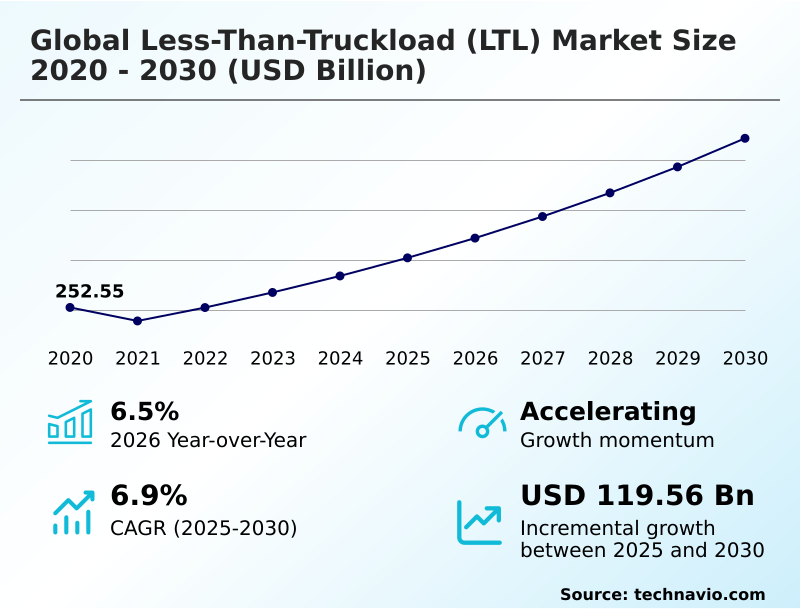

Less-than-truckload (LTL) Market Size 2026-2030

The less-than-truckload (ltl) market size is valued to increase by USD 119.56 billion, at a CAGR of 6.9% from 2025 to 2030. Proliferation of e-commerce and omnichannel distribution networks will drive the less-than-truckload (ltl) market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 57.9% growth during the forecast period.

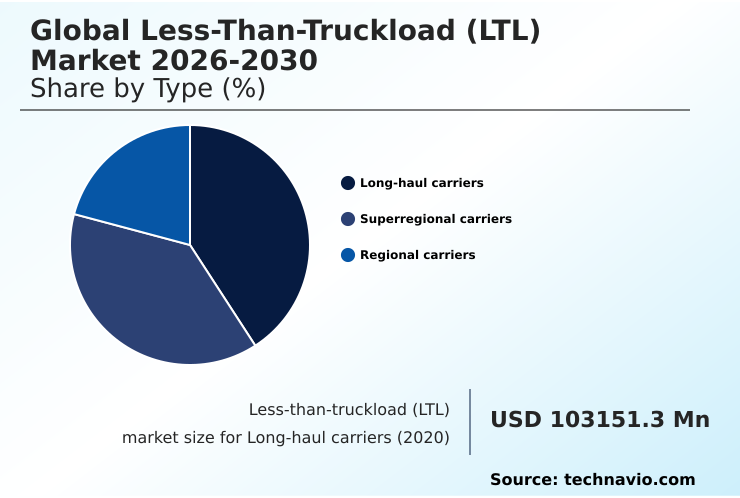

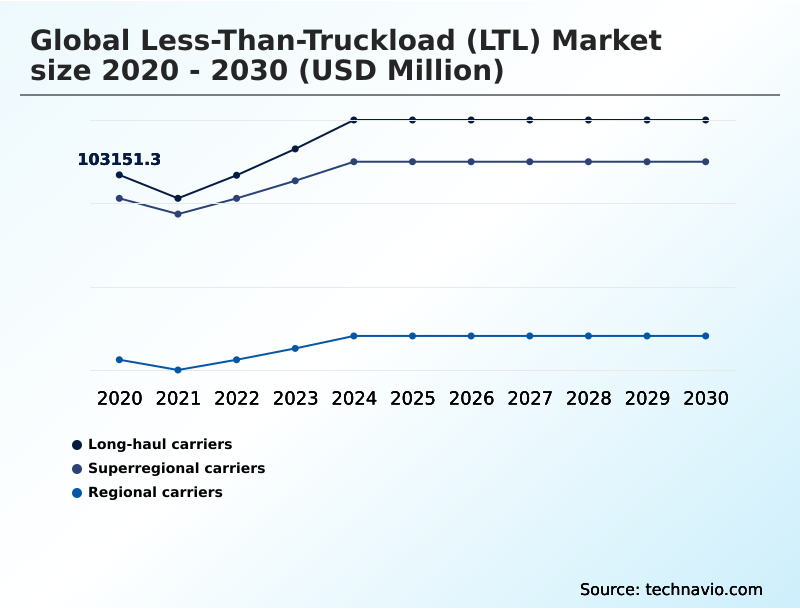

- By Type - Long-haul carriers segment was valued at USD 118.15 billion in 2024

- By Capacity - Light LTL volume segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 169.16 billion

