Education Erp For Private Institutions Market Size and Growth Forecast 2026-2030

The Education Erp For Private Institutions Market size was valued at USD 9.04 billion in 2025 growing at a CAGR of 15.9% during the forecast period 2026-2030.

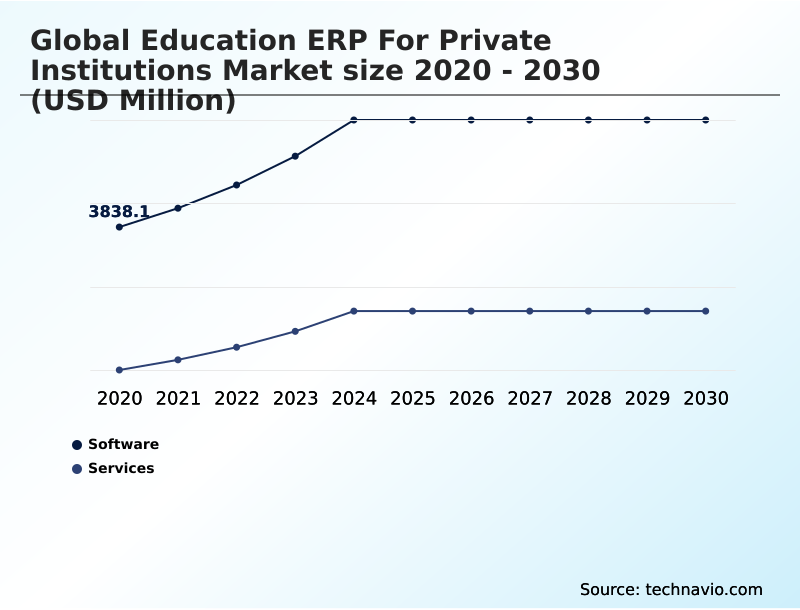

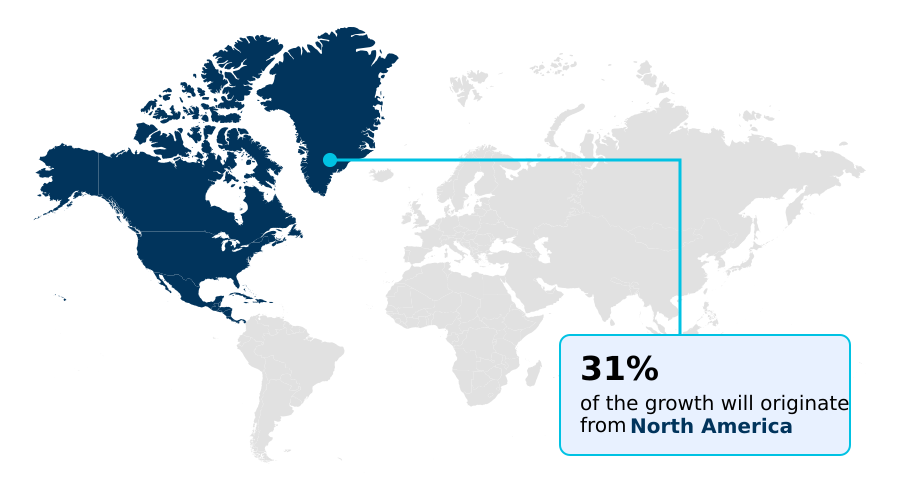

North America accounts for 31.1% of incremental growth during the forecast period. The Software segment by Component was valued at USD 5.37 billion in 2024, while the Higher education segment holds the largest revenue share by End-user.

The market is projected to grow by USD 13.29 billion from 2020 to 2030, with USD 9.88 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Education Erp For Private Institutions Market Overview

The Education ERP for Private Institutions market is undergoing a significant digital transformation, with a notable 13.7% year-over-year growth driven by the need for operational agility. Institutions are moving beyond basic record-keeping to adopt systems that provide a single source of truth for strategic decision-making. This involves integrating the student information system with modules for financial aid automation and admissions management software. A key focus is on leveraging institutional analytics to improve outcomes and ensure financial sustainability. For instance, a mid-sized private university implementing a new cloud-based ERP deployment for its campus management system can utilize student retention analytics to identify at-risk students, leading to proactive interventions that typically improve retention rates by 5-10%. This data-driven approach, which also includes a robust compliance reporting engine to meet standards like FERPA, is becoming essential for competing in a market where North America accounts for over 31% of the incremental growth.

Drivers, Trends, and Challenges in the Education Erp For Private Institutions Market

Strategic decision-making in the education ERP market for private institutions involves a complex cost-benefit analysis of education erp systems. Institutions frequently start by comparing on-premise vs cloud erp for schools, with the latter often favored for lower upfront costs and scalability.

