Playing Cards Market Size 2026-2030

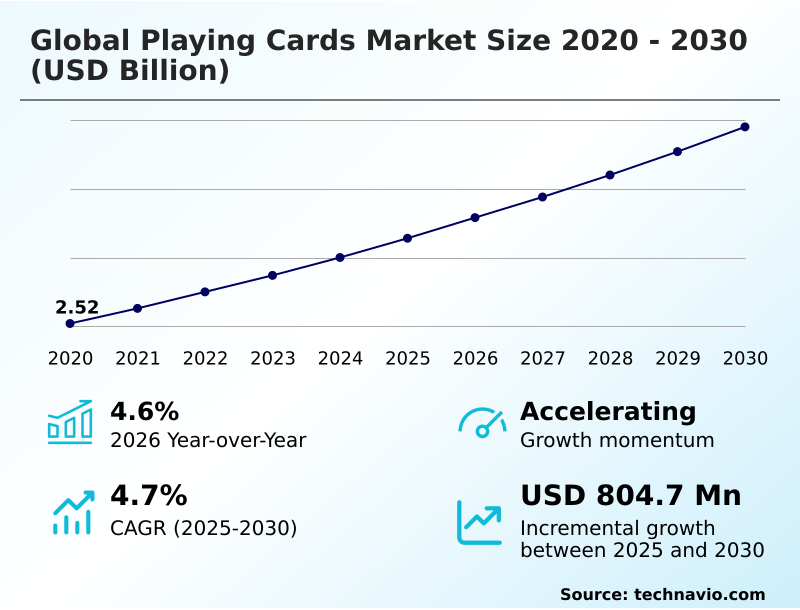

The Playing Cards Market size was valued at USD 3.14 billion in 2025, growing at a CAGR of 4.7% during the forecast period 2026-2030.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 40.4% growth during the forecast period.

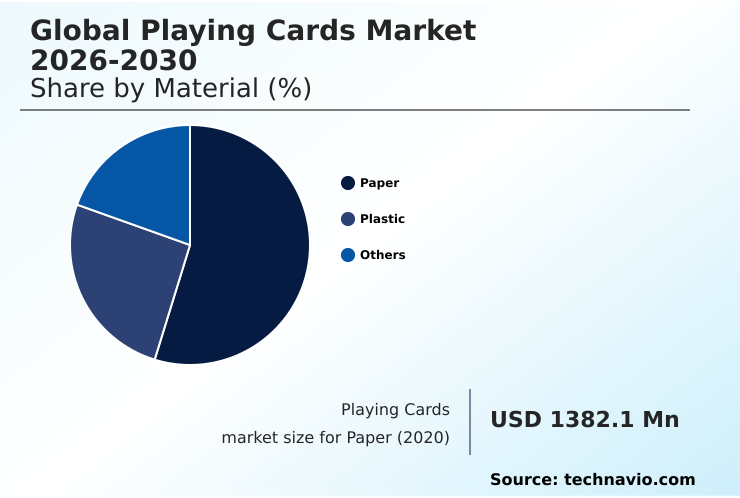

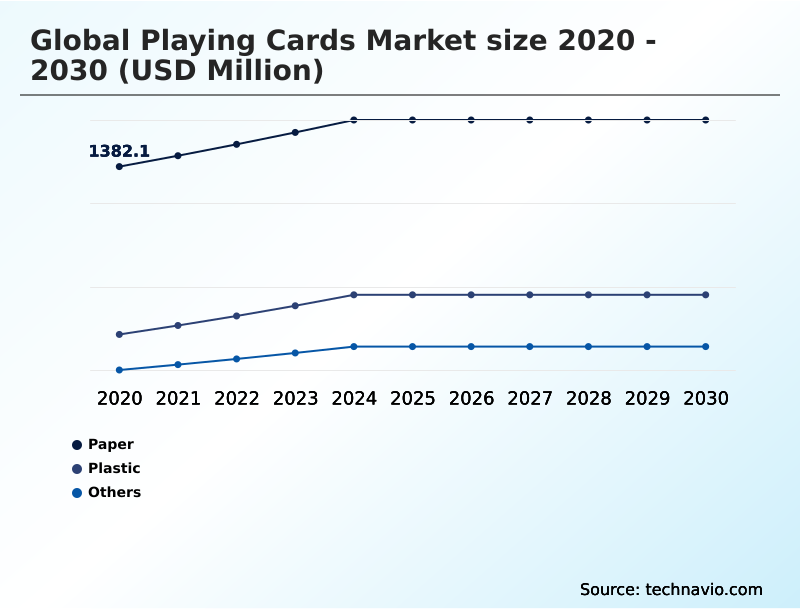

- By Material - Paper segment was valued at USD 1.59 billion in 2024

- By Application - Home entertainment segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 1.42 billion

