Packaging Market Size 2026-2030

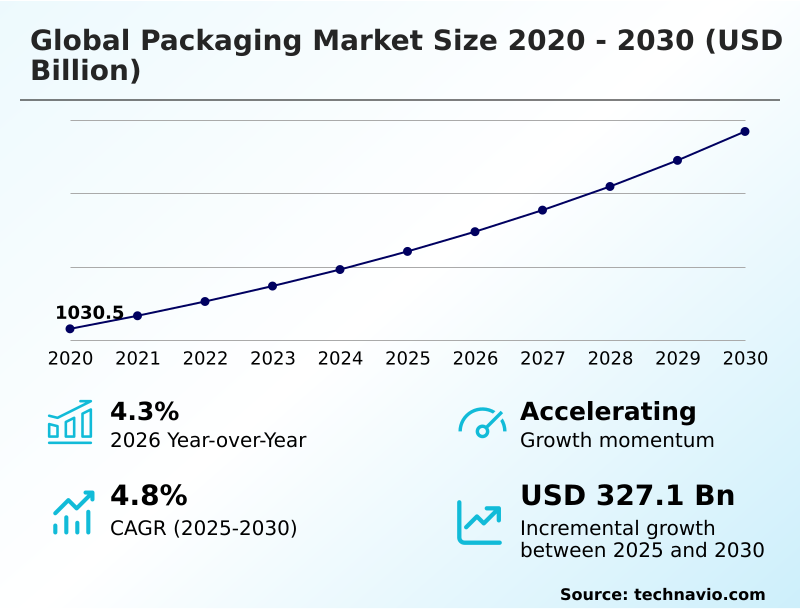

The packaging market size is valued to increase by USD 327.1 billion, at a CAGR of 4.8% from 2025 to 2030. Proliferation of global e-commerce and last-mile logistics efficiency will drive the packaging market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 38.2% growth during the forecast period.

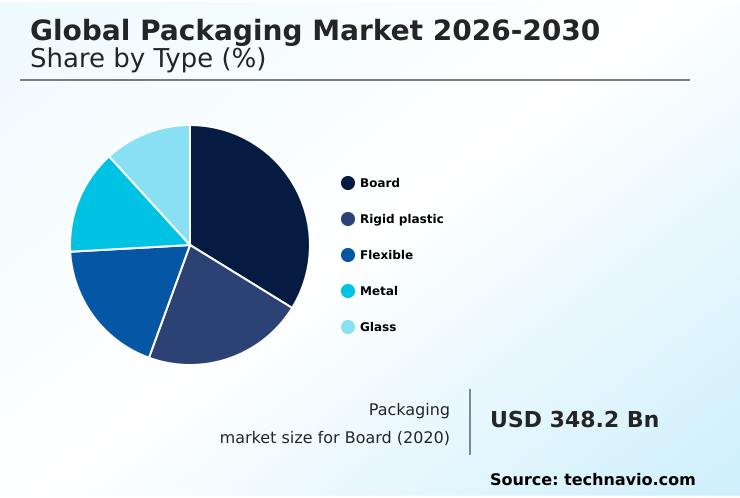

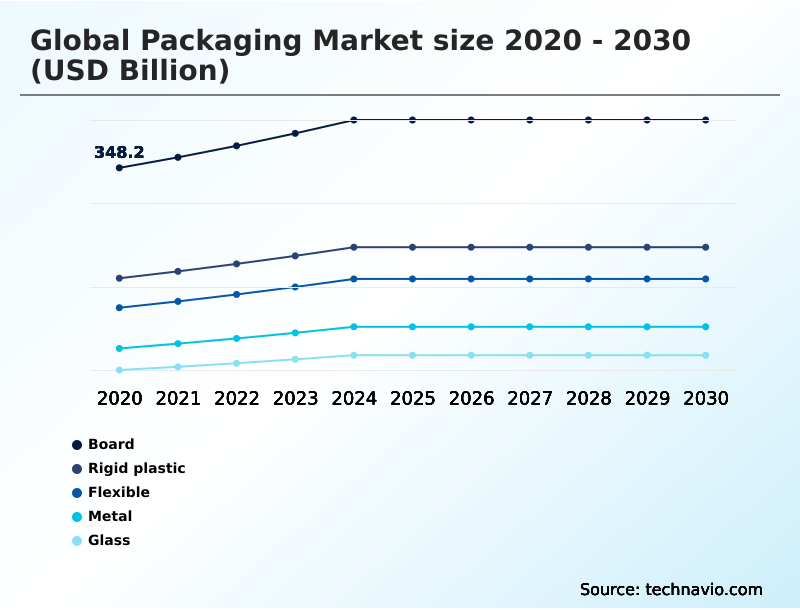

- By Type - Board segment was valued at USD 401.9 billion in 2024

- By End-user - Food segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 538.2 billion

