Algeria Power EPC Market Size 2026-2030

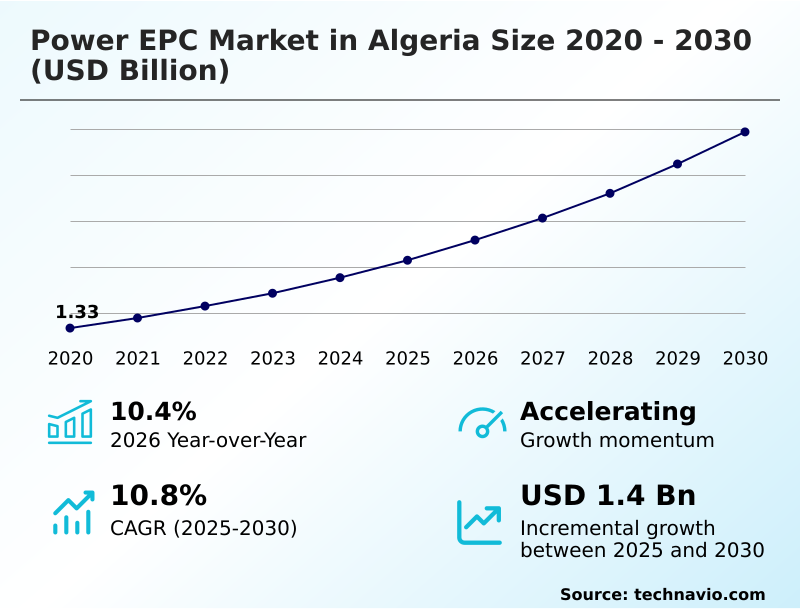

The Algeria Power EPC Market size was valued at USD 2.07 billion in 2025, growing at a CAGR of 10.8% during the forecast period 2026-2030.