- Market Future Opportunities 2025-2030: USD 804.7 million

- CAGR from 2025 to 2030 : 4.7%

Market Summary

- The playing cards market demonstrates notable resilience by adapting to modern consumer preferences, with the paper segment alone projected to grow by 4.7% annually. This expansion is driven by a societal shift toward tactile, screen-free entertainment, which has revitalized tabletop gaming culture.

- A key business strategy involves material innovation; for example, manufacturers are transitioning to forest-certified paper and biodegradable coatings, a move that can increase material costs by 10% but appeals to an eco-conscious consumer base. This driver helps counteract the primary challenge: competition from digital entertainment platforms, which capture a significant share of leisure time.

- Despite this, the demand from professional sectors like casinos, which require high-volume, continuous replacement of decks to ensure game integrity, provides a stable revenue stream, with some establishments replacing decks after a single use to maintain security.

What will be the Size of the Playing Cards Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Playing Cards Market Segmented?

The playing cards industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Material

- Paper

- Plastic

- Others

- Application

- Home entertainment

- Casino and gambling

- Tournament gaming

- Others

- Distribution channel

- Offline

- Online

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- APAC

How is the Playing Cards Market Segmented by Material?

The paper segment is estimated to witness significant growth during the forecast period.

The playing cards market is segmented by material, application, and distribution channel, with each segment reflecting distinct consumer behaviors and supply chain requirements.

The paper segment dominates, accounting for over 52% of the market, driven by its cost-effectiveness for the mass market and advancements in paper engineering.

In contrast, the plastic segment, utilizing synthetic polymers, exhibits robust growth in professional settings, where its durability can reduce replacement costs by up to 40%.

The home entertainment application holds a 37% share, underscoring the product's role in tactile social interactions.

This preference supports the offline distribution channel, which still captures over 65% of sales, demonstrating the value consumers place on physically assessing packaging and card quality before purchase.

The Paper segment was valued at USD 1.59 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Playing Cards market is rising in the leading region?

