life management is governed by regulations such as the EU Battery Regulation, mandating circular economy models for data center batteries, including the assessment of second-life EV batteries for data center use, which are vital for long-term sustainability and compliance.

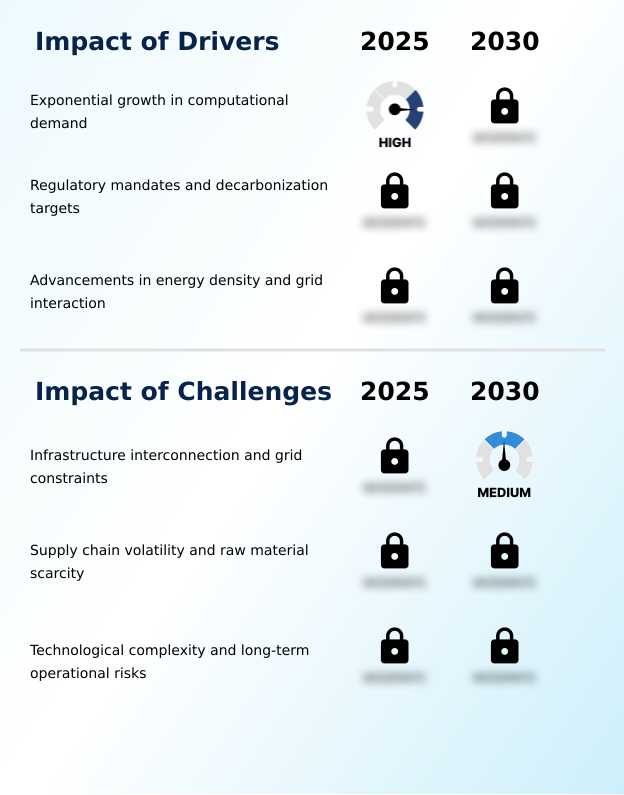

Primary Growth Driver: The exponential growth in computational demand from AI workloads is the primary driver for deploying large-scale renewable energy storage solutions to ensure power stability and sustainability.

Market growth is primarily propelled by the convergence of escalating computational demand and stringent regulatory pressures. The energy required by high-density server racks for AI workloads has surpassed the reliability of many public grids, making on-site storage a necessity.

Concurrently, mandates for Scope 2 emissions reporting are compelling operators to adopt carbon-neutral data centers, directly fueling investment in renewable storage.

Government incentives, such as tax credits under the US Inflation Reduction Act, further de-risk the capital expenditure for these systems.

This creates a strong business case for deploying storage to engage in demand response programs and secure favorable energy procurement agreements, aligning corporate sustainability goals with financial incentives and ensuring a stable power source for uninterrupted operations.

Emerging Market Trend: The integration of resilient microgrid design allows for autonomous data center resilience. This shift ensures operational continuity for high-performance computing clusters independent of regional grid failures.

Key trends are reshaping data center power architecture toward autonomous, sustainable operation. The adoption of resilient microgrid design is paramount, enabling facilities to function independently during grid outages. This is coupled with a strong push for circular economy principles, where battery lifecycle management and second-life battery applications are integrated into planning to comply with regulations like the WEEE Directive.

Simultaneously, the industry is leveraging AI-driven energy management and software-defined power to enable predictive load balancing in real time. This allows for dynamic energy arbitrage and optimization of utility-scale energy storage assets. These trends signal a move from passive power consumption to proactive, intelligent energy orchestration, ensuring data processing continuity for mission-critical AI.

Key Industry Challenge: Infrastructure interconnection queues and legacy grid constraints represent a primary challenge, creating significant bottlenecks for the deployment of large-scale renewable energy storage for AI data centers.

Significant structural challenges constrain market growth, led by grid-level and supply chain vulnerabilities. The lengthy grid interconnection queue for new storage assets remains a primary bottleneck, delaying projects for years. On the supply side, the volatile critical mineral supply chain, subject to geopolitical risks and regulations like REACH, creates uncertainty in the cost and availability of high-performance batteries.

