Refrigerants Market Size and Growth Forecast 2026-2030

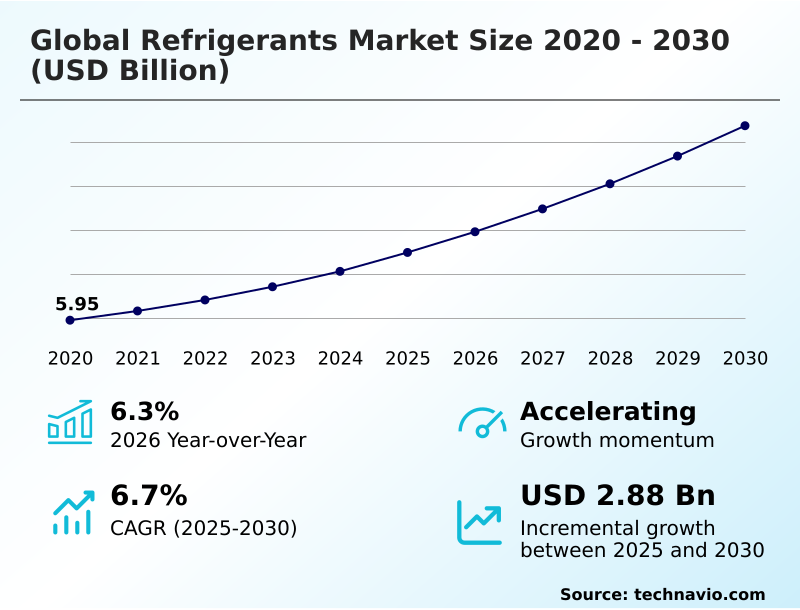

The Refrigerants Market size was valued at USD 7.49 billion in 2025 growing at a CAGR of 6.7% during the forecast period 2026-2030.

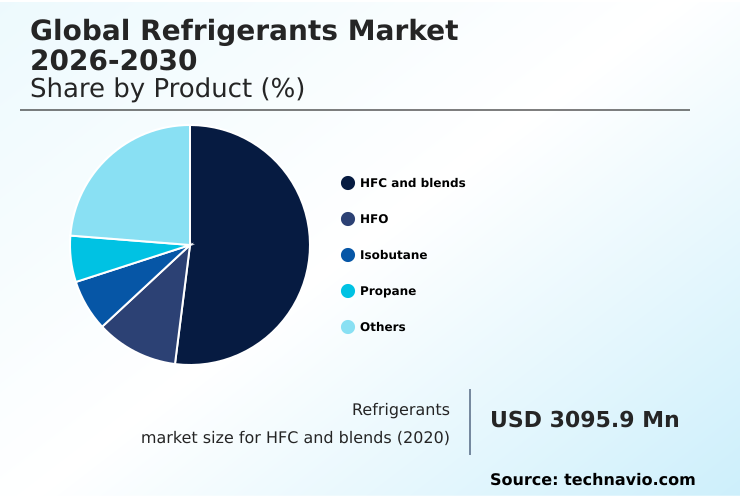

APAC accounts for 46.8% of incremental growth during the forecast period. The HFC and blends segment by Product was valued at USD 3.61 billion in 2024, while the Refrigeration system segment holds the largest revenue share by Application.

The market is projected to grow by USD 4.42 billion from 2020 to 2030, with USD 2.88 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Refrigerants Market Overview

The refrigerants market is undergoing a technology-driven transformation, compelled by global HFC phase-down schedules that mandate a shift toward low-GWP refrigerants. This transition affects the entire vapor compression cycle, impacting equipment design, lubricant compatibility, and service practices for all HVACR systems. The APAC region is central to this dynamic, contributing nearly 47% of the market's incremental growth, fueled by industrialization and the expansion of cold chain logistics. In practice, a large supermarket chain making a capital expenditure decision must now evaluate the total cost of ownership of a transcritical CO2 system against a solution using A2L refrigerants, considering factors like energy efficiency, maintenance expertise for high-pressure systems, and compliance with ASHRAE Standard 34. This choice impacts not just upfront cost but also the long-term refrigerant management plan and adherence to evolving green building standards. The focus on refrigerant reclamation and end-of-life recovery further complicates the supply chain, creating new value streams.