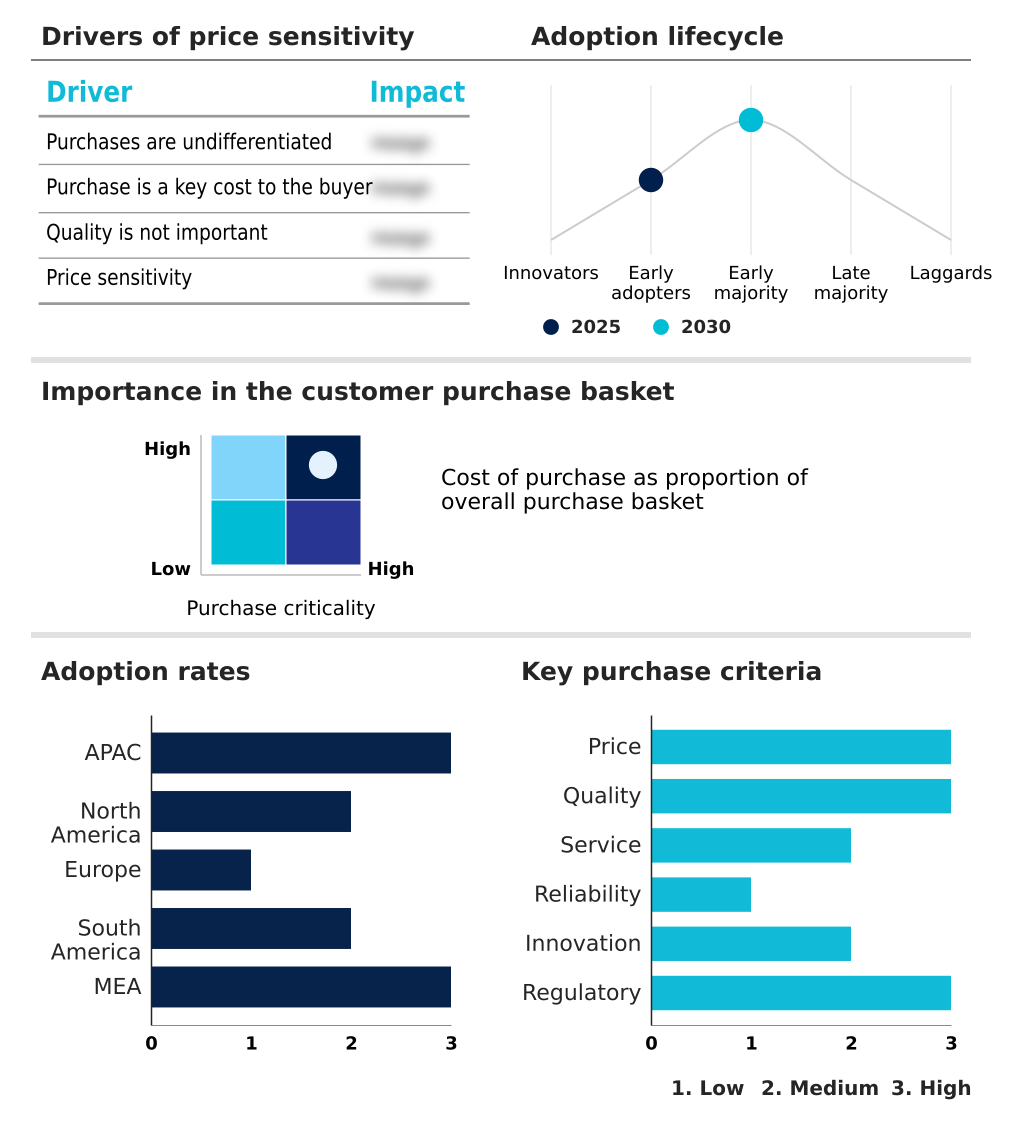

APAC is estimated to contribute 40.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Playing Cards Market demand is rising in APAC Request Free Sample

The geographic landscape of the playing cards market is led by APAC, which is projected to contribute 40.4% of the market's total incremental growth, expanding at a CAGR of 5.2%.

This outpaces the more mature markets of North America and Europe, which are forecast to grow at 4.9% and 3.9%, respectively.

The dynamism in APAC is driven by countries like China, with a market size of $399.7 million in 2025, and the rapid expansion of casino operations across the region.

This institutional demand for high-security, professional-grade decks contrasts with North America, where the market is heavily influenced by the trend of collector-centric editions and artisanal design.

This divergence requires manufacturers to adapt their product strategies, focusing on security features for APAC and tactile aesthetics for North American consumers.

What are the key Drivers, Trends, and Challenges in the Playing Cards Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolving regulatory and technological landscape is compelling manufacturers to rethink production from the ground up. For instance, high-security rfid playing card regulations in major gaming jurisdictions are no longer a niche requirement but a new standard, forcing investment in advanced printing and embedding technologies.

- This intersects with a powerful consumer-driven movement toward sustainable manufacturing in casino supplies, where the focus extends beyond simple recycling. The development of new biodegradable coatings for playing cards is a key R&D focus, with successful formulations reducing landfill waste from a single large casino by over 25% annually.

- These material science advancements are now influencing artisanal playing card design trends, where eco-credentials have become a significant marketing feature. Simultaneously, digital integration in physical card games is adapting to these new materials, ensuring that augmented reality features function flawlessly on non-traditional surfaces.

- This convergence of security, sustainability, and technology creates a complex but highly innovative market where adapting to one trend often requires investment across all three, a challenge that separates market leaders from followers.

What are the key market drivers leading to the rise in the adoption of Playing Cards Industry?

