Digital Pathology Workflow Software Market Size and Growth Forecast 2026-2030

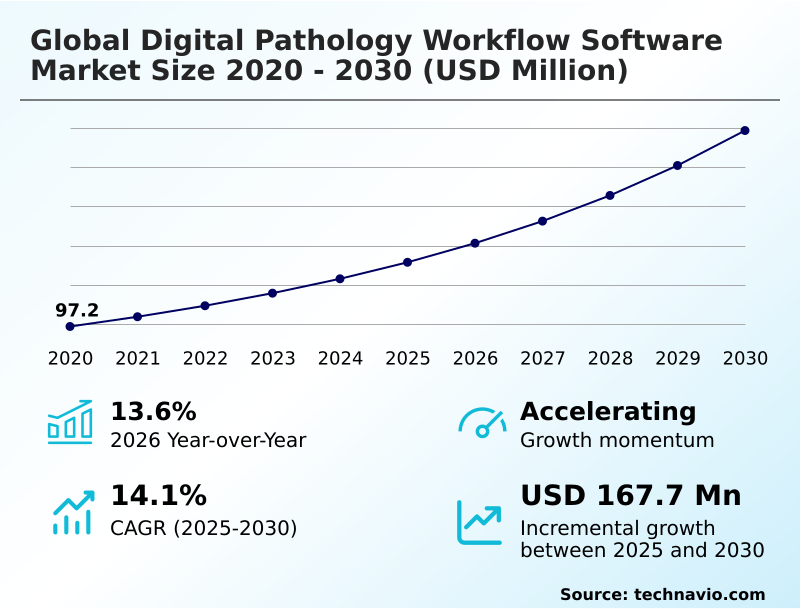

The Digital Pathology Workflow Software Market size was valued at USD 178.9 million in 2025 growing at a CAGR of 14.1% during the forecast period 2026-2030.

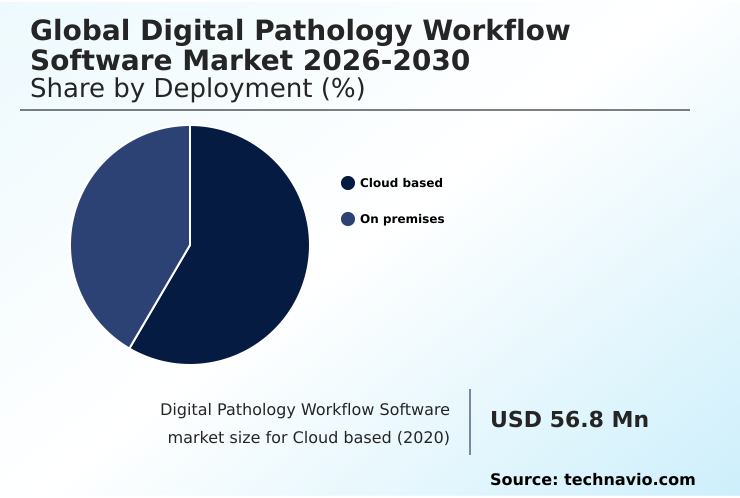

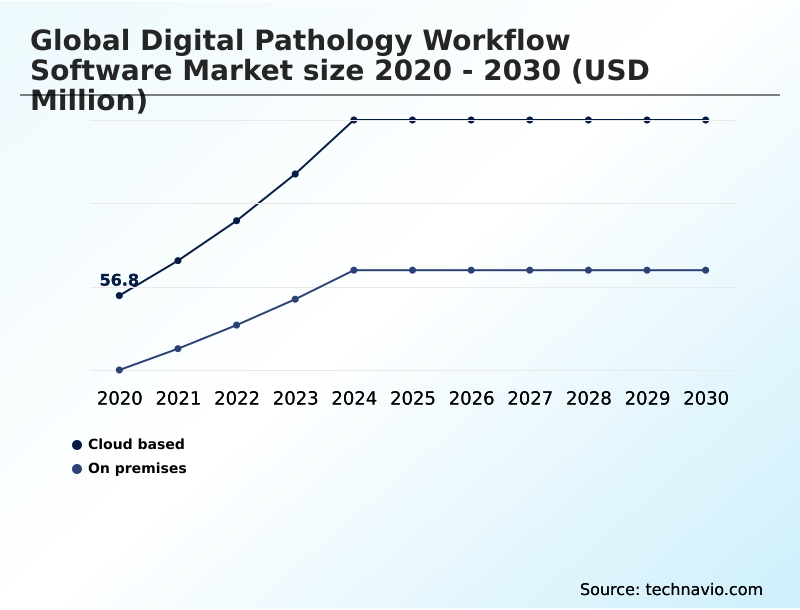

North America accounts for 40.2% of incremental growth during the forecast period. The Cloud based segment by Deployment was valued at USD 95.5 million in 2024, while the Disease diagnosis segment holds the largest revenue share by Application.