Drivers, Trends, and Challenges in the Refrigerants Market

Strategic decisions in the refrigerants market are increasingly governed by the HFC phase-down impact on HVAC operations and long-term asset management. For facility managers in the food retail sector, compliance with regulations like the EU F-Gas Regulation necessitates a move away from legacy systems.

The choice between technologies such as CO2 refrigeration in food retail and systems designed for propane R-290 in commercial refrigeration involves a complex analysis of capital expenditure, energy efficiency of natural refrigerants, and technician training for A2L refrigerant safety standard compliance.

For instance, while HFO-1234yf for automotive AC systems offers a GWP of less than 1, a significant improvement over its predecessor, implementing it required substantial changes in mobile air conditioning design. Similarly, selecting low GWP alternatives for R-410A in residential units requires careful evaluation.

The expansion of refrigerant reclamation and recycling programs offers a method to manage existing assets, while the use of ammonia for industrial cold storage remains a highly efficient, albeit safety-intensive, option. Ultimately, creating a digital twin for refrigerant management is becoming essential for tracking assets and ensuring compliance across a diverse portfolio.

Primary Growth Driver: The exponential growth of global cold chain logistics, driven by demand for perishable goods and pharmaceuticals, is a key driver for the refrigerants market.

Market growth is propelled by a convergence of regulatory mandates and macroeconomic shifts. The implementation of systematic phase-down schedules under the Kigali Amendment acts as a forcing function, compelling the industry to abandon high-GWP HFC refrigerants.

This regulatory push is amplified by the rapid expansion of global cold chain logistics, essential for the food and pharmaceutical sectors.

Concurrently, accelerating urbanization in developing nations, particularly in the APAC region which is growing at 7.6% annually, fuels demand for residential and commercial air conditioning.

This creates a powerful, sustained need for new cooling capacity, from large-scale district cooling projects in new urban developments to the proliferation of mobile air conditioning (MAC) in an expanding global vehicle fleet.

Emerging Market Trend: The proliferation of natural and ultra-low global warming potential substances is a defining market trend. This shift is driven by regulatory mandates and a growing emphasis on sustainable cooling solutions.

The market is advancing beyond chemical innovation, with digitalization emerging as a transformative trend. The integration of IoT sensors and AI-powered analytics enables predictive maintenance, shifting from reactive repairs to proactive management of HVACR systems. This technology is critical for early refrigerant leak detection, which addresses a major source of both environmental impact and operational cost.

Digital platforms now allow for sophisticated system performance monitoring and refrigerant charging optimization, ensuring that equipment runs at its peak energy efficiency ratio (EER). Furthermore, these tools are vital for executing a robust refrigerant management plan, automating the tracking required for regulatory compliance under frameworks like the F-Gas regulation.

This move toward smart systems enhances reliability and extends asset lifespan, fundamentally altering the service and maintenance landscape.

Key Industry Challenge: Safety and flammability risks associated with many eco-friendly alternative refrigerants present a significant challenge, requiring new standards and technician training.

A primary challenge restraining market adoption of next-generation refrigerants is the flammability risk assessment associated with many low-GWP alternatives. The use of A2L and A3 refrigerants, such as propane, necessitates a comprehensive overhaul of building codes and safety standards, alongside significant investment in technician training to handle high-pressure systems safely.

This is compounded by the high capital expenditure required for refrigerant retrofitting or the deployment of entirely new infrastructures like transcritical CO2 systems, a significant barrier for many businesses.

Furthermore, the fragmented global regulatory landscape, with varying phase-down schedules, complicates supply chain management for multinational corporations and creates opportunities for the illicit trade of banned substances, undermining environmental goals and posing safety risks from non-compliant products.

