Marine Loading Arms Market Size 2026-2030

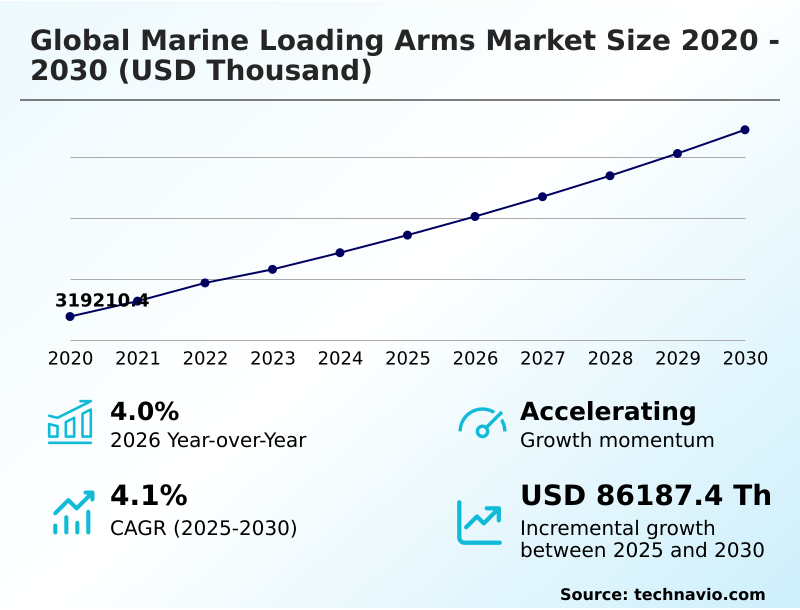

The Marine Loading Arms Market size was valued at USD 385.81 million in 2025, growing at a CAGR of 4.1% during the forecast period 2026-2030.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 36.9% growth during the forecast period.

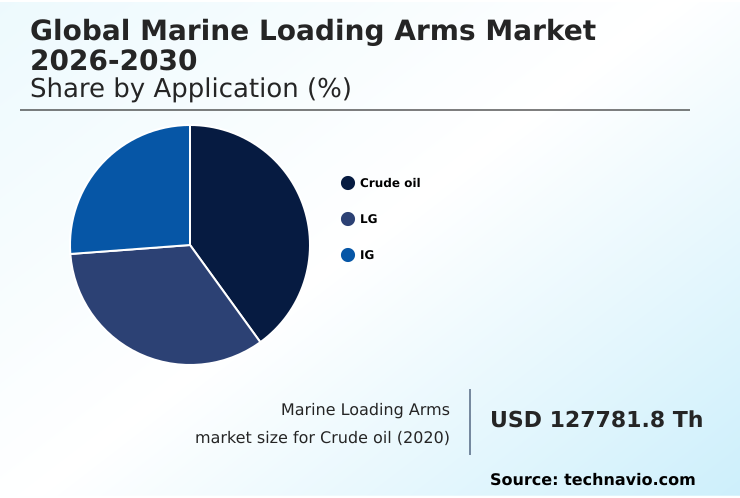

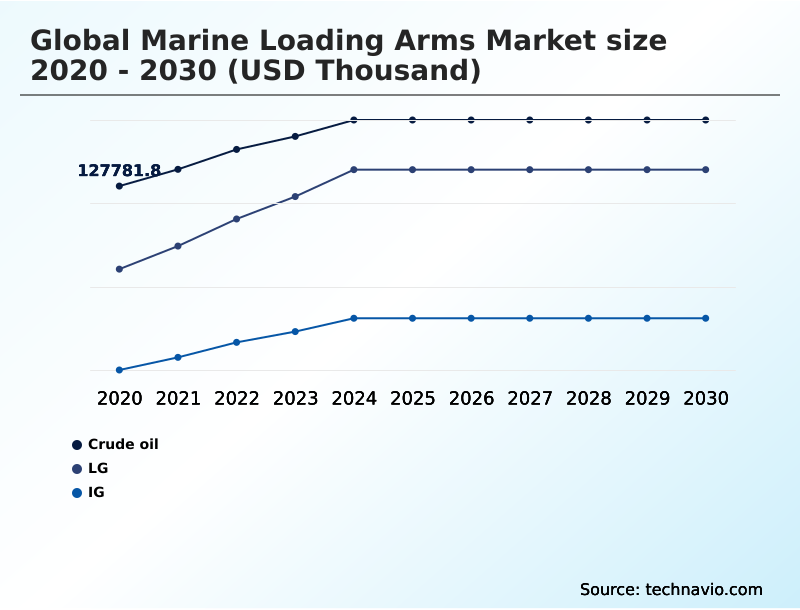

- By Application - Crude oil segment was valued at USD 143.66 million in 2024

- By Type - Manual marine loading arms segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024:

- Market Future Opportunities 2025-2030: USD 86.19 million

- CAGR from 2025 to 2030 : 4.1%

Market Summary

- The marine loading arms market is defined by its critical role in energy and chemical logistics, where hydraulic systems now represent over 45% of new installations. These systems provide a more than 30% improvement in connection speed compared to manual marine loading arm counterparts, directly enhancing terminal throughput.

