Maritime Emissions Monitoring Systems Market Size and Growth Forecast 2026-2030

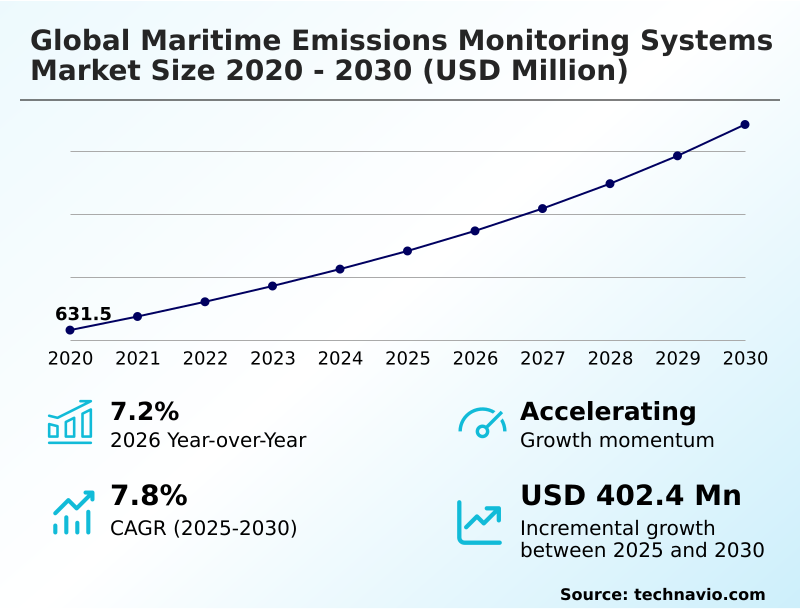

The Maritime Emissions Monitoring Systems Market size was valued at USD 883.3 million in 2025 growing at a CAGR of 7.8% during the forecast period 2026-2030.

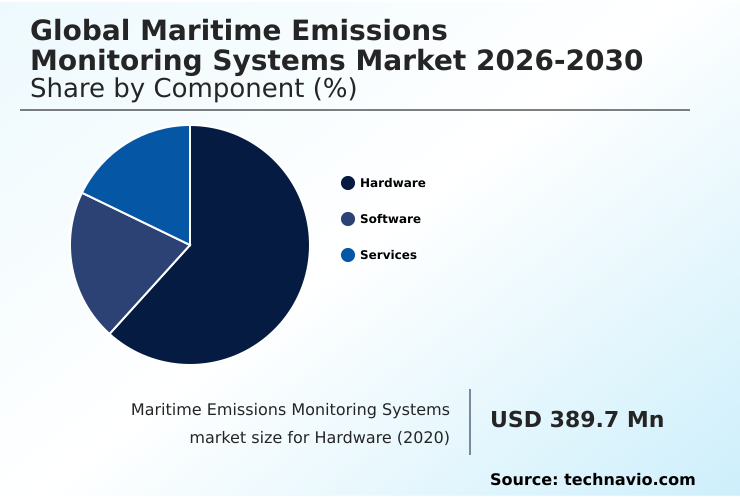

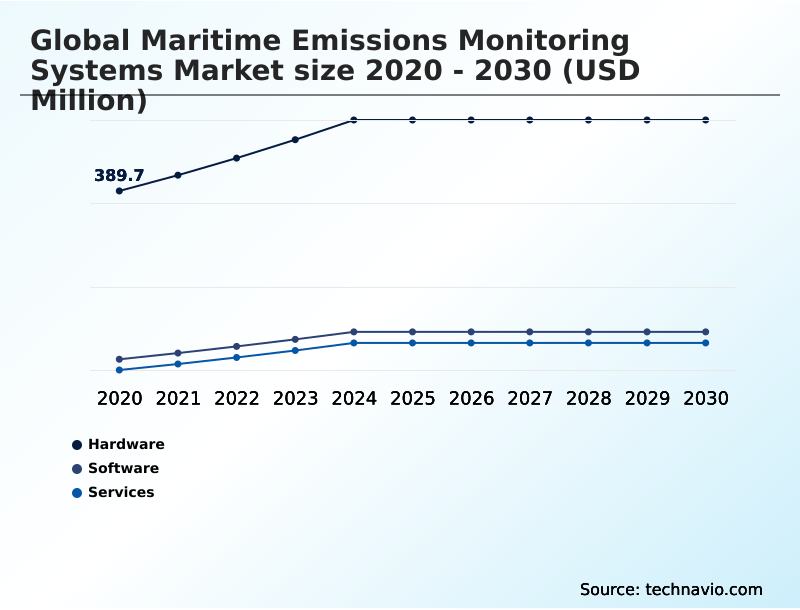

APAC accounts for 35.1% of incremental growth during the forecast period. The Hardware segment by Component was valued at USD 499.5 million in 2024, while the Continuous emissions monitoring systems segment holds the largest revenue share by Technology.