Explore Full Market Dynamics Analysis Request Free Sample

Refrigerants Market Segmentation

The refrigerants industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

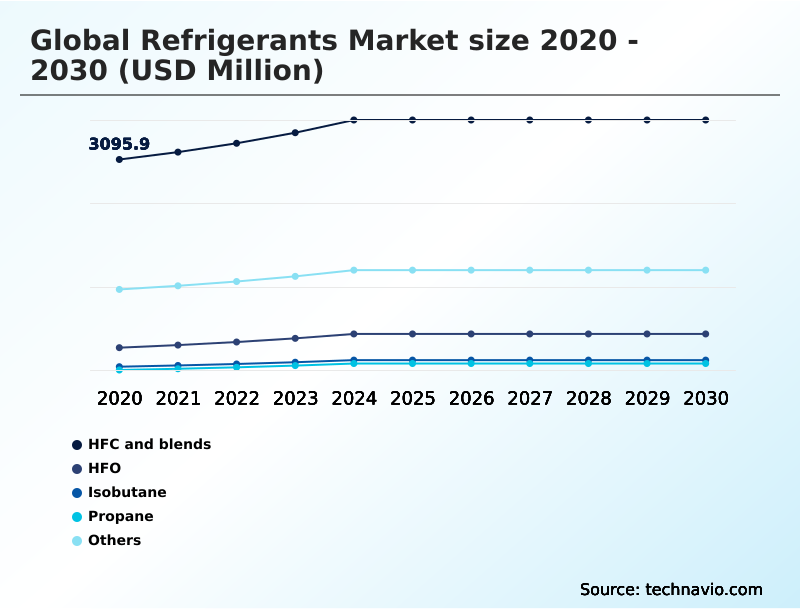

Product Segment Analysis

The hfc and blends segment is estimated to witness significant growth during the forecast period.

The hydrofluorocarbons (HFCs) and blends segment is navigating a critical transition shaped by global phase-down schedules.

While HFC refrigerants still represent the largest component of the installed base in existing HVACR systems, their high Global Warming Potential (GWP) has triggered stringent regulatory actions under frameworks like the Kigali Amendment.

This creates a bifurcated market reality for procurement decision-makers, balancing the ongoing service needs of legacy equipment against the capital investment required for refrigerant retrofitting or full system replacement.

The focus is shifting towards managing the remaining lifecycle of these systems as the availability of virgin HFCs diminishes, driving up service costs and making the total cost of ownership for older assets a primary concern.

The HFC and blends segment was valued at USD 3.61 billion in 2024 and showed a gradual increase during the forecast period.

Refrigerants Market by Region: APAC Leads with 46.8% Growth Share

APAC is estimated to contribute 46.8% to the growth of the global market during the forecast period.

The geographic landscape is dominated by the APAC region, which is projected to contribute approximately 47% of the market's incremental growth.

This expansion is powered by rapid urbanization and industrial development in countries like China and India, driving demand for both commercial and residential HVACR systems.

In contrast to mature markets focused on refrigerant retrofitting, APAC's growth is largely from new installations, including district cooling projects and the build-out of cold chain logistics to support food and pharmaceutical supply chains.

Regional policies such as India's Cooling Action Plan are shaping technology choices, encouraging the adoption of refrigerants with a lower global warming potential.

The region's manufacturing prowess also makes it a central hub for producing both cooling equipment and thermally conductive materials, influencing global supply chain stability.

