Personalized Digital Health Platforms Market Size and Growth Forecast 2026-2030

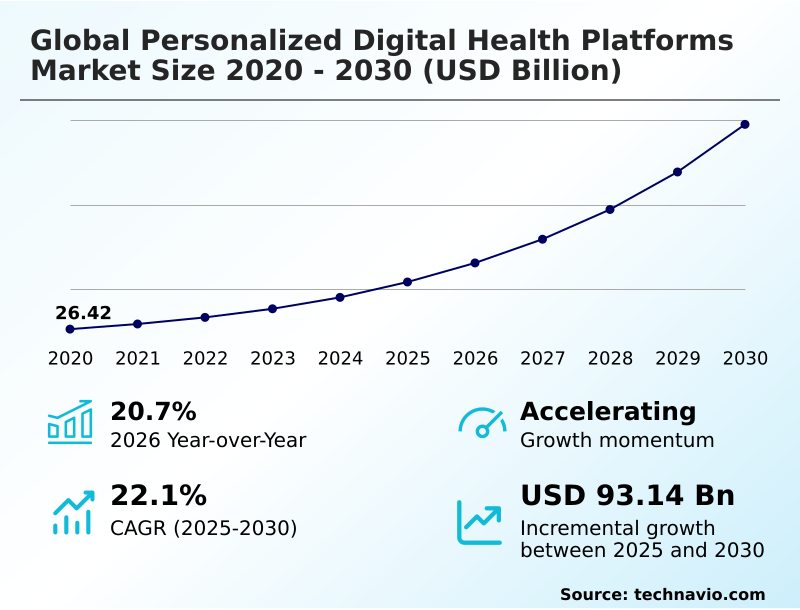

The Personalized Digital Health Platforms Market size was valued at USD 54.27 billion in 2025 growing at a CAGR of 22.1% during the forecast period 2026-2030.