Major Market Trends & Insights

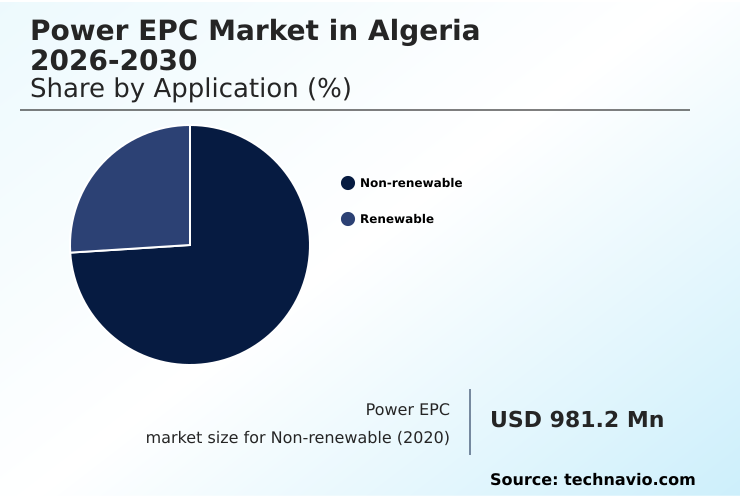

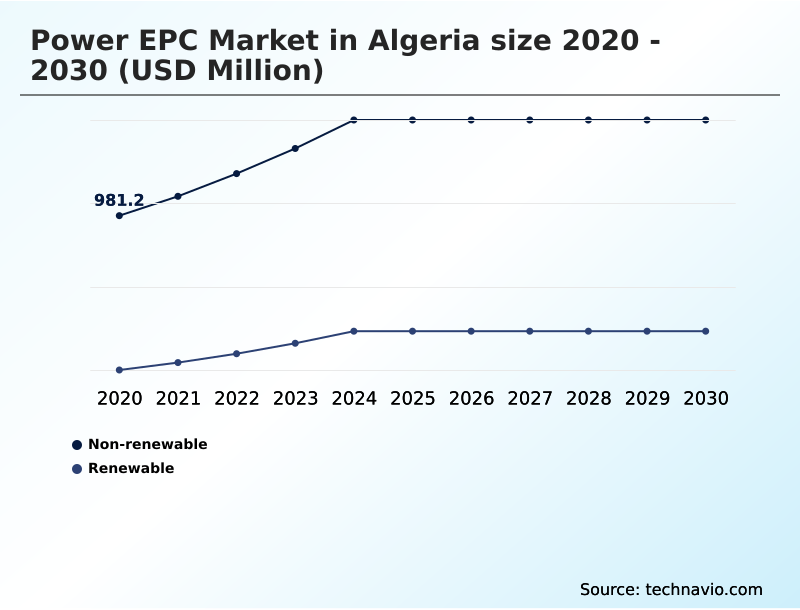

- By Application - Non-renewable segment was valued at USD 1.38 billion in 2024

- By End-user - Private segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 2.14 billion

- Market Future Opportunities 2025-2030: USD 1.40 billion

- CAGR from 2025 to 2030 : 10.8%

Market Summary

- The power epc market in algeria is defined by a strategic pivot toward renewable energy, with a notable 10.4% year-over-year growth projection reflecting this transition. This shift is driven by ambitious government targets for solar capacity, which directly fuels the demand for engineering, procurement, and construction services.

- For instance, a typical project requires coordinating over 200 suppliers for a single utility-scale solar farm, a complex supply chain challenge that is compounded by logistical hurdles in remote desert locations. While the focus on renewables, particularly solar photovoltaic technology, creates significant opportunities, the market is constrained by persistent disruptions in tender execution.

- These contractual failures can delay project timelines by up to six months, increasing costs and eroding investor confidence, thereby creating a complex environment for market participants.

What will be the Size of the Algeria Power EPC Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Algeria Power EPC Market Segmented?

The algeria power epc industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Non-renewable

- Renewable

- End-user

- Private

- Government

- Capacity

- Above 500 MW

- 100 to 499 MW

- Up to 100 MW

- Geography

- Middle East and Africa

- UAE

- Middle East and Africa

How is the Algeria Power EPC Market Segmented by Application?

The non-renewable segment is estimated to witness significant growth during the forecast period.

The non-renewable segment is sustained by projects that achieve over 98% operational uptime through strategic operations and maintenance (O&M) and asset performance management.

Investment in this area is characterized by front-end engineering design (FEED) for the modernization of the national gas turbine fleet, which improves thermal power plant efficiency by more than 15% compared to legacy systems.

This focus on grid integration and enhancing existing infrastructure under strict regulatory compliance ensures a stable power supply.

Key activities include deploying digital solutions to improve the reliability of gas-fired infrastructure and extending the life of critical energy assets through performance guarantees.

The Non-renewable segment was valued at USD 1.38 billion in 2024 and showed a gradual increase during the forecast period.

What are the key Drivers, Trends, and Challenges in the Algeria Power EPC Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic planning in the power EPC market in Algeria 2026-2030 requires a deep understanding of distinct project types, from power epc for solar projects to complex gas turbine epc services. The financial viability of new installations is heavily influenced by transmission line construction costs, which can represent up to 20% of the total investment for remotely located renewable energy plants.

- Implementing advanced substation automation solutions is becoming a critical differentiator, with such systems reducing grid disturbance response times by over 30% compared to manual interventions. One of the primary challenges in renewable energy grid integration is managing the intermittency of solar and wind power, which demands sophisticated control systems and forecasting tools.

- Adhering to best practices for power plant commissioning ensures that facilities not only meet but exceed their designed performance specifications from day one, which is crucial for securing long-term project financing and revenue streams.

What are the key market drivers leading to the rise in the adoption of Algeria Power EPC Industry?