At the facility level, managing the operational risk of large-scale battery energy storage systems, including sophisticated thermal management systems to prevent thermal runaway, adds complexity and cost. Furthermore, ensuring the cybersecurity of the battery management system is a critical, often underestimated, challenge that is vital for protecting both the asset and the data center it supports.

Explore Full Market Dynamics Analysis Request Free Sample

Renewable Energy Storage For Ai Data Centers Market Segmentation

The renewable energy storage for ai data centers industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Technology Segment Analysis

The lithium-ion battery storage segment is estimated to witness significant growth during the forecast period.

Lithium-ion battery storage technology, particularly configurations using lithium-iron-phosphate batteries, underpins the renewable energy storage for AI data centers market, accounting for nearly 60% of deployments.

Procurement decisions are driven by superior energy density metrics and established manufacturing scale, which are critical for supporting the computational workload profiles of high-density server racks.

While initial capital outlay is a key consideration, operators are increasingly focused on total cost of ownership, factoring in battery cycling degradation and round-trip efficiency over the system's lifespan.

The implementation of battery management system analytics, compliant with ISO 50001 for energy management, is essential for optimizing state of charge monitoring and extending the operational life of these critical power assets, ensuring data processing continuity.

The Lithium-ion battery storage segment was valued at USD 112.65 million in 2024 and showed a gradual increase during the forecast period.

Renewable Energy Storage For Ai Data Centers Market by Region: North America Leads with 34.9% Growth Share

North America is estimated to contribute 34.9% to the growth of the global market during the forecast period.

The geographic landscape of the renewable energy storage for AI data centers market is led by North America, which accounts for the largest share of incremental growth, driven by hyperscale data center energy demands and supportive policies like the US Inflation Reduction Act.

However, APAC is the fastest-growing region, with a projected growth rate over 21%, as nations like China and India rapidly build out digital infrastructure resilience.

In Europe, stringent regulations under the EU Green Deal compel colocation facility power providers to integrate localized power generation with storage to meet carbon-neutral mandates.

This regional divergence reflects different priorities, from pure scaling in APAC to grid harmonization and demand-side management in mature European markets, all converging on the need for robust energy infrastructure investment to power AI's future.

Customer Landscape Analysis for the Renewable Energy Storage For Ai Data Centers Market