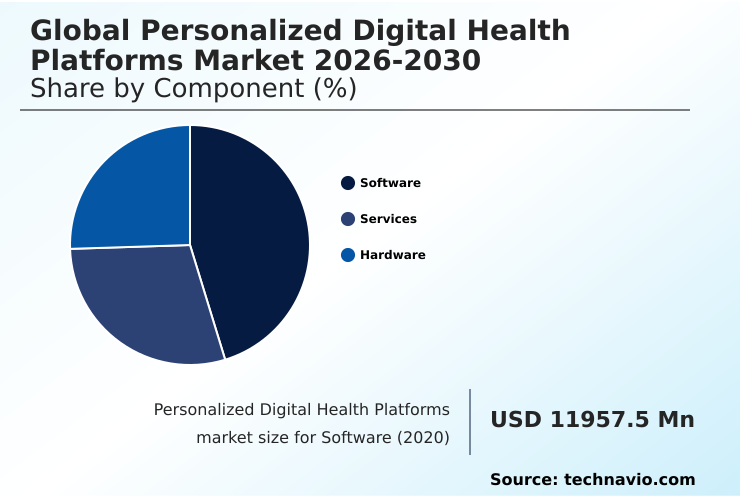

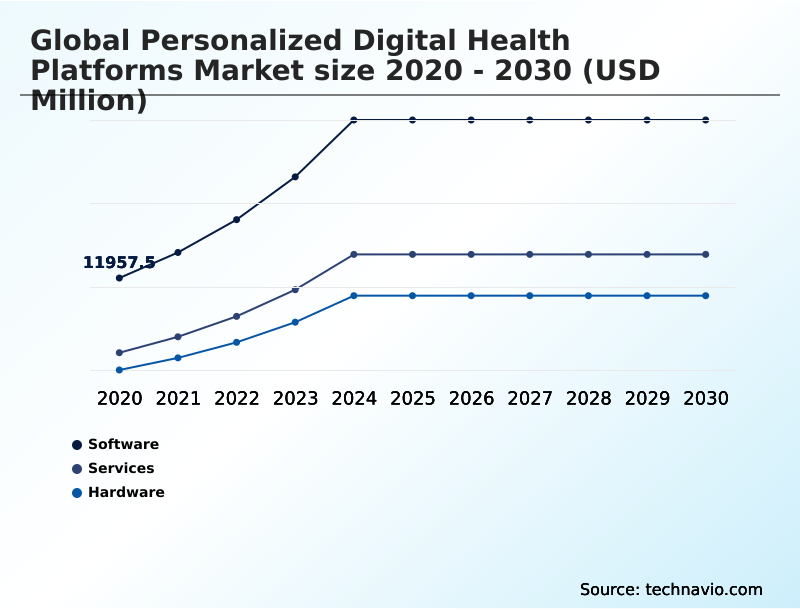

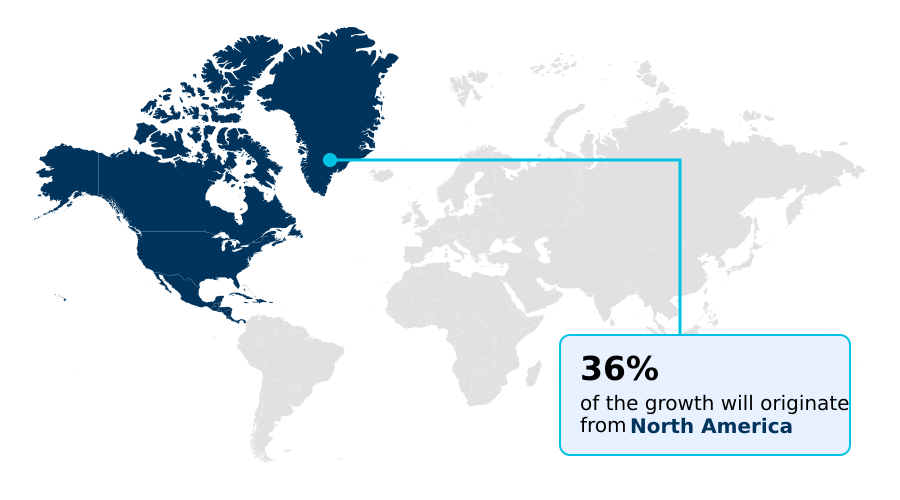

North America accounts for 35.5% of incremental growth during the forecast period. The Software segment by Component was valued at USD 20.92 billion in 2024, while the Healthcare providers segment holds the largest revenue share by End-user.

The market is projected to grow by USD 121.00 billion from 2020 to 2030, with USD 93.14 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Personalized Digital Health Platforms Market Overview

The personalized digital health platforms market is defined by the convergence of data analytics and patient-centric care models, with North America contributing over 35% of incremental growth. The operational core involves wearable sensor technology capturing real-time physiological monitoring data, which is then processed through AI-driven health insights to support proactive health interventions. This ecosystem relies on robust IoMT device connectivity and seamless electronic health records integration to create comprehensive individual health profiles. For instance, a cardiology clinic managing post-operative patients uses a platform for remote patient monitoring, tracking heart rate variability and medication adherence solutions through a patient's mobile health application. This digital therapeutics approach allows for early detection of anomalies, reducing readmission rates by identifying risks before they become critical events. The shift toward value-based care models further propels adoption, as providers are increasingly compensated based on measurable outcomes achieved through such data-driven wellness programs and chronic disease management apps.

Drivers, Trends, and Challenges in the Personalized Digital Health Platforms Market

Strategic decision-making in the personalized digital health platforms market is increasingly influenced by the need to navigate complex regulatory and technical landscapes. The integration of AI for predictive health analytics allows providers to shift from reactive to preventive care, a transition heavily dependent on robust data security in personalized health.

For example, a multi-state hospital system implementing IoMT for remote patient monitoring must ensure its entire data pipeline, from sensor to cloud, is fully compliant with HIPAA to avoid severe penalties. The adoption of blockchain for secure health records is gaining consideration as a method to address patient data interoperability challenges and build trust in digital health platforms.