- A primary driver is the global expansion of LNG transfer infrastructure, demanding advanced cryogenic loading arm technology to support the energy transition. Operations often involve complex vessel motion dynamics, requiring sophisticated motion compensation to ensure a safe operating envelope.

- However, the market faces a significant challenge from the volatility in crude oil prices, which can delay capital expenditure on new port infrastructure and modernization projects, impacting manufacturer order books and supply chain logistics.

What will be the Size of the Marine Loading Arms Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Marine Loading Arms Market Segmented?

The marine loading arms industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Crude oil

- LG

- IG

- Type

- Manual marine loading arms

- Hydraulic marine loading arms

- Method

- Top loading

- Bottom Loading

- Material

- Carbon steel

- Stainless steel

- Aluminum

- Others

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- The Netherlands

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

How is the Marine Loading Arms Market Segmented by Application?

The crude oil segment is estimated to witness significant growth during the forecast period.

The crude oil segment, which accounts for over 35% of all applications, remains the foundational application for marine loading arms.

These systems are engineered for the high-volume transfer of petroleum, requiring large nominal bore diameters, typically 20% greater than those used for chemical transfers, to maximize terminal throughput.

The construction relies on robust carbon steel to handle operational pressures and the abrasive nature of raw petroleum.

Modern designs incorporate advanced vapor recovery systems and emergency release systems (ERS), which mitigate fugitive emissions and improve disconnection safety by over 99%, meeting stringent environmental and port infrastructure regulations.

This focus on safety and efficiency is critical for maintaining asset integrity in high-consequence cargo handling operations.

The Crude oil segment was valued at USD 143.66 million in 2024 and showed a gradual increase during the forecast period.

How demand for the Marine Loading Arms market is rising in the leading region?

APAC is estimated to contribute 36.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Marine Loading Arms Market demand is rising in APAC Request Free Sample

The geographic landscape of the marine loading arms market is led by APAC, which is projected to contribute 37% of the market's incremental growth, outpacing North America's 31% share.

This dominance is fueled by massive port infrastructure investments in countries like China and India, whose energy demands are driving the construction of new LNG import terminals and petrochemical handling facilities.

In contrast, the market in Europe, which accounts for approximately 16% of growth, is primarily driven by retrofitting and modernization projects focused on regulatory compliance and enhancing terminal throughput.

North America's growth is concentrated in the US Gulf Coast, where a boom in hydrocarbon infrastructure for LNG and crude oil exports necessitates new installations of high-capacity hydraulic marine loading arms.

This regional difference in drivers—new builds in APAC versus upgrades in Europe—shapes global supply chain logistics and sales strategies.

What are the key Drivers, Trends, and Challenges in the Marine Loading Arms Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Terminal operators evaluating the total cost of marine loading arm installation must consider factors beyond the initial purchase price, including long-term operational efficiency and asset integrity. The decision between a manual loading arm and a hydraulic marine loading arm often hinges on terminal throughput requirements and safety protocols, with hydraulic systems offering a 25% faster connection time on average.

- For facilities handling LNG transfer, the selection of a cryogenic marine loading arm for LNG transfer is non-negotiable, requiring specialized materials and swivel joint technology to handle extreme temperatures. Proper marine loading arm maintenance and inspection are critical to prevent spills and ensure regulatory compliance, forming a significant part of the lifecycle cost.

- Furthermore, integrating motion compensating systems for offshore loading is essential for operations in challenging sea conditions, ensuring a safe operating envelope and protecting both equipment and personnel. Understanding the specific safety features of hydraulic marine loading arms, such as the emergency release system (ERS), is paramount for risk management in all hazardous fluid transfer scenarios.

- These considerations are fundamental to modern port modernization and hydrocarbon infrastructure projects.

What are the key market drivers leading to the rise in the adoption of Marine Loading Arms Industry?