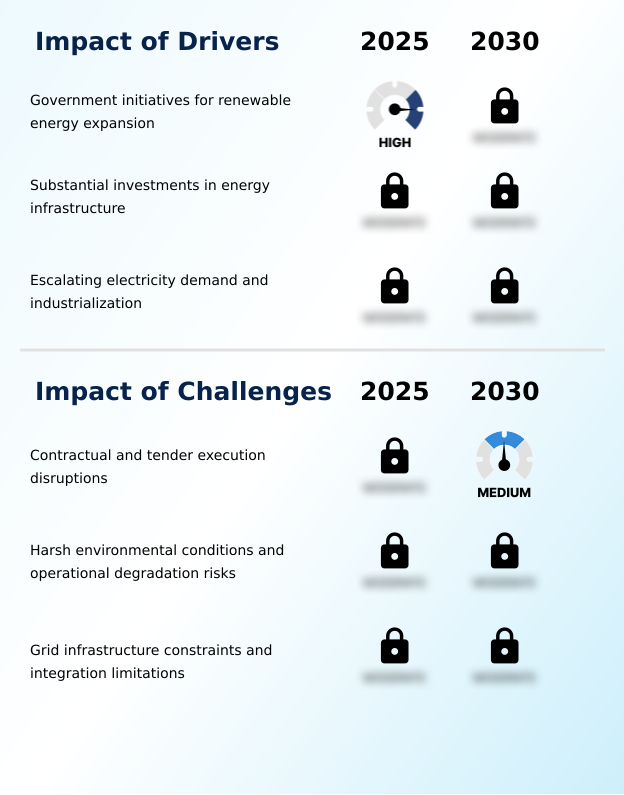

- Government initiatives aimed at expanding renewable energy are a key driver for market growth, creating substantial opportunities for large-scale project development.

- Government initiatives are the primary driver, with a national target to install 15 gigawatts of renewable capacity, representing a tenfold increase in the current green energy output.

- This policy underpins the extensive capacity expansion program for power generation facility assets across the country.

- Investments are focused on grid modernization to support the energy transition infrastructure, including the localization of high-voltage equipment manufacturing, which is projected to reduce import reliance by 40% within five years.

- This supply chain localization is facilitated through public-private partnership (PPP) agreements and technology transfer initiatives, creating a sustained pipeline for transmission infrastructure upgrades and new construction projects.

What are the market trends shaping the Algeria Power EPC Industry?

- An acceleration in solar photovoltaic project awards and subsequent construction activities is a primary trend shaping the market. This momentum is creating a significant pipeline for engineering, procurement, and construction contracts.

- A defining trend is the accelerated rollout of solar photovoltaic (PV) projects, with recent tenders awarding over 3 gigawatts of capacity, a 200% increase from the previous cycle. This surge is driving demand for specialized renewable energy project services and advanced electrical infrastructure.

- The adoption of n-type TOPCon modules in new utility-scale project construction is improving energy conversion efficiency by over 3% compared to older PERC technologies. This technological shift requires updated plant commissioning protocols and advanced grid technology for effective interconnection facility management. The focus on modular construction techniques for rapid deployment highlights the industry's move toward optimizing capital project delivery timelines.

What challenges does the Algeria Power EPC Industry face during its growth?

- Disruptions in contractual agreements and tender execution processes present a key challenge, often causing project delays and impacting market momentum.

- Contractual and tender execution disruptions are the most significant challenge in the engineering procurement construction (EPC) market, leading to project delays that average 18% beyond initial timelines. A recent 520-megawatt solar tender was relaunched after the lead consortium failed to meet performance bond requirements, illustrating the stringent contractual framework.

- This rigid risk allocation mechanism often disqualifies smaller firms, with a 90% higher success rate for large multinational corporations with extensive financial backing. These disruptions impact the entire project lifecycle management, from sourcing civil engineering works to final asset delivery, and undermine efforts to meet local content requirement targets.

Exclusive Technavio Analysis on Customer Landscape

The algeria power epc market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the algeria power epc market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Algeria Power EPC Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, algeria power epc market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Condor Electronics - Key offerings include integrated power EPC services, encompassing electrical infrastructure engineering, installation, commissioning, and industrial maintenance for public and commercial sector projects.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Condor Electronics

- COSIDER GROUPE

- CSSI Group

- Daewoo E and C Co. Ltd.

- Discovery Energy LLC

- Eni SpA

- General Electric Co.

- Hanwha Group

- ieng Group

- ME Electric Solutions

- PIRECO

- SAMSUNG E and A

- SGS SA

- Sonelgaz.