Meanwhile, telehealth for rural healthcare access and the use of virtual reality for physical rehabilitation are expanding the market's reach. The market in Asia is growing at a faster rate, approximately 2.7 percentage points higher than in North America, which has significant implications for global supply chain and localization strategies.

Vendors are also exploring how biometric data for insurance underwriting could create new revenue streams while managing chronic conditions like diabetes through continuous monitoring. The use of gamification in patient engagement strategies is proving effective in improving adherence, while AI-powered diagnostics in personalized healthcare are enhancing clinical accuracy.

Finally, the impact of real-world evidence on drug development is linking digital health platforms to the pharmaceutical lifecycle.

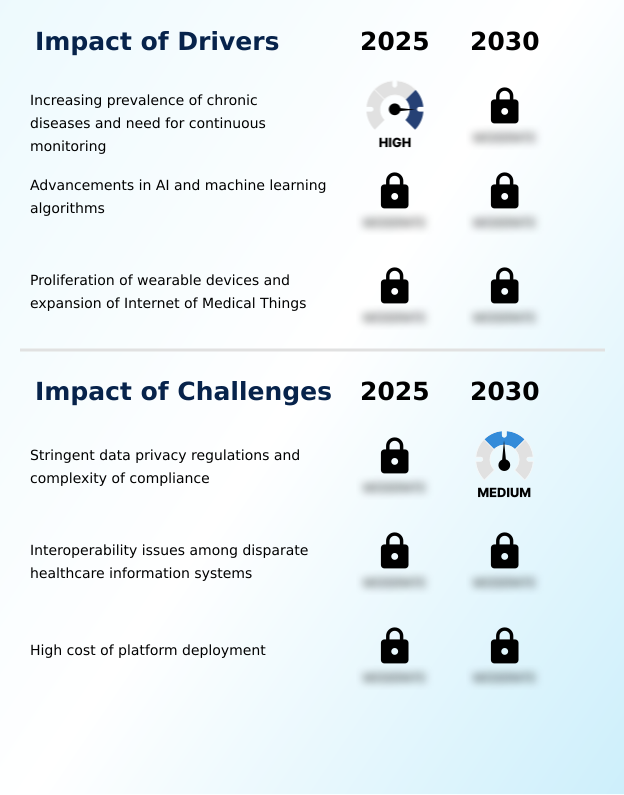

Primary Growth Driver: The increasing prevalence of chronic diseases and the corresponding need for continuous patient monitoring are key drivers of market growth.

Market expansion is fueled by the escalating prevalence of chronic conditions, creating immense demand for continuous monitoring for diabetes management and cardiovascular health tracking. This clinical need is met by rapid advancements in technology.

The proliferation of wearable technology for chronic care and IoMT for remote patient monitoring provides the necessary data streams. Simultaneously, progress in AI and machine learning allows platforms to process this data, offering predictive analytics and personalized recommendations.

These technologies enable a shift toward proactive care, with Asia emerging as the fastest-growing regional market, registering a growth rate of over 23%.

This technological synergy allows for the delivery of scalable and cost-effective personalized healthcare solutions, addressing systemic challenges in healthcare delivery worldwide.

Emerging Market Trend: A significant market trend is the integration of genomic data with advanced biomarker analytics. This shift enables hyper-personalized care pathways based on an individual's unique genetic makeup.

The market is advancing beyond simple activity tracking toward hyper-personalization, driven by three core trends. First, the integration of genomic data with real-time biomarker tracking is enabling highly specific care plans. Platforms are incorporating AI for predictive health analytics to offer customized fitness regimens and personalized nutrition based on genetics.

Second, to address low long-term adherence, vendors are deploying gamification in patient engagement strategies, using principles of behavioral psychology to drive sustainable habit formation. This is critical for applications in digital platforms for mental health support.

Finally, to tackle security concerns, blockchain for secure health records is being explored to enhance data integrity and give users control over their information, which is vital for building trust in digital health platforms and ensuring compliance with regulations like GDPR.