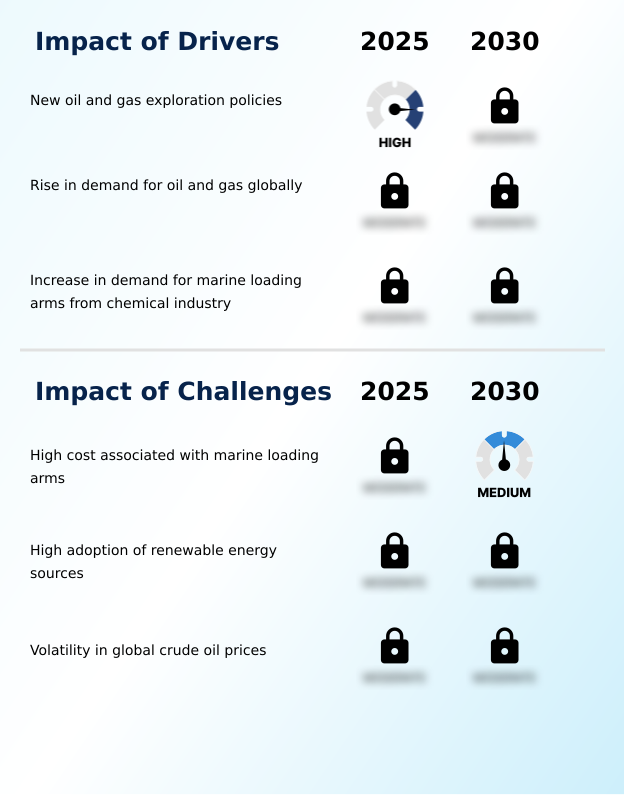

- New oil and gas exploration policies are a key driver for the market, stimulating investment in hydrocarbon infrastructure and increasing the demand for efficient fluid transfer equipment.

- Rising global energy demand is a primary driver, with projections indicating a more than 700,000 barrel-per-day increase in oil consumption, directly boosting the need for efficient fluid transfer equipment.

- This surge necessitates significant investment in port modernization and new hydrocarbon infrastructure to expand cargo handling capacity.

- Simultaneously, the chemical industry's expansion, particularly in APAC, is projected to grow by 5-6% annually, fueling demand for specialized loading arms for petrochemical handling.

- The growing international trade in LNG, driven by the global push for cleaner energy transition fuels, requires a substantial build-out of terminals equipped with advanced cryogenic loading arm technology.

- This confluence of demand from the oil, gas, and chemical sectors underpins the sustained need for new marine transfer systems globally.

What are the market trends shaping the Marine Loading Arms Industry?

- The advent of motion-recognizing marine loading arms represents a significant market trend. This innovation is driven by the increasing need for enhanced safety and operational efficiency during fluid transfer.

- The market is shifting toward intelligent and flexible fluid transfer equipment, with motion-recognizing marine loading arms delivering over 20% improvements in operational efficiency. This trend is driven by the need to manage complex vessel motion dynamics during LNG transfer, where automated positioning can reduce connection time by up to 30%.

- The emergence of mobile marine loading arms provides enhanced flexibility for jetty operations, allowing for quicker adaptation to different cargo handling needs without fixed port infrastructure. Innovations focus on integrating remote diagnostics and a robust counterweight system to improve safety and simplify preventive maintenance.

- These advancements in terminal automation are critical for operators looking to improve terminal throughput and ensure a safe operating envelope, especially in FLNG applications and bunkering operations.

What challenges does the Marine Loading Arms Industry face during its growth?

- The high initial capital investment and long-term maintenance costs associated with marine loading arms present a significant challenge to market growth, particularly for smaller terminal operators.

- The high cost associated with marine loading arms, with prices for a single hydraulic unit ranging from USD 50,000 to over USD 250,000, presents a significant barrier to adoption for many operators. This capital expenditure is often 3-4 times higher than that for flexible hose alternatives, although the lifecycle cost and safety benefits differ.

- Price volatility in the crude oil market creates further challenges, as a sudden downturn can lead to the deferral of up to 40% of planned capital projects for port infrastructure upgrades, directly impacting manufacturers' order pipelines.

- This financial uncertainty complicates long-term investment in advanced technologies like the articulated arm or systems with integrated motion compensation, forcing operators to balance immediate costs against long-term operational efficiency and regulatory compliance requirements.