The market is projected to grow by USD 654.2 million from 2020 to 2030, with USD 402.4 million of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Maritime Emissions Monitoring Systems Market Overview

The maritime emissions monitoring systems market is expanding as regulatory mandates and ESG pressures converge, making emissions data a critical operational asset. With APAC poised to contribute significantly to incremental growth, the industry is shifting from compliance as a cost center to data-driven optimization. A tangible example is a global container line retrofitting its fleet with continuous emissions monitoring system technology. By integrating Coriolis flow meter data with gas analyzer outputs, the company achieves precise fuel consumption monitoring. This real-time data acquisition feeds into a vessel performance optimization platform, which uses digital twin simulation to recommend voyage adjustments. This not only ensures nitrogen oxide compliance with MARPOL Annex VI but also improves the vessel's carbon intensity indicator rating, unlocking preferential financing under the Poseidon Principles and satisfying shipper demands for scope 3 emissions reporting. This illustrates the move from basic monitoring to a holistic environmental performance strategy.

Drivers, Trends, and Challenges in the Maritime Emissions Monitoring Systems Market

Navigating the complexities of maritime decarbonization requires a multi-faceted approach to emissions monitoring. For vessels equipped with scrubbers, CEMS integration for marine exhaust scrubbers is non-negotiable for proving compliance with MARPOL Annex VI sulfur oxide limits.

In contrast, the adoption of transitional fuels necessitates sophisticated software solutions, where PEMS for dual-fuel engine NOx prediction offers a less hardware-intensive method for ensuring nitrogen oxide compliance. A critical operational challenge is maintaining data integrity through routine onboard sensor calibration for SOx compliance, a process that is increasingly being streamlined via remote verification services.

The most significant strategic shift involves leveraging this data for efficiency gains; through AI-driven fuel optimization with emission data, operators can reduce fuel consumption by several percentage points compared to conventional noon-reporting methods.

Finally, from a regulatory standpoint, remote sensing for ECA enforcement, using technologies like airborne "sniffer" drones, acts as an external check, compelling the industry to maintain accurate onboard systems and ensuring a level playing field.

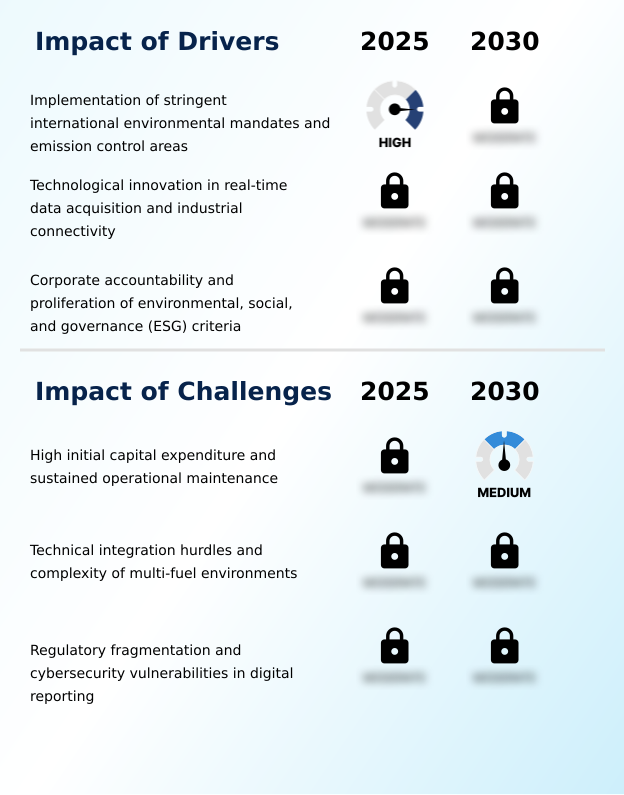

Primary Growth Driver: The implementation of stringent international environmental mandates and the designation of new emission control areas are the key drivers for market growth.

Market growth is fundamentally propelled by a stringent global regulatory framework and increasing pressure for corporate accountability.

The designation of new Emission Control Areas (ECAs) mandates adherence to strict sulfur oxide limits and drives investment in continuous emissions monitoring system technology.

Beyond compliance, the proliferation of environmental social and governance criteria pressures operators to provide verifiable data for scope 3 emissions reporting.