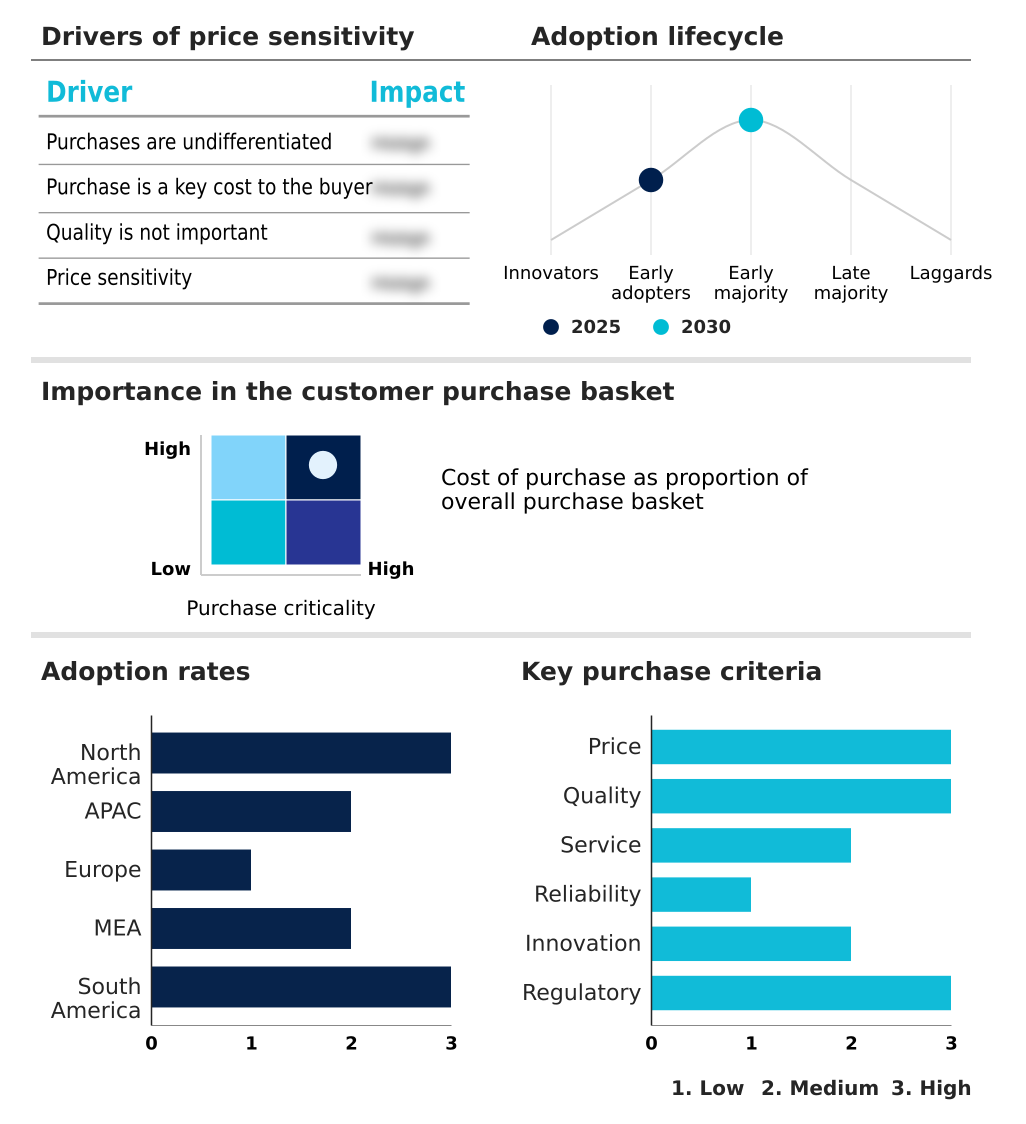

The renewable energy storage for ai data centers market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the renewable energy storage for ai data centers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Renewable Energy Storage For Ai Data Centers Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the renewable energy storage for ai data centers market industry.

ABB Ltd. - Key offerings include grid-interactive battery systems and intelligent software to ensure power quality and renewable energy reliability for critical AI data center infrastructure.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Bloom Energy Corp.

- BYD Co. Ltd.

- Contemporary Amperex Ltd.

- Eaton Corp. Plc

- Enel X Italia S.r.l.

- Fluence Energy LLC

- Generac Power Systems Inc.

- Hitachi Energy Ltd.

- Honeywell International Inc.

- Johnson Controls International

- LG Energy Solution Ltd.

- Powin Inc.

- Samsung Electronics Co. Ltd.

- Schneider Electric SE

- Siemens AG

- Stem Inc.

- Tesla Inc.

- Vertiv Holdings Co.

- Wartsila Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Renewable Energy Storage For Ai Data Centers Market

- In January 2025, Microsoft announced plans to invest USD 80 billion in AI-focused data centers designed to support its cloud platform and research partnerships, requiring extensive power infrastructure.

- In January 2025, Invenergy and Meta Platforms Inc. entered into four agreements to supply 791 megawatts of new solar and wind energy, supported by storage, to power Meta's data center operations.

- In December 2025, Alphabet Inc. announced an agreement to acquire Intersect Power for approximately USD 4.75 billion, aiming to expand the clean energy infrastructure needed to support Google's AI data centers.

- In December 2025, Google partnered with NextEra Energy to develop gigawatt-scale AI data centers powered by dedicated clean energy generation and storage to meet rising electricity demand from advanced AI.