Key Industry Challenge: Stringent data privacy regulations, such as GDPR and HIPAA, and the complexities of ensuring global compliance present a key challenge affecting industry growth.

The market's growth is constrained by significant structural and regulatory hurdles. The foremost challenge involves stringent data privacy regulations, such as HIPAA and GDPR, which impose complex compliance burdens and increase operational costs for secure health data storage and data security in personalized health.

A second major barrier is the lack of patient data interoperability challenges among disparate systems, which silos information and prevents the creation of a unified patient view essential for effective personalized care. This fragments the digital health ecosystem. Finally, high deployment costs and cultural resistance to technology within some healthcare settings hinder widespread adoption of patient-centric care models.

Overcoming these obstacles requires standardized protocols for data exchange, more affordable platform solutions, and demonstrating clear clinical and financial value to all stakeholders.

Explore Full Market Dynamics Analysis Request Free Sample

Personalized Digital Health Platforms Market Segmentation

The personalized digital health platforms industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Component Segment Analysis

The software segment is estimated to witness significant growth during the forecast period.

The software segment is the foundational architecture of the personalized digital health platforms market. This category includes AI-driven health insights, clinical decision support algorithms, and patient engagement platforms that process vast arrays of medical data.

These solutions, often deployed on HIPAA compliant cloud infrastructure, enable the aggregation of biometric data analytics from disparate sources, including electronic health records integration.

Accounting for nearly 47% of the market, software innovation is the primary catalyst for expanding capabilities in personalized care.

As health systems transition toward value-based care models, demand for interoperable software that facilitates secure data exchange and delivers proactive health interventions continues to accelerate, defining the competitive landscape for vendors.

The Software segment was valued at USD 20.92 billion in 2024 and showed a gradual increase during the forecast period.

Personalized Digital Health Platforms Market by Region: North America Leads with 35.5% Growth Share

North America is estimated to contribute 35.5% to the growth of the global market during the forecast period.

The geographic landscape is characterized by varied adoption rates, with North America representing the largest market, contributing over 35% of the global opportunity.

This dominance is driven by high investment in health technology and a mature regulatory environment that supports clinical workflow automation.

Asia is projected to be the fastest-growing region, where the demand for remote diagnostics and proactive disease prevention is surging due to a massive and increasingly health-conscious population.

In Europe, which accounts for over 26% of the market, the focus is on integrating digital platforms into national health systems under strict GDPR compliance for patient data interoperability challenges.

A key factor across all regions is the push for evidence-based digital care and consumer health technology to manage population health more efficiently.