This market-based driver makes the installation of systems for fuel consumption monitoring and ensuring nitrogen oxide compliance a strategic financial advantage, especially as financiers link loan terms to environmental performance through frameworks like the Poseidon Principles.

These factors create a mandatory market for technologies enabling transparent and automated high-frequency data reporting.

Emerging Market Trend: The integration of AI and machine learning for predictive emissions analysis represents a significant upcoming market trend. This evolution is shifting the industry from reactive data logging to proactive environmental management.

Market evolution is characterized by the integration of AI and machine learning, transitioning from reactive data logging to proactive environmental management. A key trend is the use of a predictive emissions monitoring system to anticipate compliance breaches and optimize the carbon intensity indicator rating. For vessels with a dual-fuel engine, advanced algorithms now enable more precise methane slip measurement.

This software-defined approach is also expanding to include a predictive maintenance module, reducing operational costs by optimizing sensor calibration schedules. The development of digital twin simulation allows operators to model voyage emissions under various conditions, enhancing vessel performance optimization and supporting long-term decarbonization strategies in alignment with the IMO's GHG reduction targets.

Key Industry Challenge: The high initial capital expenditure required for system procurement, coupled with the costs of sustained operational maintenance, presents a key challenge affecting industry growth.

Key market challenges center on technical complexity and cost. The high initial capital expenditure for a high-precision continuous emissions monitoring system is a significant barrier, especially for smaller operators. Integrating diverse sensor arrays, including a specialized electrochemical sensor for new fuels like ammonia, into legacy vessel systems presents considerable technical hurdles.

The transition to a multi-fuel future complicates the landscape, as the chemical composition of exhaust from a dual-fuel engine is more difficult to measure accurately.

Furthermore, the increasing reliance on digital reporting platforms introduces significant cybersecurity risks, demanding robust data encryption and blockchain-secured monitoring to prevent tampering, especially when data is tied to carbon pricing mechanisms under regulations like the EU ETS.

Explore Full Market Dynamics Analysis Request Free Sample

Maritime Emissions Monitoring Systems Market Segmentation

The maritime emissions monitoring systems industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Component Segment Analysis

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment, which accounted for a majority of the market in 2025, includes the essential physical instruments for emissions verification.

Procurement decisions are driven by the need for robust components like a gas analyzer and sample conditioning unit that can withstand harsh marine environments.

The adoption of an exhaust gas cleaning system or a selective catalytic reduction unit necessitates corresponding hardware for compliance validation. For instance, non-dispersive infrared technology is frequently employed for CO2 and SOx analysis.

The reliability of each particulate matter sensor and multi-gas sampling probe is critical, as equipment failure directly impacts a vessel's ability to operate within regulated emission control areas established under MARPOL Annex VI.

The Hardware segment was valued at USD 499.5 million in 2024 and showed a gradual increase during the forecast period.

Maritime Emissions Monitoring Systems Market by Region: APAC Leads with 35.1% Growth Share

APAC is estimated to contribute 35.1% to the growth of the global market during the forecast period.

The geographic landscape is shaped by regional regulatory intensity, with Europe and APAC being key markets. APAC, contributing over 35% of incremental growth, is driven by its shipbuilding dominance and the implementation of domestic emission control areas in China.

In this region, new build specifications frequently include integrated systems for methane slip measurement from the outset.

Europe remains a regulatory vanguard, where the EU Emissions Trading System and FuelEU Maritime regulation compel investment in technologies enabling automated high-frequency data sharing.

North America's market, representing about 21% of the opportunity, focuses on green shipping corridors and local air quality, driving demand for advanced particulate matter sensor technology and systems that provide a remote verification service to satisfy both port authorities and ESG-focused cargo owners.

Customer Landscape Analysis for the Maritime Emissions Monitoring Systems Market

The maritime emissions monitoring systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the maritime emissions monitoring systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Maritime Emissions Monitoring Systems Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the maritime emissions monitoring systems market industry.

ABB Ltd. - Provides maritime emissions monitoring systems for real-time gas pollutant measurement, supporting decarbonization and regulatory compliance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Danfoss AS

- DNV Group AS

- Emerson Electric Co.

- ENVEA

- Fuji Electric Co. Ltd.

- Honeywell International Inc.

- HORIBA Ltd.

- Kongsberg Gruppen ASA

- KROHNE Group

- Mettler Toledo Inc.

- Parker Hannifin Corp.

- Rockwell Automation Inc.

- Servomex Group Ltd.

- SICK AG

- Siemens AG

- Teledyne Technologies Inc.