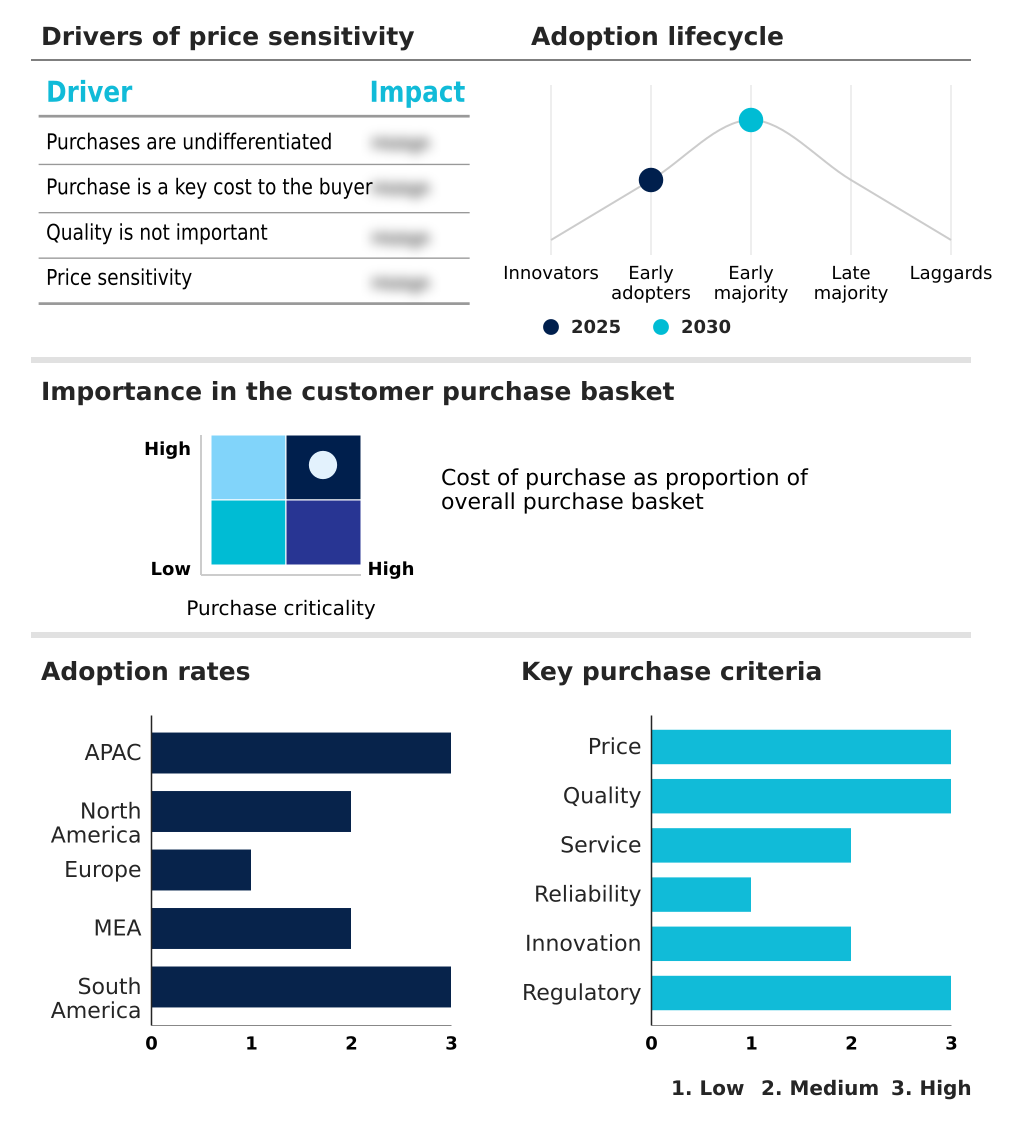

Customer Landscape Analysis for the Refrigerants Market

The refrigerants market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the refrigerants market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Refrigerants Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the refrigerants market industry.

A Gas International Ltd. - Key offerings center on low-GWP HFO refrigerants, providing advanced thermal management solutions engineered to meet stringent environmental regulations and enhance system efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- A Gas International Ltd.

- AGC Inc.

- Air Liquide SA

- Arkema Group

- Daikin Industries Ltd.

- Dongyue Group Ltd.

- Gujarat Fluorochemicals Ltd.

- Harp International Ltd.

- Honeywell International Inc.

- Hudson Technologies, Inc.

- Linde Plc

- National Refrigerants Inc.

- Orbia

- Resonac Holdings Corp.

- Sinochem Hong Kong (Group) Co., Ltd

- SRF Ltd.

- Tazzetti Spa

- The Chemours Co.

- Trane Technologies Plc

- WEITRON Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Refrigerants Market

- In November 2024, Honeywell International Inc. announced a strategic partnership with a leading automotive OEM to supply its Solstice yf (HFO-1234yf) refrigerant for a new line of electric vehicles, ensuring compliance with EPA regulations under the AIM Act.