Customer Landscape Analysis for the Personalized Digital Health Platforms Market

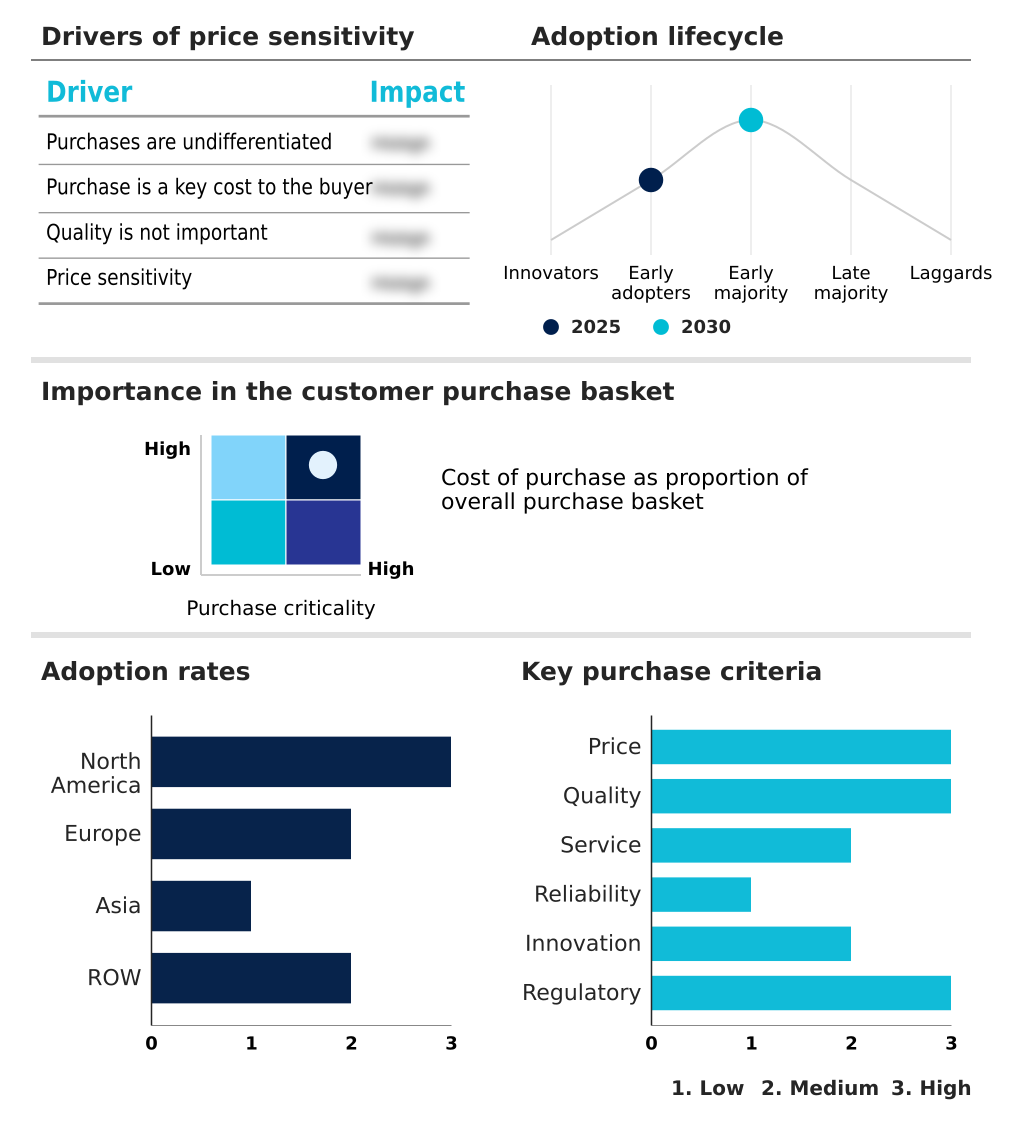

The personalized digital health platforms market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the personalized digital health platforms market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Personalized Digital Health Platforms Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the personalized digital health platforms market industry.

American Well Corp. - Delivers comprehensive telehealth platforms integrating virtual primary care, urgent care, and behavioral health services to enhance personalized patient access and treatment.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- American Well Corp.

- Apple Inc.

- CalmSpace

- Dexcom Inc.

- Fitbit LLC

- Garmin Ltd.

- Google LLC

- Myfitnesspal

- Noom Inc.

- Omada Health Inc.

- Oura Health Oy

- Parsley Health

- Personify Health Inc.

- Segterra Inc.

- Spring Health Inc.

- Teladoc Health Inc.

- Thorne HealthTech Inc.

- Viome Life Sciences, Inc.

- Wild Health

- ZOE Limited

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Personalized Digital Health Platforms Market

- In June, 2025, Hims and Hers Health announced an agreement to acquire the UK-based digital health platform Zava Global GmbH as part of its international expansion strategy.

- In October, 2025, Midi Health announced the raising of $50 million in funding, aimed at accelerating its mission to transform women's healthcare through its AI-enabled, personalized care platform.

- In January, 2026, Spring Health announced its plan to acquire Alma, a move reflecting the accelerating shift toward AI-driven, data-integrated mental healthcare delivery systems.

- In March, 2026, Amazon introduced a new Health AI agent integrated into its website and mobile application, providing users with AI-driven health assistance and round-the-clock access to virtual care.