- Market Future Opportunities: USD 119.56 billion

- CAGR from 2025 to 2030 : 6.9%

Market Summary

- The less-than-truckload (LTL) market operates on a sophisticated hub and spoke network model, designed for consolidating shipments that do not require a full trailer. This structure is essential for businesses seeking cost-effective freight transportation.

- Key market drivers include the rapid expansion of e-commerce, which fuels demand for smaller, more frequent deliveries, and the strategic shift toward nearshoring, which increases regional and cross-border LTL volumes. The adoption of AI for route optimization and density-based pricing is a major trend reshaping operational efficiency and logistics services.

- For instance, a retail company can leverage the LTL network for just-in-time inventory replenishment across its stores, optimizing supply chain visibility without incurring the expense of underutilized full truckloads. However, the industry grapples with challenges such as severe labor shortages, volatile fuel costs, and escalating cybersecurity threats that can disrupt the entire supply chain.

- The global less-than-truckload (LTL) market 2026-2030 continues to evolve through technological integration and strategic network expansions to meet these complex demands.

What will be the Size of the Less-than-truckload (LTL) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Less-than-truckload (LTL) Market Segmented?

The less-than-truckload (ltl) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Long-haul carriers

- Superregional carriers

- Regional carriers

- Capacity

- Light LTL volume

- Heavy LTL volume

- Mode of transportation

- Domestic

- International

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Type Insights

The long-haul carriers segment is estimated to witness significant growth during the forecast period.

Long-haul carriers in the global less-than-truckload (LTL) market 2026-2030 are central to transcontinental supply chains, specializing in freight transportation over extensive distances.

These operators leverage a robust hub and spoke network of break-bulk hubs to consolidate palletized freight and maximize trailer cube utilization during linehaul movements.

A structural shift is underway, with a greater focus on multimodal coordination, particularly intermodal rail, to offset volatile operational costs. This asset-based logistics segment is defined by its ability to offer day-definite service across vast geographies.

To enhance service reliability, major operators are insourcing a larger share of their linehaul miles, reporting a significant reduction in reliance on third-party capacity to maintain control over transit times and uphold freight classification standards for contract logistics.

The Long-haul carriers segment was valued at USD 118.15 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 57.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Less-than-truckload (LTL) Market Demand is Rising in APAC Get Free Sample

The geographic landscape is being reshaped by the rise of regional trade blocs and the strategic pivot to nearshoring, increasing demand for sophisticated supply chain management.

In North America, network density and service excellence define the market, with investments focused on expanding cross-docking facility infrastructure to handle both light LTL volume and heavy LTL volume.

Conversely, the APAC region is the fastest-growing market, driven by digitalization and infrastructure investment. In this region, machine learning algorithms are improving fleet utilization by 15-20%.

The rapid adoption of technology in APAC, where electric heavy-duty trucks reached a 29% market share in China, is enabling carriers to build highly efficient hub and spoke networks that integrate intermodal rail and optimize warehousing and distribution for final mile delivery.