Exclusive Technavio Analysis on Customer Landscape

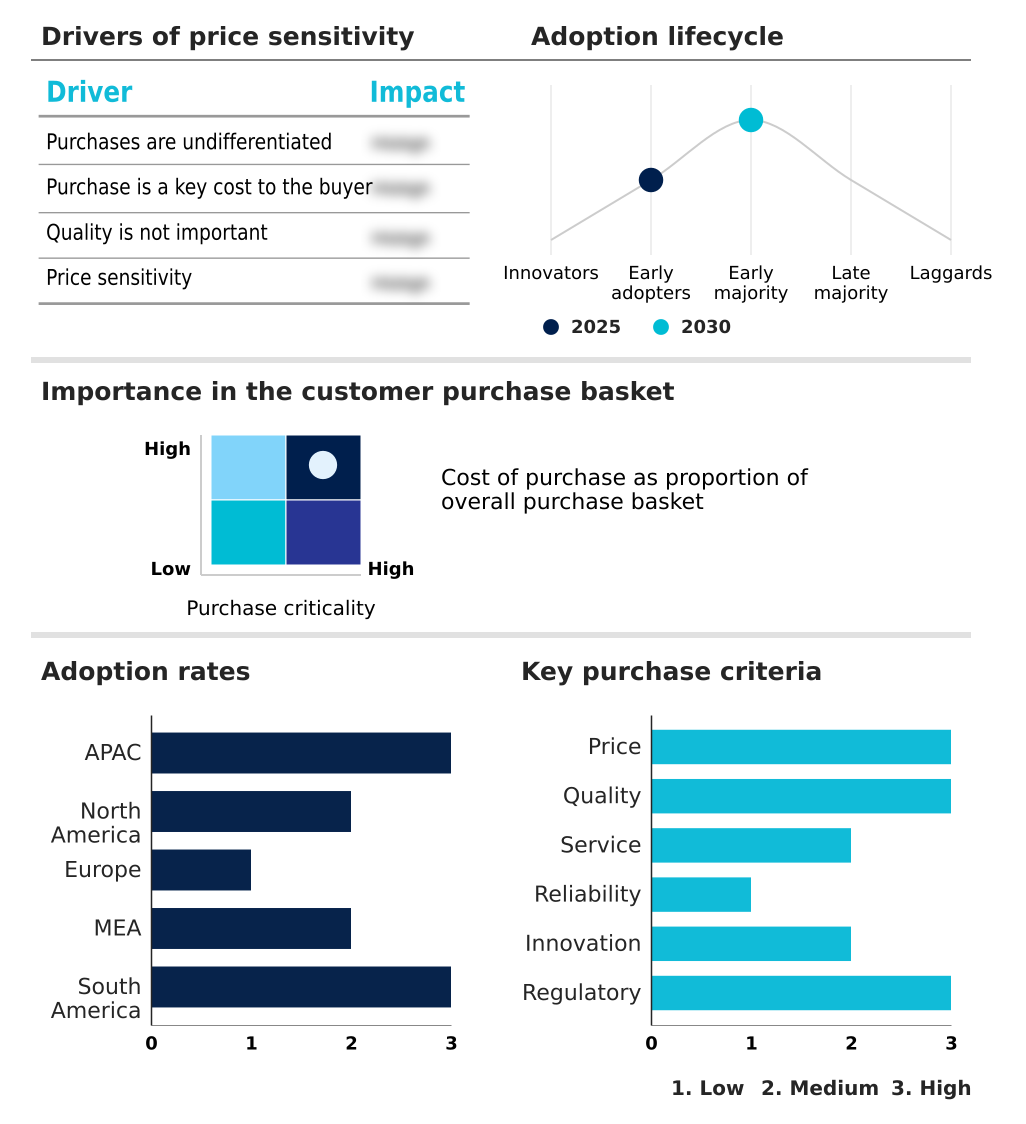

The marine loading arms market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the marine loading arms market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Marine Loading Arms Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, marine loading arms market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Baretti - Provides specialized fluid transfer equipment and integrated arm systems, including the 400 Series, engineered for industrial loading and precision fluid management applications across multiple sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Baretti

- Carbis Loadtec Group

- Flotech Performance Systems

- Ingersoll Rand Inc.

- J de Jonge Group

- Jiangsu Changlong Co. Ltd.

- JRE Pvt. Ltd.

- KANON Loading Equipment BV

- Lianyungang HUADE Co. Ltd.

- Lloyds Steel Industries Ltd.

- OGCF Engineering M Sdn Bhd.

- OPW Engineered Systems

- Safe Harbor Access Systems

- SVT APAC Pte. Ltd.

- TB Global Technologies Ltd.

- TechnipFMC plc

- WLT liquid and gas BV

- Woodfield Systems

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Marine Transportation industry, the accelerated adoption of Liquefied Natural Gas (LNG) as a primary marine fuel has directly increased demand for specialized cryogenic marine loading arms. This shift, driven by the need to comply with stricter emissions standards, necessitates new bunkering operations infrastructure at major ports, creating a high-value niche for equipment capable of handling cryogenic fluid.