Research Analyst Overview: Renewable Energy Storage For Ai Data Centers Market

The renewable energy storage for AI data centers market is shifting from short-duration uninterruptible power supply to long-duration energy storage solutions capable of providing multi-hour grid independence. This evolution is a direct response to the massive, sustained energy draws of AI computational workload profiles.

Boardroom decisions on infrastructure CAPEX now weigh the high upfront cost of a vanadium redox flow battery against the lifecycle and thermal runaway prevention benefits over traditional lithium-iron-phosphate batteries. We see increasing adoption of direct current coupling to improve round-trip efficiency between solar arrays and the battery energy storage system.

A key consideration for operators is the ability of the power conversion system to provide ancillary grid services like grid frequency regulation, turning a cost center into a revenue stream.

As facilities grow, ensuring black start capability and integrating advanced battery management system software for state of charge monitoring becomes critical for ensuring resilience and meeting stringent service level agreements under frameworks like Uptime Institute's Tier classifications.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Renewable Energy Storage For Ai Data Centers Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 318 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 20.2% |

| Market growth 2026-2030 | USD 329845.0 thousand |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 16.8% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, France, Italy, The Netherlands, Spain, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Renewable Energy Storage For Ai Data Centers Market: Key Questions Answered in This Report

-

What is the expected growth of the Renewable Energy Storage For Ai Data Centers Market between 2026 and 2030?

-

The Renewable Energy Storage For Ai Data Centers Market is expected to grow by USD 329.85 million during 2026-2030, registering a CAGR of 20.2%. Year-over-year growth in 2026 is estimated at 16.8%%. This acceleration is shaped by exponential growth in computational demand, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (Lithium-ion battery storage, Flow battery storage, Hydrogen energy storage, Flywheel energy storage, and Supercapacitor energy storage), End-user (Hyperscale data centers, Colocation data centers, Enterprise data centers, and Edge data centers), Source (Solar energy storage systems, Wind energy storage systems, Hydropower-based storage, and Others) and Geography (North America, APAC, Europe, Middle East and Africa, South America). Among these, the Lithium-ion battery storage segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, APAC, Europe, Middle East and Africa and South America. North America is estimated to contribute 34.9% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, France, Italy, The Netherlands, Spain, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is exponential growth in computational demand, which is accelerating investment and industry demand. The main challenge is infrastructure interconnection and grid constraints, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Renewable Energy Storage For Ai Data Centers Market?

-

Key vendors include ABB Ltd., Bloom Energy Corp., BYD Co. Ltd., Contemporary Amperex Ltd., Eaton Corp. Plc, Enel X Italia S.r.l., Fluence Energy LLC, Generac Power Systems Inc., Hitachi Energy Ltd., Honeywell International Inc., Johnson Controls International, LG Energy Solution Ltd., Powin Inc., Samsung Electronics Co. Ltd., Schneider Electric SE, Siemens AG, Stem Inc., Tesla Inc., Vertiv Holdings Co. and Wartsila Corp.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Renewable Energy Storage For Ai Data Centers Market Research Insights

Market dynamics are increasingly shaped by sophisticated energy procurement agreements and the need to manage total cost of ownership over the lifecycle of power assets. In markets like North America and Europe, operators leverage power purchase agreements to secure long-term, fixed-price renewable energy, using on-site storage to manage intermittency.

This contrasts with strategies in APAC, where the focus is on rapid deployment of modular energy storage to overcome grid instability. Across all regions, the ability to participate in energy markets and provide grid stabilization services is transforming data center power architecture from a cost center into a revenue-generating asset.

Adherence to frameworks like the Greenhouse Gas Protocol for Scope 2 emissions reporting is a non-negotiable factor in procurement decisions, directly influencing the choice of storage technology and the design of the entire data center cooling infrastructure.

We can help! Our analysts can customize this renewable energy storage for ai data centers market research report to meet your requirements.

RIA -

RIA -