- Market Future Opportunities: USD 327.1 billion

- CAGR from 2025 to 2030 : 4.8%

Market Summary

- The packaging market is navigating a period of profound transformation, balancing the need for e-commerce protective packaging with a strategic pivot toward sustainability. This shift is characterized by a move to mono-material packaging and the integration of post-consumer recycled content, driven by both consumer demand and extended producer responsibility legislation.

- In practice, a food manufacturer may adopt flexible packaging films with enhanced barrier properties to extend product shelf life, while simultaneously using supply chain traceability systems to validate the origin of its bio-based packaging materials. Innovations in digital printing for packaging allow for greater customization, while end-of-line automation enhances operational efficiency.

- However, the industry grapples with the technical challenges of developing food-grade recycled polymers and ensuring that new formats are compatible with existing waste management infrastructure. Success hinges on a holistic approach that marries advanced material science with circular economy principles to create solutions that are both functional and environmentally responsible.

What will be the Size of the Packaging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Packaging Market Segmented?

The packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Board

- Rigid plastic

- Flexible

- Metal

- Glass

- End-user

- Food

- Beverage

- Healthcare

- Personal care

- Others

- Technology

- Flexography

- Offset

- Gravure

- Digital

- Screen

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- Turkey

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Type Insights

The board segment is estimated to witness significant growth during the forecast period.

The board segment, a foundational pillar of the industry, is driven by demand for corrugated board solutions in secondary and tertiary packaging systems. Its versatility and environmental credentials, rooted in renewable sourcing, align with circular economy principles.

This is particularly critical in e-commerce, where lightweighting technologies are essential for optimizing logistics and distribution. The material’s excellent surface for high-quality graphics, achieved through advanced ink and coating formulations, makes it a powerful tool for brand communication.

Continuous R&D efforts are focused on enhancing performance, with advancements in moisture-resistant coatings improving applicability and expanding the use of paperboard in primary packaging design, increasing its adoption by 12% in certain food categories.

The Board segment was valued at USD 401.9 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 38.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Packaging Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the packaging market is defined by varied regional growth and regulatory pressures.

The APAC region is a significant growth engine, contributing 38.15% of the market's incremental growth, driven by demand for flexible packaging films for its expanding food sector.

In contrast, North America and Europe, while representing mature markets, are epicenters of innovation in sustainable packaging solutions and advanced material science.

Growth in South America, at 6.1%, outpaces Europe's 4.1% rate, largely due to the region's focus on bio-based packaging materials derived from its agricultural sector.

Across all regions, the adoption of aseptic carton technology and rigid plastic containers continues, with a strong emphasis on meeting diverse regulatory compliance standards and enhancing brand protection technologies.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic implementation of circular economy models in the packaging industry is reshaping supply chains, particularly for sustainable packaging for food and beverage. This transition necessitates advanced recycling technologies for flexible plastics to effectively process materials and reintroduce them into the production cycle.

- Simultaneously, the impact of raw material volatility on packaging costs is compelling organizations to explore lightweighting strategies for rigid plastic containers and optimize packaging for last-mile delivery. For high-value sectors, meeting pharmaceutical packaging compliance standards is non-negotiable, driving demand for tamper-evident solutions for brand protection and smart packaging for supply chain visibility.

- Robotic automation in secondary packaging lines is becoming standard, with some companies reporting a threefold reduction in packing errors compared to manual processes. This focus on automation is also seen in packaging design for automated filling lines. The push for sustainability also involves a cost-benefit analysis of returnable packaging and the development of bio-based alternatives to petroleum plastics.