Research Analyst Overview: Personalized Digital Health Platforms Market

The personalized digital health platforms market's evolution is driven by the operational need for data-driven wellness programs that can function at a population scale. Boardroom decisions on capital allocation are increasingly tied to a platform's ability to facilitate decentralized clinical trials and demonstrate a clear return on investment through improved outcomes in chronic disease management apps.

North America remains the dominant region, and the software segment commands the largest market share, underscoring the criticality of advanced biometric data analytics and AI-driven health insights. A key technical pillar is wearable sensor technology, which provides the continuous, real-time physiological monitoring data essential for predictive health modeling.

Compliance with stringent regulations such as HIPAA necessitates investment in secure data exchange and HIPAA compliant cloud infrastructure. Platforms that successfully integrate genomic data and offer sophisticated digital twin simulation for treatment planning are setting the standard for hyper-personalized nutrition and proactive health interventions, forcing competitors to re-evaluate their R&D priorities.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Personalized Digital Health Platforms Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 22.1% |

| Market growth 2026-2030 | USD 93143.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 20.7% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, The Netherlands, Spain, Russia, China, India, Japan, South Korea, Indonesia, Thailand, Singapore, Australia, Brazil, UAE, Saudi Arabia, South Africa and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Personalized Digital Health Platforms Market: Key Questions Answered in This Report

-

What is the expected growth of the Personalized Digital Health Platforms Market between 2026 and 2030?

-

The Personalized Digital Health Platforms Market is expected to grow by USD 93.14 billion during 2026-2030, registering a CAGR of 22.1%. Year-over-year growth in 2026 is estimated at 20.7%%. This acceleration is shaped by increasing prevalence of chronic diseases and need for continuous monitoring, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, Services, and Hardware), End-user (Healthcare providers, Patients and consumers, Pharma and biotech companies, and Healthcare payers), Application (Monitoring and follow‑up, Preventive care and wellness, Diagnosis and treatment support, and Rehabilitation and recovery) and Geography (North America, Europe, Asia, Rest of World (ROW)). Among these, the Software segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, Asia and Rest of World (ROW). North America is estimated to contribute 35.5% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, UK, Germany, France, Italy, The Netherlands, Spain, Russia, China, India, Japan, South Korea, Indonesia, Thailand, Singapore, Australia, Brazil, UAE, Saudi Arabia, South Africa and Turkey, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is increasing prevalence of chronic diseases and need for continuous monitoring, which is accelerating investment and industry demand. The main challenge is stringent data privacy regulations and complexity of compliance, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Personalized Digital Health Platforms Market?

-

Key vendors include American Well Corp., Apple Inc., CalmSpace, Dexcom Inc., Fitbit LLC, Garmin Ltd., Google LLC, Myfitnesspal, Noom Inc., Omada Health Inc., Oura Health Oy, Parsley Health, Personify Health Inc., Segterra Inc., Spring Health Inc., Teladoc Health Inc., Thorne HealthTech Inc., Viome Life Sciences, Inc., Wild Health and ZOE Limited. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Personalized Digital Health Platforms Market Research Insights

Market dynamics are shaped by demands for evidence-based digital care and patient empowerment tools. As the software segment's contribution to the market is substantially larger than hardware's, focus intensifies on algorithm-based recommendations and sustainable habit formation. Stakeholders must navigate complex data privacy and security frameworks like HIPAA to build trust for sharing user-generated health data.

In practice, an employer deploying a corporate wellness platform must ensure its data aggregation methods for holistic wellness tracking are compliant, using secure health data storage to protect employee privacy.

The drive for interoperable health systems that support personalized care pathways is a critical structural issue, compelling vendors to design platforms that not only deliver clinical value but also integrate seamlessly into existing healthcare IT infrastructure, moving beyond traditional, siloed methods of data management.

We can help! Our analysts can customize this personalized digital health platforms market research report to meet your requirements.

RIA -

RIA -