The process of selecting an erp vendor for a private school requires careful evaluation of the top features of modern education erp, especially for distinct segments like erp systems for k-12 private schools versus the more complex cloud erp for higher education institutions.

A primary goal is improving student retention with erp analytics, which hinges on successfully integrating lms with student information systems. This integration is not just operational but also a matter of compliance, particularly for meeting the stringent data privacy rules of FERPA, which governs ferpa compliance in student data systems.

For instance, a private university that automated its admissions and financial aid processes saw a 20% reduction in processing time compared to its legacy system, highlighting how using ai in education administration software yields tangible benefits.

Despite common erp implementation challenges in private colleges, a modular approach focusing on high-impact areas like erp for international student management and automating financial aid with erp software can deliver a faster return on investment, demonstrating that student lifecycle management software benefits are maximized through strategic, phased adoption.

Primary Growth Driver: The acceleration of cloud-based deployment and the widespread adoption of Software-as-a-Service (SaaS) models are key drivers for the market.

The market's 13.7% year-over-year growth is largely propelled by the imperative for data-driven decision making in a competitive educational landscape. Private institutions are investing heavily in modern campus management system solutions to derive actionable insights from institutional analytics.

The rapid acceleration of cloud-based ERP deployment is a primary engine, offering the scalability required to support advanced functions like AI-powered enrollment forecasting and predictive modeling for retention. This is particularly evident in high-growth regions like APAC.

Furthermore, the integration of AI for administrative workflow automation, including automated course scheduling and tuition billing systems, is reducing operational costs and freeing up staff for strategic initiatives, thereby fueling further demand for advanced ERP capabilities.

Emerging Market Trend: A key market trend is the rising emphasis on holistic student lifecycle management and engagement, moving beyond traditional administrative functions.

The market is evolving from administrative record-keeping to platforms centered on holistic student engagement. This trend prioritizes a unified digital ecosystem where learning management system integration with the core student information system is seamless and robust.

Institutions are increasingly adopting a composable enterprise strategy, utilizing interoperability APIs to connect specialized applications for functions like the donor management module and alumni relations management. This approach is critical as the higher education segment, which constitutes the majority of the market, intensifies its focus on student retention analytics to secure financial stability.

This strategic pivot toward full student lifecycle management is a direct response to rising expectations for a connected, consumer-grade digital campus experience.

Key Industry Challenge: Substantial initial implementation costs and persistent budgetary constraints represent a key challenge affecting industry growth and technology adoption.

A primary hurdle for market adoption remains the challenge of ensuring data security in higher ed while adhering to complex regulatory compliance frameworks such as GDPR and FERPA. This necessitates sophisticated data governance protocols and a reliable compliance reporting engine, which significantly increases the system's total cost of ownership (TCO).

Furthermore, migrating from entrenched legacy systems requires substantial business process reengineering and overcoming cultural resistance to change, which can delay the realization of a single source of truth. The technical and financial resources needed to successfully integrate disparate applications into a modern student information system continue to be a significant barrier for many budget-conscious private institutions.

Explore Full Market Dynamics Analysis Request Free Sample

Education Erp For Private Institutions Market Segmentation

The education erp for private institutions industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Component Segment Analysis

The software segment is estimated to witness significant growth during the forecast period.

The software segment is the primary component of the education ERP market for private institutions, commanding approximately 67% of the total market share. This dominance reflects a strategic shift away from fragmented, legacy systems toward a unified digital ecosystem.

Procurement decisions are increasingly focused on integrated platforms that combine the student information system, admissions management software, and learning management system integration into a single interface.

The adoption of cloud-based ERP deployment is a critical factor, enabling institutions to leverage advanced institutional analytics and a centralized campus management system without significant upfront capital expenditure.

This trend is driven by the need for a comprehensive student lifecycle management solution that enhances operational efficiency and supports data-driven decision-making across all administrative functions.

The Software segment was valued at USD 5.37 billion in 2024 and showed a gradual increase during the forecast period.

Education Erp For Private Institutions Market by Region: North America Leads with 31.1% Growth Share

North America is estimated to contribute 31.1% to the growth of the global market during the forecast period.

The global geographic landscape is diverse, with North America representing a mature market focused on modernization, contributing nearly one-third of the incremental growth.

In contrast, the APAC region is the fastest-growing market, with a CAGR of 17.7%, driven by first-time adoption of comprehensive campus management system solutions in countries like India.

European institutions prioritize ERP systems with a robust compliance reporting engine to adhere to GDPR mandates, influencing vendor selection criteria.

Across all regions, the core requirements for student lifecycle management and learning management system integration remain consistent, but implementation strategies are tailored to local regulatory and competitive pressures.

This regional differentiation shapes the global demand for adaptable and scalable education ERP platforms.