- The widespread adoption of mono-material solutions for improved recyclability and high-barrier films for perishable food preservation addresses both environmental and functional requirements.

- As e-commerce packaging for fragile goods becomes more sophisticated, digital printing for personalized consumer packaging offers new avenues for brand engagement, all while navigating the complexities of extended producer responsibility scheme implementation and the challenges in incorporating post-consumer recycled content in aseptic packaging systems for liquid products.

What are the key market drivers leading to the rise in the adoption of Packaging Industry?

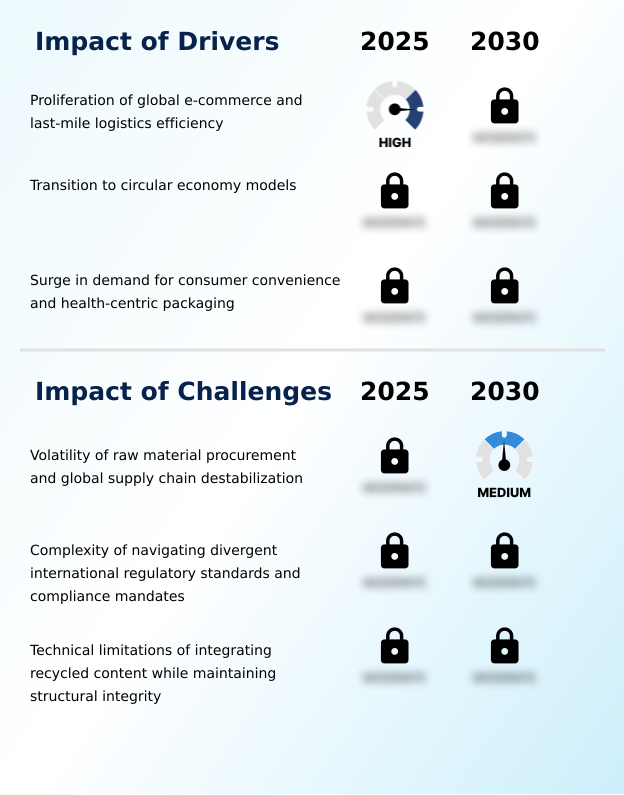

- The proliferation of global e-commerce and the corresponding need for last-mile logistics efficiency serves as a key driver for market growth.

- Market growth is significantly driven by the expansion of e-commerce, which has amplified the need for robust secondary packaging optimization and efficient logistics and distribution networks. This has spurred innovation in corrugated board solutions designed for transit.

- Simultaneously, the global shift towards a circular economy has become a primary catalyst, promoting the use of post-consumer recycled content and returnable packaging systems.

- This driver has accelerated advancements in waste management infrastructure, with some regions improving plastic bottle collection rates by up to 30%.

- Consumer demand for convenience and health is also crucial, fueling the development of rigid plastic containers with consumer convenience features and advanced dispensing closure systems.

What are the market trends shaping the Packaging Industry?

- The integration of Packaging 4.0 principles, including advanced smart monitoring systems, is emerging as a transformative market trend.

- Key trends reshaping the market include the adoption of smart packaging integration and end-of-line automation, which together are reducing processing errors by over 25% in high-volume facilities. The rise of hyper-personalization, enabled by digital printing for packaging, allows for custom packaging production at scale, significantly reducing time-to-market compared to conventional methods.

- The push for sustainability is driving innovation in heat-sealable coatings and flexible forming films, which contribute to lightweighting efforts. Furthermore, the industrial shift towards Packaging 4.0 is fostering a connected ecosystem where e-commerce protective packaging and aseptic carton technology are optimized in real-time, improving supply chain efficiency and product safety.

What challenges does the Packaging Industry face during its growth?

- Volatility in raw material procurement and global supply chain destabilization present a key challenge to industry growth.

- A primary challenge remains raw material volatility, where unpredictable price swings can increase production costs by as much as 20% in a single quarter, disrupting material sourcing strategies. This instability is compounded by a fragmented global regulatory landscape, creating complexities around regulatory compliance standards and extended producer responsibility mandates.

- Furthermore, technical limitations in chemical recycling processes and the integration of food-grade recycled polymers present significant hurdles. Achieving the desired performance in high-barrier packaging films while using recycled materials requires breakthroughs in multi-layer film coextrusion and substrate compatibility, presenting ongoing R&D challenges for the industry.