Market Dynamics

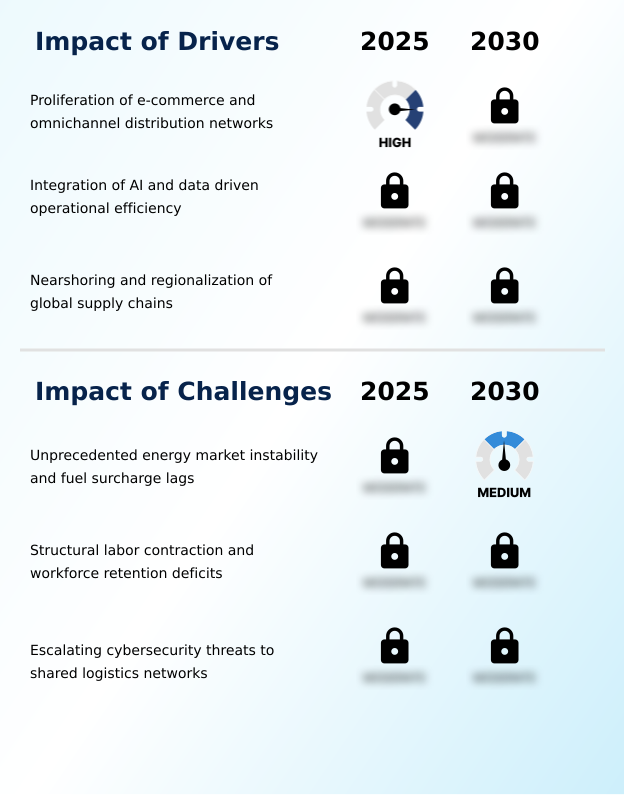

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the less-than-truckload (LTL) sector is increasingly complex, requiring a thorough less-than-truckload vs full truckload cost analysis for each shipment. Businesses are focused on improving LTL freight transit times to meet consumer expectations, a challenge amplified by the persistent impact of the driver shortage on LTL services.

- The AI impact on less-than-truckload routing is a critical factor, with advanced algorithms optimizing networks and mitigating delays. Adopting AI-driven platforms has been shown to reduce empty miles by over 10% compared to traditional methods, directly improving asset utilization. This is particularly relevant for autonomous trucking in LTL middle mile, which promises further efficiencies.

- The shift toward density-based pricing impact on LTL shippers necessitates new packaging strategies to control costs, while the role of terminal density in LTL networks becomes paramount for managing capacity. Carriers are also enhancing cross-border LTL services for nearshoring to support resilient supply chains. Simultaneously, managing fuel surcharges in LTL shipping remains a constant operational hurdle.

- Shippers now use sophisticated LTL carrier selection criteria for shippers that prioritize technology and service. These challenges in LTL final mile delivery and LTL capacity constraints and market impact are driving investments in real-time tracking technologies for LTL freight and automating LTL terminal and sorting operations.

- Navigating LTL freight classification changes and embracing multimodal LTL solutions for cost savings are key to success. Finally, cybersecurity risks in LTL transportation management, LTL services for e-commerce fulfillment, optimizing trailer cube utilization in LTL and adopting sustainable practices in LTL logistics are becoming core competencies.

What are the key market drivers leading to the rise in the adoption of Less-than-truckload (LTL) Industry?

- The proliferation of e-commerce and the expansion of omnichannel distribution networks are key drivers of market growth.

- The expansion of e-commerce and omnichannel distribution is a primary market driver, compelling a shift toward smaller, more frequent less-than-truckload freight shipments to support just-in-time inventory strategies.

- This surge in demand from e-commerce fulfillment has led to a 3% rise in daily shipment counts for some providers, even during periods of manufacturing slowdown.

- To manage this complexity, carriers are adopting AI-powered route optimization and other advanced logistics services to improve trailer cube utilization and overall fleet utilization.

- The adoption of machine learning algorithms in some regions has been shown to improve efficiency by 15-20%.

- The widespread demand for complete supply chain visibility and real-time freight visibility is now a standard expectation for all stakeholders in the global less-than-truckload (LTL) market 2026-2030.

What are the market trends shaping the Less-than-truckload (LTL) Industry?

- A key market trend is the accelerated commercialization of Level 4 autonomous technology. This is primarily focused on middle-mile logistics to enhance operational efficiency.

- A transformative trend is the commercialization of autonomous trucking for middle-mile logistics, a development that promises to reduce delivery times by up to 40% and address chronic labor shortages. This shift is complemented by a move toward density-based pricing, enabled by the aggressive deployment of dimensional scanners and automated sorting technology in terminal operations.

- Regional carriers are expanding physical terminal density to enhance network efficiency for freight consolidation and groupage services. This investment in both physical and digital infrastructure allows for improved handling of time-critical LTL shipments and is setting a new performance benchmark that even freight forwarders must adapt to.

- Through better network design and handling protocols, leading operators have also driven damage claim ratios below 0.2%, improving service reliability.

What challenges does the Less-than-truckload (LTL) Industry face during its growth?

- Unprecedented energy market instability, compounded by fuel surcharge lags, presents a key challenge to industry growth.

- The sector faces significant headwinds from extreme energy price volatility, with diesel costs surging 50% in some instances, creating severe challenges in managing fuel surcharges. This is compounded by a structural driver shortage and persistent LTL capacity constraints, forcing some firms to increase compensation by 20% to retain staff for services like last mile delivery and cross-border LTL.