- Testo SE and Co. KGaA

- Vaisala Oyj

- Wartsila Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Maritime Emissions Monitoring Systems Market

- In August, 2024, HMM announced the completion of an extensive sensor installation program across its container fleet to provide real-time emissions data to its global customers, prompted by demand from large retail and industrial clients.

- In March, 2025, ABB Marine and Ports launched an enhanced digital emissions suite that utilizes advanced sensors for real-time carbon dioxide and methane slip measurements with unprecedented accuracy.

- In April, 2025, the International Maritime Organization approved new guidelines during the eighty-third session of the Marine Environment Protection Committee that specifically target methane slip from gas-fueled engines.

- In May, 2025, the European Commission implemented a new digital registry requiring all data for the MRV system to be timestamped and encrypted using distributed ledger technology.

Research Analyst Overview: Maritime Emissions Monitoring Systems Market

The maritime emissions monitoring systems market is undergoing a fundamental shift from a hardware-centric compliance function to a software-driven strategic asset. While the hardware segment, including the core gas analyzer and sample conditioning unit, still represents the largest portion of the market, the true value is migrating to data analytics.

Boardroom decisions now hinge on optimizing a vessel's carbon intensity indicator rating, a metric directly influenced by data from these systems. A key development is the use of laser absorption spectroscopy in new optical sensor designs for precise methane slip measurement on vessels with a dual-fuel engine. This technology is critical for operators investing in LNG as a transitional fuel.

The move towards alternative fuels also drives demand for advanced sensor technologies like the electrochemical sensor for ammonia and robust particulate matter sensor technology.

The ability to integrate and interpret data from a continuous emissions monitoring system or a predictive emissions monitoring system is now a primary determinant of a fleet's commercial viability and its ability to meet tightening IMO 2023 GHG Strategy targets.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Maritime Emissions Monitoring Systems Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 309 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.8% |

| Market growth 2026-2030 | USD 402.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.2% |

| Key countries | Germany, UK, France, Italy, Spain, Russia, China, Japan, South Korea, India, Australia, Indonesia, US, Canada, Mexico, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Egypt and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Maritime Emissions Monitoring Systems Market: Key Questions Answered in This Report

-

What is the expected growth of the Maritime Emissions Monitoring Systems Market between 2026 and 2030?

-

The Maritime Emissions Monitoring Systems Market is expected to grow by USD 402.4 million during 2026-2030, registering a CAGR of 7.8%. Year-over-year growth in 2026 is estimated at 7.2%%. This acceleration is shaped by implementation of stringent international environmental mandates and emission control areas, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, and Services), Technology (Continuous emissions monitoring systems, Predictive emissions monitoring systems, Remote sensing systems, and Others), End-user (Commercial ships, Passenger ships, and Others) and Geography (Europe, APAC, North America, South America, Middle East and Africa). Among these, the Hardware segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers Europe, APAC, North America, South America and Middle East and Africa. APAC is estimated to contribute 35.1% to market growth during the forecast period. Country-level analysis includes Germany, UK, France, Italy, Spain, Russia, China, Japan, South Korea, India, Australia, Indonesia, US, Canada, Mexico, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Egypt and Turkey, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is implementation of stringent international environmental mandates and emission control areas, which is accelerating investment and industry demand. The main challenge is high initial capital expenditure and sustained operational maintenance, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Maritime Emissions Monitoring Systems Market?

-

Key vendors include ABB Ltd., Danfoss AS, DNV Group AS, Emerson Electric Co., ENVEA, Fuji Electric Co. Ltd., Honeywell International Inc., HORIBA Ltd., Kongsberg Gruppen ASA, KROHNE Group, Mettler Toledo Inc., Parker Hannifin Corp., Rockwell Automation Inc., Servomex Group Ltd., SICK AG, Siemens AG, Teledyne Technologies Inc., Testo SE and Co. KGaA, Vaisala Oyj and Wartsila Corp.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Maritime Emissions Monitoring Systems Market Research Insights

Market dynamics are increasingly shaped by the need for verifiable data to meet both regulatory and commercial demands. While North America accounts for over 20% of the market, driven by strict Emission Control Area enforcement of sulfur oxide limits, the pressure from environmental social and governance criteria is a global force.

Charterers and financiers now demand access to granular vessel data, making systems that provide a remote verification service and automated high-frequency data essential for securing contracts. For instance, operators of vessels with a dual-fuel engine must provide accurate methane slip measurement data, a task requiring advanced sensor technology.

This shift transforms monitoring from a simple compliance tool into a key element of vessel performance optimization and a prerequisite for accessing green finance and premium cargo.

We can help! Our analysts can customize this maritime emissions monitoring systems market research report to meet your requirements.

RIA -

RIA -