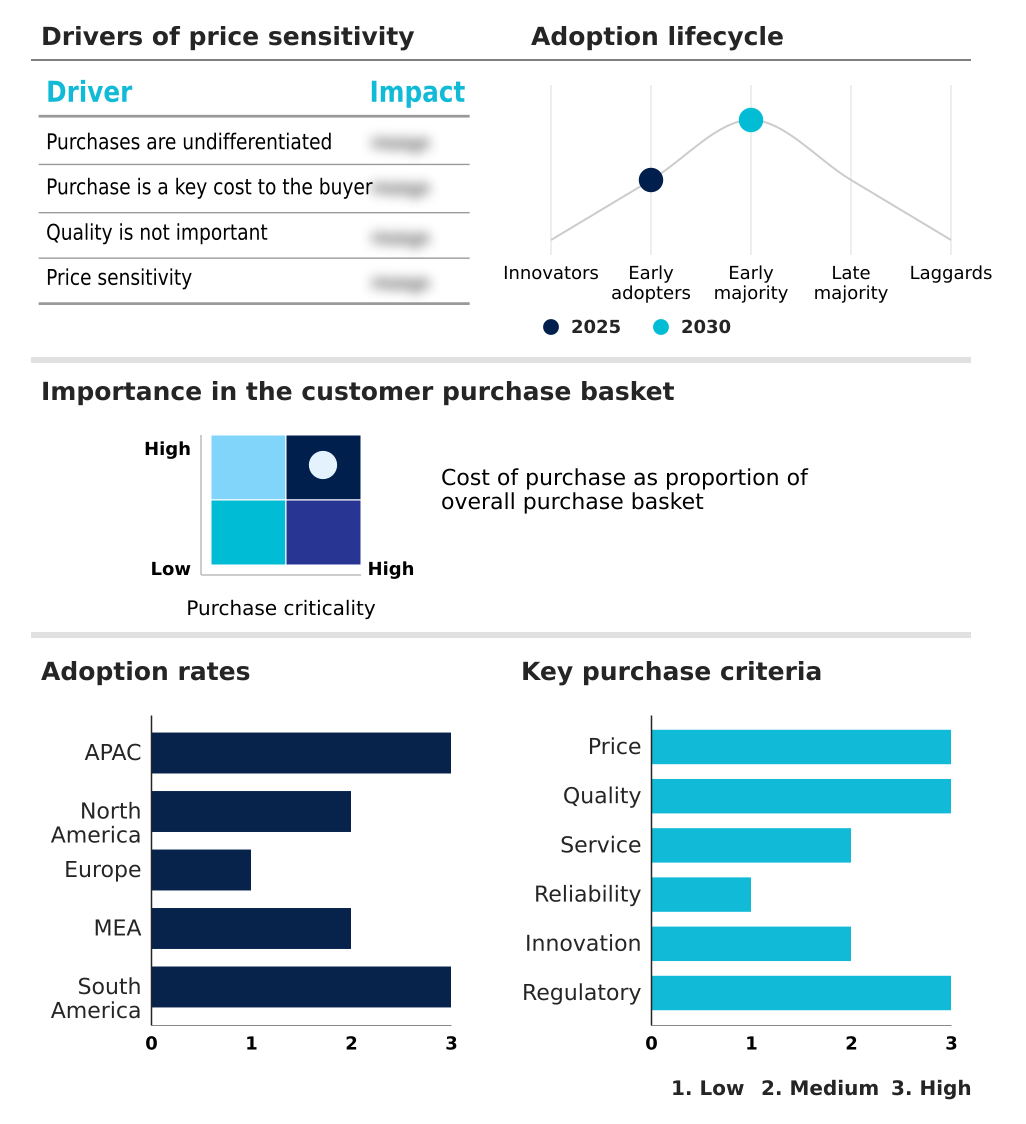

Exclusive Technavio Analysis on Customer Landscape

The packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Packaging Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amcor Plc - Key offerings include a diverse range of rigid and flexible packaging formats, specialty cartons, and closure systems tailored for the food, beverage, healthcare, and personal care sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- AptarGroup Inc.

- Ball Corp.