- Stringent international regulations, such as the International Maritime Organization's (IMO) mandates on sulfur emissions, have forced a focus on cleaner fuels and advanced vapor recovery systems. This regulatory compliance push is a primary driver for the retrofitting of older terminals with modern marine transfer solutions that minimize environmental impact during cargo handling.

- A significant trend toward port modernization involves the integration of terminal automation and digital twin technologies for optimizing jetty operations. This development fuels the demand for smart articulated arms equipped with sensors for remote diagnostics and automated positioning, enhancing both operational efficiency and safety.

- The strategic development of new energy export hubs focused on energy transition fuels, such as green ammonia and liquid hydrogen, is creating future demand for a new generation of marine loading arms. These projects require advanced material science and engineering to ensure the safe transfer of highly specialized and often corrosive fluids, reshaping long-term R&D priorities for manufacturers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Marine Loading Arms Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 310 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.1% |

| Market growth 2026-2030 | USD 86187.4 thousand |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.0% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, The Netherlands, Norway, France, Italy, Spain, Saudi Arabia, UAE, South Africa, Egypt, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The marine loading arms market ecosystem is a complex network where raw material suppliers of high-grade carbon steel construction and stainless steel fabrication provide essential inputs to equipment manufacturers. These manufacturers, in turn, produce systems like the cryogenic loading arm and hydraulic power unit, which are then supplied to end-users such as oil and gas terminals and petrochemical handling facilities.

- Regulatory bodies like the Oil Companies International Marine Forum (OCIMF) establish the design and safety standards, heavily influencing product development and necessitating features like an emergency release system (ERS). This creates a market where manufacturers must balance the high cost of regulatory compliance with end-user demands for operational efficiency, where advanced systems can improve terminal throughput by over 15%.

- Supporting entities focused on logistics and installation play a vital role in port modernization projects, ensuring these complex systems are integrated correctly into existing port infrastructure.

What are the Key Data Covered in this Marine Loading Arms Market Research and Growth Report?

-

What is the expected growth of the Marine Loading Arms Market between 2026 and 2030?

-

The Marine Loading Arms Market is expected to grow by USD 86.19 million during 2026-2030, registering a CAGR of 4.1%. Year-over-year growth in 2026 is estimated at 4.0%%. This acceleration is shaped by new oil and gas exploration policies, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Crude oil, LG, and IG), Type (Manual marine loading arms, and Hydraulic marine loading arms), Method (Top loading, and Bottom Loading), Material (Carbon steel, Stainless steel, Aluminum, and Others) and Geography (APAC, North America, Europe, Middle East and Africa, South America). Among these, the Crude oil segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, North America, Europe, Middle East and Africa and South America. APAC is estimated to contribute 36.9% to market growth during the forecast period. Country-level analysis includes China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, The Netherlands, Norway, France, Italy, Spain, Saudi Arabia, UAE, South Africa, Egypt, Turkey, Brazil, Argentina and Chile, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is new oil and gas exploration policies, which is accelerating investment and industry demand. The main challenge is high cost associated with marine loading arms, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Marine Loading Arms Market?

-

Key vendors include Baretti, Carbis Loadtec Group, Flotech Performance Systems, Ingersoll Rand Inc., J de Jonge Group, Jiangsu Changlong Co. Ltd., JRE Pvt. Ltd., KANON Loading Equipment BV, Lianyungang HUADE Co. Ltd., Lloyds Steel Industries Ltd., OGCF Engineering M Sdn Bhd., OPW Engineered Systems, Safe Harbor Access Systems, SVT APAC Pte. Ltd., TB Global Technologies Ltd., TechnipFMC plc, WLT liquid and gas BV and Woodfield Systems. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for marine loading arms is moderately fragmented, with the top five vendors comprising less than 40% of the market share. Key players like TechnipFMC plc and Ingersoll Rand Inc. are focusing on technological differentiation, particularly in cryogenic loading arm systems for the expanding LNG market.

- Recent innovations center on terminal automation and the integration of remote diagnostics, which can reduce unplanned downtime by up to 15%. This shift addresses the end-user demand for higher operational efficiency and enhanced safety in hazardous fluid transfer.

- A persistent challenge remains the high capital expenditure required for these advanced systems, compelling vendors to offer comprehensive lifecycle cost analyses and preventive maintenance packages to justify the initial investment and ensure long-term asset integrity.

We can help! Our analysts can customize this marine loading arms market research report to meet your requirements.

RIA -

RIA -