- Furthermore, escalating cybersecurity risks threaten shared logistics platforms used for shipment tracking, freight brokerage, and even customs brokerage. A successful attack can paralyze inventory management systems, with the frequency of such incidents having surged by 61% in the logistics sector, and the average cost of a data breach exceeding $4 million.

Exclusive Technavio Analysis on Customer Landscape

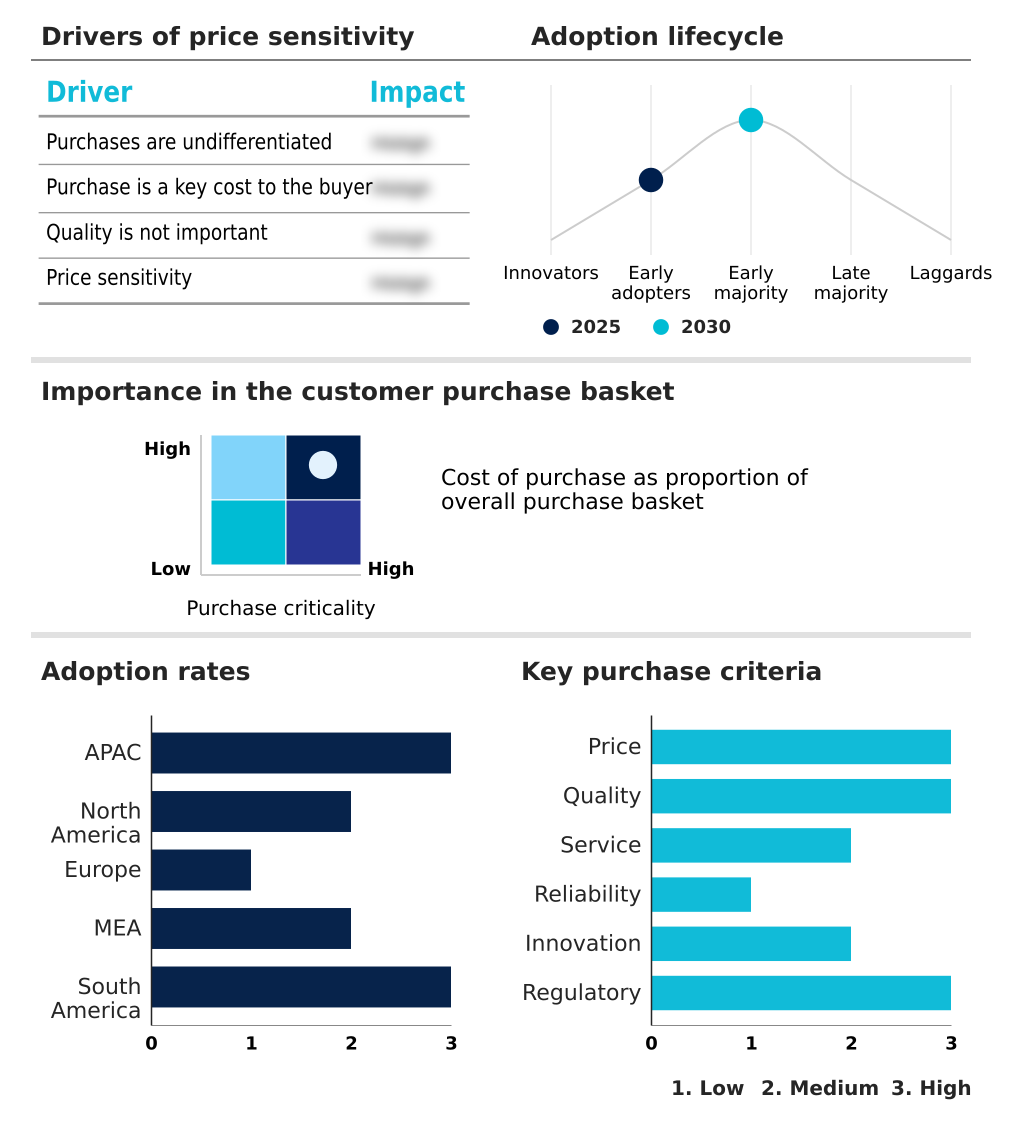

The less-than-truckload (ltl) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the less-than-truckload (ltl) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Less-than-truckload (LTL) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, less-than-truckload (ltl) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ArcBest Corp. - Specializes in providing time-critical and managed logistics less-than-truckload (LTL) solutions, focusing on asset-based freight services for complex supply chain needs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ArcBest Corp.