- CCL Industries Inc.

- Constantia Flexibles GmbH

- Crown Holdings Inc.

- DS Smith Plc

- Gerresheimer AG

- Graphic Packaging Holding Co.

- Greif Inc.

- Huhtamaki Oyj

- International Paper Co.

- Mondi Plc

- O I Glass Inc.

- Sealed Air Corp.

- SIG Group AG

- Silgan Holdings Inc.

- Smurfit Westrock plc

- Sonoco Products Co.

- Stora Enso Oyj

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Packaging market

- In September 2024, Mondi Plc announced a significant investment in its production lines to scale the output of its new mono-material pouch technology, designed to be fully recyclable while maintaining high-barrier properties for food applications.

- In November 2024, Smurfit Westrock plc initiated a large-scale deployment of advanced robotic automation and AI-powered vision systems across its North American corrugated packaging plants, targeting a 15% increase in throughput and enhanced quality control.

- In January 2025, SIG Group AG formalized a strategic partnership with the Ellen MacArthur Foundation to advance circular packaging systems, focusing on minimizing industrial waste and enhancing the recyclability of liquid cartons.

- In April 2025, Amcor Plc completed its acquisition of Berry Global Group Inc., creating a combined entity focused on high-growth categories like healthcare and specialty nutrition and aiming to scale the production of innovative, sustainable dispensing solutions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Packaging Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 323 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.8% |

| Market growth 2026-2030 | USD 327.1 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.3% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, Turkey, South Africa, Israel, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The packaging market is undergoing a structural realignment, driven by the dual mandates of sustainability and technological advancement. Boardroom decisions are increasingly focused on Capex for robotic process automation and R&D for bio-based packaging materials.

- The adoption of circular economy principles is no longer a peripheral concern but a core strategic driver, compelling a re-evaluation of the entire value chain, from raw material inputs to end-of-life management. We see a clear trend in the adoption of mono-material packaging and aseptic filling systems, which simplifies recycling and improves efficiency.

- For instance, companies investing in high-barrier packaging films that are also recyclable have seen a 10% improvement in market penetration within environmentally conscious segments. The integration of tamper-evident features and supply chain traceability is now standard for high-value goods, while the development of food-grade recycled polymers and chemical recycling processes addresses key sustainability hurdles.

- This landscape requires a multi-faceted approach, balancing innovations in dispensing closure systems, multi-layer film coextrusion, and modified atmosphere packaging with the practicalities of cold chain logistics.

What are the Key Data Covered in this Packaging Market Research and Growth Report?

-

What is the expected growth of the Packaging Market between 2026 and 2030?

-

USD 327.1 billion, at a CAGR of 4.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Board, Rigid plastic, Flexible, Metal, and Glass), End-user (Food, Beverage, Healthcare, Personal care, and Others), Technology (Flexography, Offset, Gravure, Digital, and Screen) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of global e-commerce and last-mile logistics efficiency, Volatility of raw material procurement and global supply chain destabilization

-

-

Who are the major players in the Packaging Market?

-

Amcor Plc, AptarGroup Inc., Ball Corp., CCL Industries Inc., Constantia Flexibles GmbH, Crown Holdings Inc., DS Smith Plc, Gerresheimer AG, Graphic Packaging Holding Co., Greif Inc., Huhtamaki Oyj, International Paper Co., Mondi Plc, O I Glass Inc., Sealed Air Corp., SIG Group AG, Silgan Holdings Inc., Smurfit Westrock plc, Sonoco Products Co. and Stora Enso Oyj

-

Market Research Insights

- Market dynamics are increasingly shaped by the pursuit of operational efficiency gains and supply chain resilience. The adoption of returnable packaging systems is growing, showing a 15% higher asset utilization rate compared to single-use alternatives in closed-loop systems. Meanwhile, advanced material science is enabling the development of flexible forming films that use 20% less raw material without compromising strength.

- Custom packaging production, facilitated by digital transformation in packaging, allows for rapid response to consumer demand. These shifts underscore a move toward integrated solutions that optimize the entire packaging lifecycle assessment, from material sourcing strategies to compatibility with evolving waste management infrastructure.

We can help! Our analysts can customize this packaging market research report to meet your requirements.

RIA -

RIA -