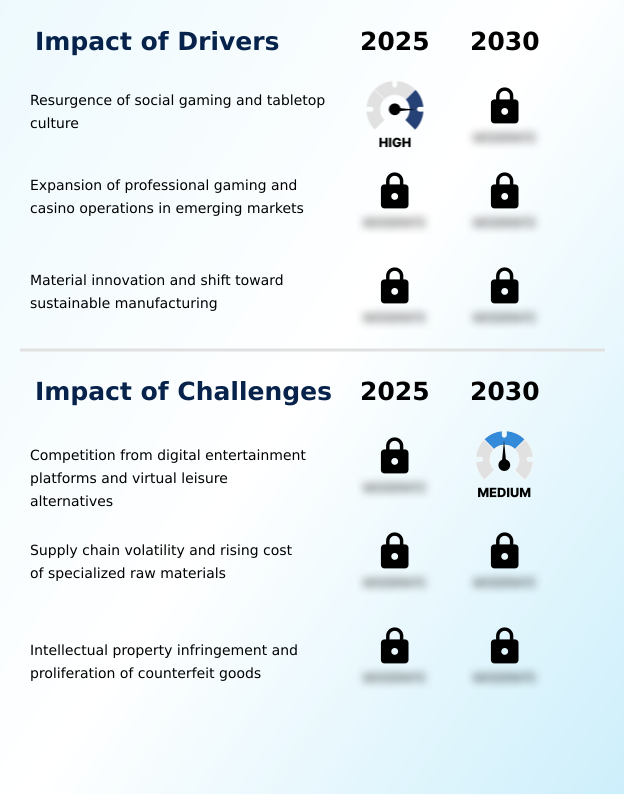

- The resurgence of social gaming and tabletop culture is a key driver, renewing demand for tactile, screen-free entertainment and interpersonal connection.

- A primary driver for the playing cards market is the industry-wide shift toward sustainability, with products made from sustainable materials seeing a 15% higher adoption rate among younger consumer demographics.

- This trend compels manufacturers to prioritize the use of forest-certified paper and move away from traditional synthetic polymers.

- The development and adoption of new water-borne coatings and vegetable-based inks not only meet stricter environmental regulations but also serve as a key brand differentiator.

- While this transition can increase initial production costs by approximately 10%, it aligns with the growing demand for circular production models and enhances long-term brand loyalty in an increasingly eco-conscious market.

What are the market trends shaping the Playing Cards Industry?

- The proliferation of artisanal designs and collector-centric limited editions is an increasingly significant trend. This shift positions playing cards as high-value, functional art objects.

- The integration of digital technologies with physical playing cards, known as phygital gaming, is a dominant market trend, increasing player engagement by an estimated 30% compared to traditional formats. This evolution leverages augmented reality integration, where mobile apps recognize card designs to unlock interactive content, and RFID embedded cards, which automate tracking in professional gaming.

- The adoption of a universal object recognition protocol has been pivotal, reducing development costs for hybrid gaming experiences by up to 40%. This trend moves beyond simple card manipulation, enhancing the tactile aesthetics of the physical product with a layer of digital interactivity, a feature particularly popular in tech-forward markets.

What challenges does the Playing Cards Industry face during its growth?

- A key challenge affecting industry growth is the escalating competition from digital entertainment platforms and immersive virtual leisure alternatives.

- A significant challenge confronting the playing cards market is intellectual property infringement, with counterfeit goods eroding revenues for legitimate creators of artisanal designs by an estimated 20-25%. These unauthorized replicas, often sold through online marketplaces, lack the sophisticated security features like micro-printing and ultraviolet markings found in authentic products.

- This not only results in direct financial loss but also damages brand reputation, as the fakes are produced with inferior materials that fail to replicate the intended air-cushion finish and tactile aesthetics. Consequently, manufacturers are forced to invest heavily in anti-counterfeiting technologies, which can increase unit costs by 5-10%.

Exclusive Technavio Analysis on Customer Landscape

The playing cards market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the playing cards market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Playing Cards Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, playing cards market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Angel Playing Cards Co.Ltd. - Key offerings span from standard paper decks for casual use to high-durability plastic cards for casinos and premium, artistically designed collectibles for enthusiasts and professionals.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Angel Playing Cards Co.Ltd.

- Art of Play

- Cartamundi Group

- Copag USA

- Ellusionist

- Expert Playing Card Co.

- Kings Wild Project Inc

- Kuo Kau Paper Products Co.Ltd.

- Legends Playing Card Co.

- Modiano S.p.A.

- Naipes Heraclio Fournier, S.A.

- Nintendo Co. Ltd.

- QP Group Holdings Ltd.

- Riffle Shuffle Playing Card Co.

- Shanghai Three-A Playing Cards Co.Ltd.

- Shenzhen Wangjing Printing Co.

- Shuffled Ink

- Teodoro Dal Negro S.p.A.

- Theory11.