- C H Robinson Worldwide Inc.

- CEVA Logistics SA

- CJ Logistics Corp.

- Dachser SE

- DB Schenker

- DHL International GmbH

- DSV AS

- FedEx Corp.

- Forward Air Corporation

- GEODIS

- Kuehne Nagel Management AG

- Landstar System Inc.

- Mainfreight Ltd.

- Nippon Express Holdings Inc.

- Old Dominion Freight Line

- Rhenus SE and Co. KG

- Schneider National Inc.

- TFI International Inc.

- XPO Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Less-than-truckload (ltl) market

- In March, 2025, FedEx Corp. detailed its independence strategy for its FedEx Freight division, targeting a 12% operating margin by focusing on high-value industrial and cross-border shipments.

- In April, 2025, Saia Inc. expanded its network by opening a new 74-door terminal in York, Pennsylvania, to enhance one-day service capabilities in the Mid-Atlantic and Northeast corridors.

- In May, 2025, Amazon expanded its logistics services, opening its automated freight, distribution, and parcel shipping network to external businesses, increasing competition in the supply chain sector.

- In January, 2025, The National Motor Freight Traffic Association initiated a major classification overhaul, transitioning the industry toward a streamlined, density-based system to reduce disputes and modernize freight preparation.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Less-than-truckload (LTL) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.9% |

| Market growth 2026-2030 | USD 119555.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.5% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, Poland, The Netherlands, Saudi Arabia, UAE, South Africa, Turkey, Qatar, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The less-than-truckload (LTL) market is undergoing a significant transformation driven by technological integration and shifting supply chain dynamics. The foundational hub and spoke network is being enhanced with advanced route optimization and automated sorting technology to manage the complexities of modern logistics services. This evolution is critical for handling the surge in less-than-truckload freight from e-commerce and regionalized manufacturing.

- A key trend is the industry's move toward density-based pricing, supported by automated dimensional scanners that provide precise freight data. This shift forces a boardroom-level re-evaluation of packaging engineering and its impact on overall logistics costs, directly influencing product profitability and supply chain strategy. The implementation of AI-driven terminal operations has demonstrated the ability to improve throughput by over 30%.

- As the market evolves, capabilities such as real-time shipment tracking, efficient customs brokerage for cross-border LTL, and sophisticated inventory management are becoming standard. This digital transformation is essential for optimizing trailer cube utilization and enhancing overall supply chain visibility.

What are the Key Data Covered in this Less-than-truckload (LTL) Market Research and Growth Report?

-

What is the expected growth of the Less-than-truckload (LTL) Market between 2026 and 2030?

-

USD 119.56 billion, at a CAGR of 6.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Long-haul carriers, Superregional carriers, and Regional carriers), Capacity (Light LTL volume, and Heavy LTL volume), Mode of Transportation (Domestic, and International) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of e-commerce and omnichannel distribution networks, Unprecedented energy market instability and fuel surcharge lags

-

-

Who are the major players in the Less-than-truckload (LTL) Market?

-

ArcBest Corp., C H Robinson Worldwide Inc., CEVA Logistics SA, CJ Logistics Corp., Dachser SE, DB Schenker, DHL International GmbH, DSV AS, FedEx Corp., Forward Air Corporation, GEODIS, Kuehne Nagel Management AG, Landstar System Inc., Mainfreight Ltd., Nippon Express Holdings Inc., Old Dominion Freight Line, Rhenus SE and Co. KG, Schneider National Inc., TFI International Inc. and XPO Inc.

-

Market Research Insights

- The less-than-truckload (LTL) market is characterized by disciplined pricing and a strategic pivot toward enhanced regional service offerings. Asset-based logistics providers are expanding their terminal density to support day-definite service commitments, a crucial factor as shippers prioritize reliability. The transition to density-based freight classification is compelling shippers to optimize packaging, impacting both light LTL volume and heavy LTL volume.

- To manage rising costs from the persistent driver shortage, some carriers have increased compensation by up to 20%. Concurrently, leading operators have improved service quality, with damage claim ratios falling below 0.2%. This focus on efficiency and service is vital for managing time-critical LTL and expedited LTL shipments in a competitive environment where e-commerce fulfillment and just-in-time inventory models dominate.

We can help! Our analysts can customize this less-than-truckload (ltl) market research report to meet your requirements.

RIA -

RIA -