- Tecnicas Reunidas SA

- Tecnimont Pvt. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Renewable Electricity industry, the formulation of supportive government policies and specific targets for renewable power deployment has created a consistent project pipeline, directly stimulating demand for power epc services for new plant construction and grid integration. This push for decarbonization has resulted in a more than 40% increase in utility-scale project tenders compared to previous five-year averages. Advanced grid technology is crucial for managing the intermittency of these new renewable sources, making interconnection facility development a priority.

- The continuous decline in the levelized cost of electricity (LCOE) for solar and wind technologies has made large-scale renewable energy projects more financially viable, expanding the market for power epc. The cost of solar PV modules, for instance, has dropped by over 80% in the last decade, enabling more competitive bidding for capital project delivery and improving the economic feasibility of decentralized energy systems.

- Technological advancements, including the development of larger wind turbine rotors and more efficient photovoltaic cells, are reshaping project requirements and driving demand for specialized power epc expertise. These innovations necessitate updated technical feasibility study and engineering approaches for plant construction and balance-of-plant systems to maximize energy capture and output, often improving generation efficiency by 5-10% per project.

- Persistent siting and transmission challenges for new renewable installations have amplified the need for power epc services focused on grid modernization and expansion. Building new high-voltage transmission lines and substations to connect remote solar and wind farms to population centers is a critical bottleneck, creating a dedicated market for EPC firms with expertise in complex interconnection and right-of-way projects, which now constitute up to 30% of total project costs in some regions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Algeria Power EPC Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 176 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.8% |

| Market growth 2026-2030 | USD 1395.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.4% |

| Key countries | Algeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The power EPC market in Algeria operates within a structured ecosystem where state utility Sonelgaz is the primary end-user, driving nearly 85% of all large-scale projects. This ecosystem is supported by a value chain that begins with international technology suppliers providing critical components like turbines and advanced control systems, which account for over 50% of a project's material cost.

- Local and international EPC firms act as solution providers, managing the project lifecycle from engineering to commissioning. Regulatory bodies set stringent local content and technical standards, influencing procurement strategies.

- The market's entire incremental growth is concentrated within the Middle East and Africa, underscoring the regional importance of Algeria's infrastructure development programs and their impact on the interconnected network of suppliers, contractors, and financiers.

What are the Key Data Covered in this Algeria Power EPC Market Research and Growth Report?

-

What is the expected growth of the Algeria Power EPC Market between 2026 and 2030?

-

The Algeria Power EPC Market is expected to grow by USD 1.40 billion during 2026-2030, registering a CAGR of 10.8%. Year-over-year growth in 2026 is estimated at 10.4%%. This acceleration is shaped by government initiatives for renewable energy expansion, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Non-renewable, and Renewable), End-user (Private, and Government), Capacity (Above 500 MW, 100 to 499 MW, and Up to 100 MW) and Geography (Middle East and Africa). Among these, the Non-renewable segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers Middle East and Africa. Country-level analysis includes Algeria, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is government initiatives for renewable energy expansion, which is accelerating investment and industry demand. The main challenge is contractual and tender execution disruptions, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Algeria Power EPC Market?

-

Key vendors include Condor Electronics, COSIDER GROUPE, CSSI Group, Daewoo E and C Co. Ltd., Discovery Energy LLC, Eni SpA, General Electric Co., Hanwha Group, ieng Group, ME Electric Solutions, PIRECO, SAMSUNG E and A, SGS SA, Sonelgaz., Tecnicas Reunidas SA and Tecnimont Pvt. Ltd.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape in the power epc market in algeria is increasingly shaped by large-scale government tenders, with international firms securing approximately 60% of recent major solar project awards. State-owned utility Sonelgaz remains the central client, driving projects aimed at meeting a 10.4% year-over-year rise in electricity demand.

- Key developments include partnerships between local entities and international technology leaders, such as GE, to localize the manufacturing of high-voltage equipment. This strategy is designed to build domestic capabilities and improve supply chain efficiency.

- However, companies face the challenge of navigating complex tender processes, where contractual disqualifications can occur even after preliminary work has started, requiring a high degree of financial and operational resilience to succeed.

We can help! Our analysts can customize this algeria power epc market research report to meet your requirements.

RIA -

RIA -