- In February 2025, Taiwan's Ministry of Environment released two official notices implementing Regulations on Hydrofluorocarbons (HFCs) Management, establishing categories of HFCs that are prohibited or restricted from being manufactured, imported, sold, or used.

- In March 2025, A-Gas completed the acquisition of Refrigerant Services Inc., a prominent Canadian refrigerant services company, thereby expanding its refrigerant recovery and reclamation capacity in North America.

- In May 2025, Daikin Industries Ltd. announced a USD 100 million investment to expand its R&D facility in Osaka, Japan, focused on developing next-generation heat pump systems using low-GWP refrigerants like R-32 and new HFO blends.

Research Analyst Overview: Refrigerants Market

The operational reality of the refrigerants market is defined by a fundamental tension: managing a vast installed base of equipment designed for HFC refrigerants while navigating a mandatory transition to low-GWP alternatives.

This creates a critical boardroom-level decision concerning capital allocation—investing in new, compliant HVACR systems and heat pump systems versus managing the rising operational costs of servicing legacy equipment with quota-restricted gases. The classification of A2L refrigerants and A3 refrigerants under ASHRAE Standard 34 introduces new flammability risk assessments into facility design and insurance considerations.

For example, while HFO refrigerants offer a viable path forward, their deployment in centrifugal chillers and screw chillers requires specific training and handling protocols.

With the HFC and blends segment still accounting for a major share of the market, the growth of refrigerant reclamation infrastructure is essential to support the service life of existing assets without violating phase-down schedules, impacting everything from mobile air conditioning (MAC) to industrial ammonia refrigeration.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Refrigerants Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 311 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.7% |

| Market growth 2026-2030 | USD 2879.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.3% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Refrigerants Market: Key Questions Answered in This Report

-

What is the expected growth of the Refrigerants Market between 2026 and 2030?

-

The Refrigerants Market is expected to grow by USD 2.88 billion during 2026-2030, registering a CAGR of 6.7%. Year-over-year growth in 2026 is estimated at 6.3%%. This acceleration is shaped by exponential growth of global cold chain logistics, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (HFC and blends, HFO, Isobutane, Propane, and Others), Application (Refrigeration system, Air Conditioning system, Chillers, and Mobile air conditioning), End-user (Commercial refrigeration, Residential refrigeration, Industrial refrigeration, and Transportation refrigeration) and Geography (APAC, North America, Europe, Middle East and Africa, South America). Among these, the HFC and blends segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, North America, Europe, Middle East and Africa and South America. APAC is estimated to contribute 46.8% to market growth during the forecast period. Country-level analysis includes China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is exponential growth of global cold chain logistics, which is accelerating investment and industry demand. The main challenge is safety and flammability risks associated with eco-friendly alternatives, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Refrigerants Market?

-

Key vendors include A Gas International Ltd., AGC Inc., Air Liquide SA, Arkema Group, Daikin Industries Ltd., Dongyue Group Ltd., Gujarat Fluorochemicals Ltd., Harp International Ltd., Honeywell International Inc., Hudson Technologies, Inc., Linde Plc, National Refrigerants Inc., Orbia, Resonac Holdings Corp., Sinochem Hong Kong (Group) Co., Ltd, SRF Ltd., Tazzetti Spa, The Chemours Co., Trane Technologies Plc and WEITRON Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Refrigerants Market Research Insights

Market dynamics are dictated by the interplay between regulatory mandates and technology readiness. The Kigali Amendment compliance framework sets the overarching pace, but regional enforcement, such as the EU's F-Gas regulation and the EPA AIM Act in the US, creates distinct market conditions.

This regulatory pressure accelerates the transition away from high-GWP substances, influencing total cost of ownership calculations for new equipment. For instance, the rapid adoption of low-GWP refrigerants in Europe contrasts with the high-volume growth in APAC, which accounts for over 46% of the market's incremental growth, driven by new construction rather than retrofitting.

This divergence requires a nuanced approach to supply chain management and product strategy, balancing the need for innovative thermal management solutions with the practicalities of lubricant compatibility and refrigerant retrofitting in diverse economic environments.

We can help! Our analysts can customize this refrigerants market research report to meet your requirements.

RIA -

RIA -