Customer Landscape Analysis for the Education Erp For Private Institutions Market

The education erp for private institutions market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the education erp for private institutions market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Education Erp For Private Institutions Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the education erp for private institutions market industry.

Academia - Offerings include unified platforms that manage the complete student lifecycle through integrated admissions, finance, and academic modules, enhancing institutional analytics and operational efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Academia

- Anthology Inc.

- Blackbaud Inc.

- Classe365

- Creatrix Campus

- Ellucian Co.

- Foradian Technologies Pvt Ltd.

- iSAMS Pty Ltd

- Jenzabar Inc.

- Kuali Inc

- MasterSoft

- Oracle Corp.

- Populi

- PowerSchool Holdings Inc.

- SAP SE

- Skyward Inc.

- Tribal Group Plc

- Unit4 Group Holding BV

- Veracross

- Workday Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Education Erp For Private Institutions Market

- In September 2024, Anthology Inc. announced a strategic partnership with a leading cloud services provider to enhance the AI capabilities and cybersecurity framework of its Anthology Student platform, aiming to deliver improved predictive analytics for private higher education institutions.

- In January 2025, the Government of Uttar Pradesh in India accelerated the implementation of the Samarth ERP platform across its state universities and colleges to standardize academic, financial, and administrative processes under a unified digital framework.

- In March 2025, Jadavpur University announced it had secured funding approval for a comprehensive ERP system designed to manage academic processes, examinations, payroll, and other critical administrative workflows, aiming to modernize its operational infrastructure.

- In April 2025, Ellucian Co. launched a new SaaS module for its Banner ERP platform, focusing on advanced donor management and alumni engagement analytics, which is specifically tailored for the fundraising and advancement offices of private universities.

Research Analyst Overview: Education Erp For Private Institutions Market

Boardroom decisions in private education are increasingly centered on leveraging institutional analytics for financial sustainability, a shift from viewing ERPs as mere administrative tools. With the software segment comprising over two-thirds of market investment, the focus is on acquiring a modern campus management system that unifies admissions management software, financial aid automation, and tuition billing systems.

A key driver is the mandate for accessibility compliance (WCAG), which is forcing a re-engineering of the mobile-first student portal and overall user experience. A unified digital ecosystem is now a baseline requirement for competitive positioning, with institutions using AI-powered enrollment forecasting to navigate demographic shifts.

The entire student lifecycle management process, from initial inquiry to alumni relations management, is being optimized through data-driven decision making. This strategic reorientation underscores the critical role of advanced ERP platforms in shaping institutional viability and growth in a competitive landscape.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Education Erp For Private Institutions Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 280 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 15.9% |

| Market growth 2026-2030 | USD 9881.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 13.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, Australia, South Korea, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Education Erp For Private Institutions Market: Key Questions Answered in This Report

-

What is the expected growth of the Education Erp For Private Institutions Market between 2026 and 2030?

-

The Education Erp For Private Institutions Market is expected to grow by USD 9.88 billion during 2026-2030, registering a CAGR of 15.9%. Year-over-year growth in 2026 is estimated at 13.7%%. This acceleration is shaped by acceleration of cloud-based deployment and saas models, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, and Services), End-user (Higher education, and K-12), Deployment (Cloud, and On-premises) and Geography (North America, Europe, APAC, Middle East and Africa, South America). Among these, the Software segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, Middle East and Africa and South America. North America is estimated to contribute 31.1% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, Australia, South Korea, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is acceleration of cloud-based deployment and saas models, which is accelerating investment and industry demand. The main challenge is initial implementation costs and budgetary constraints, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Education Erp For Private Institutions Market?

-

Key vendors include Academia, Anthology Inc., Blackbaud Inc., Classe365, Creatrix Campus, Ellucian Co., Foradian Technologies Pvt Ltd., iSAMS Pty Ltd, Jenzabar Inc., Kuali Inc, MasterSoft, Oracle Corp., Populi, PowerSchool Holdings Inc., SAP SE, Skyward Inc., Tribal Group Plc, Unit4 Group Holding BV, Veracross and Workday Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Education Erp For Private Institutions Market Research Insights

Market dynamics are increasingly shaped by stringent regulatory compliance frameworks, compelling institutions to prioritize robust data governance protocols. The adoption of a composable enterprise strategy is gaining favor over monolithic systems, offering greater operational agility in education by allowing institutions to integrate best-in-class applications.

This shift necessitates significant business process reengineering to achieve a single source of truth across all administrative and academic functions. For example, ensuring compliance with the Family Educational Rights and Privacy Act (FERPA) requires meticulous configuration of access controls within the student information system.

As a result, the focus is on creating a secure, interoperable ecosystem that supports holistic student engagement while meeting complex legal and institutional demands for data integrity and protection.

We can help! Our analysts can customize this education erp for private institutions market research report to meet your requirements.

RIA -

RIA -