- Wiener Spielkartenfabrik Ferd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Leisure Products industry, rising dual-income households have increased discretionary spending, directly boosting sales of premium and collector-centric editions of playing cards, which are increasingly positioned as affordable luxury goods and part of a broader tabletop gaming culture.

- The strong growth in online sales and omnichannel retailing strategies across the leisure sector has enabled niche playing card manufacturers, especially those focused on artisanal design, to bypass traditional distribution and reach a global audience directly, fostering material innovation.

- Heightened regulatory compliance regarding toy safety and material content, including restrictions on certain chemicals, has influenced the playing cards market to adopt safer, non-toxic materials like vegetable-based inks and water-borne coatings, aligning with the trend towards sustainable materials.

- A growing consumer emphasis on healthy lifestyles and screen-free entertainment has revitalized interest in traditional social activities, positioning playing cards as a key tool for cognitive engagement and fostering tactile social interactions away from digital entertainment platforms.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Playing Cards Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 297 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.7% |

| Market growth 2026-2030 | USD 804.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.6% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Russia, Italy, Spain, Brazil, Argentina, Colombia, South Africa, Saudi Arabia, UAE, Turkey and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The playing cards market ecosystem is a complex value chain that begins with suppliers of raw materials like high-density paper pulp and synthetic polymers, with paper-based materials constituting over 52% of the market. Manufacturers such as Cartamundi Group and various boutique firms transform these inputs using specialized processes to create products with specific tactile aesthetics and security features.

- Regulatory bodies, including gaming commissions, heavily influence the high-stakes casino segment by mandating standards for card integrity. Distribution is handled through a mix of online platforms, which are growing at a rate 15% faster than traditional retail, and brick-and-mortar stores.

- The end-users range from home consumers driving the entertainment segment, which holds a 37% share, to professional casinos and tournament organizers who prioritize durability and anti-tampering technology.

What are the Key Data Covered in this Playing Cards Market Research and Growth Report?

-

What is the expected growth of the Playing Cards Market between 2026 and 2030?

-

The Playing Cards Market is expected to grow by USD 804.7 million during 2026-2030, registering a CAGR of 4.7%. Year-over-year growth in 2026 is estimated at 4.6%%. This acceleration is shaped by resurgence of social gaming and tabletop culture, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Material (Paper, Plastic, and Others), Application (Home entertainment, Casino and gambling, Tournament gaming, and Others), Distribution Channel (Offline, and Online) and Geography (APAC, North America, Europe, South America, Middle East and Africa). Among these, the Paper segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, North America, Europe, South America and Middle East and Africa. APAC is estimated to contribute 40.4% to market growth during the forecast period. Country-level analysis includes China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Russia, Italy, Spain, Brazil, Argentina, Colombia, South Africa, Saudi Arabia, UAE, Turkey and Egypt, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is resurgence of social gaming and tabletop culture, which is accelerating investment and industry demand. The main challenge is competition from digital entertainment platforms and virtual leisure alternatives, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Playing Cards Market?

-

Key vendors include Angel Playing Cards Co.Ltd., Art of Play, Cartamundi Group, Copag USA, Ellusionist, Expert Playing Card Co., Kings Wild Project Inc, Kuo Kau Paper Products Co.Ltd., Legends Playing Card Co., Modiano S.p.A., Naipes Heraclio Fournier, S.A., Nintendo Co. Ltd., QP Group Holdings Ltd., Riffle Shuffle Playing Card Co., Shanghai Three-A Playing Cards Co.Ltd., Shenzhen Wangjing Printing Co., Shuffled Ink, Teodoro Dal Negro S.p.A., Theory11. and Wiener Spielkartenfabrik Ferd.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for playing cards is consolidated at the top, with the five largest vendors accounting for over 35% of market share, yet vibrant due to a thriving niche segment. Large-scale manufacturers like Cartamundi Group focus on volume and expanding their global manufacturing footprint, recently launching initiatives to reclaim used plastic cards from casinos.

- In contrast, boutique firms such as Theory11. excel in the luxury and collector segments, leveraging high-concept graphic design and premium packaging, which command prices up to 500% higher than standard decks. These vendors navigate significant supply chain volatility, particularly in the cost of specialized paper pulp and coatings.

- Successful adaptation involves diversifying sourcing and investing in material science to create proprietary finishes, a key differentiator in both professional and collector markets.

We can help! Our analysts can customize this playing cards market research report to meet your requirements.

RIA -

RIA -