The market is projected to grow by USD 249.4 million from 2020 to 2030, with USD 167.7 million of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Digital Pathology Workflow Software Market Overview

The digital pathology workflow software market is defined by a systemic shift from manual microscopy to integrated digital environments. This transition is driven by the need for greater efficiency and diagnostic precision, compelling laboratories to adopt computational pathology and AI-powered diagnostics. The architecture for these systems must support whole-slide imaging and ensure seamless LIS/LIMS integration for a unified anatomic pathology workflow. North America is set to capture over 40% of the market's incremental growth, leading in digital pathology adoption rates. For instance, a multi-site academic medical center implementing a unified platform for multi-site workflow orchestration and a vendor-neutral archive can achieve standardized diagnostic protocols, leveraging telepathology for expert consultations across state lines. This ensures data consistency through DICOM for pathology standards. However, the high initial investment in digital slide scanners and image management systems, alongside the complexities of pathology information system integration, requires a clear return-on-investment analysis before adoption.

Drivers, Trends, and Challenges in the Digital Pathology Workflow Software Market

The digital pathology workflow software market is expanding, with a notable year-over-year growth of 13.6%, as healthcare providers weigh the cost of implementing digital pathology workflow against long-term operational gains.

Boardroom decisions increasingly center on the ROI calculation for digital pathology systems, where upfront capital for high-throughput slide scanning equipment is balanced against efficiency improvements from AI for prostate cancer grading in pathology and other automated analyses.

A critical factor is the choice of infrastructure, with cloud storage solutions for whole slide images offering scalability but demanding rigorous security requirements for cloud pathology platforms to comply with data privacy regulations like GDPR.

For instance, a US-based laboratory network must ensure its strategy for integrating digital pathology with LIS is fully compliant with CLIA '88 regulations, which govern laboratory testing.

The move toward open ecosystems is also crucial, with growing demand for open source tools for pathology image analysis and vendor-neutral archive for digital pathology benefits, enabling best-of-breed technology adoption in digital pathology workflow for multi-site labs.

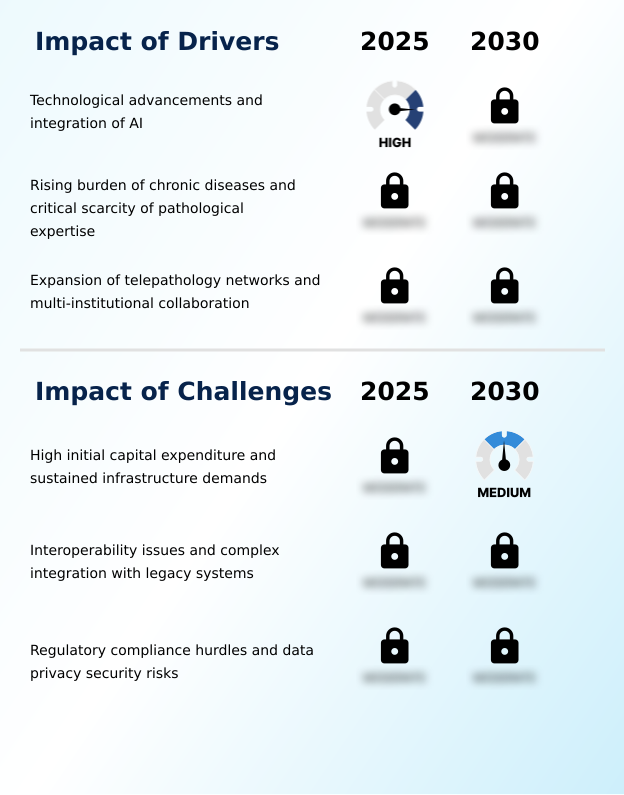

Primary Growth Driver: Technological advancements, particularly the integration of artificial intelligence, are the primary drivers of market growth.

The market's expansion is fundamentally driven by the critical scarcity of pathological expertise coupled with a rising caseload of complex diseases. This imbalance creates significant demand for solutions that improve pathology workflow efficiency and enable pathology lab automation.

North America, which is poised to contribute 40.2% of the market's incremental growth, exemplifies this trend as large healthcare networks invest heavily in digital infrastructure to optimize resource allocation.

The integration of AI-assisted cancer diagnosis into routine workflows allows these institutions to manage high volumes and provide expert-level analysis more consistently.

This technological intervention directly addresses the operational pressures on diagnostic laboratories, making software a critical tool for maintaining quality and speed in patient care.

Emerging Market Trend: The market is experiencing a significant migration toward cloud-native architectures, accompanied by the growing adoption of software-as-a-service delivery models.

A defining market trend is the move toward integrative diagnostics, where digital pathology converges with other data streams like genomics and radiology. This evolution is transforming disease diagnosis, which accounts for over half of all applications, by creating a more holistic view of patient pathology.

Software is evolving into an integrative diagnostics platform capable of correlating histopathology image analysis with molecular data, which is crucial for personalized medicine. This shift is supported by AI in histopathology, which automates complex biomarker quantification.

As laboratories generate massive datasets from whole-slide imaging, the development of open-source tools for pathology image analysis is accelerating innovation and enabling researchers to build and validate novel algorithms, further enhancing the capabilities of these sophisticated systems.

Key Industry Challenge: High initial capital expenditures and sustained infrastructure demands present a key challenge to industry growth.

A primary market challenge is the high cost of implementing digital pathology workflow, which includes not only software licenses but also capital-intensive hardware such as high-throughput slide scanning systems. This financial barrier is compounded by the technical complexities of LIS/LIMS integration and the need to ensure software is scanner-agnostic to avoid vendor lock-in.

For many institutions, justifying the investment requires a detailed digital pathology ROI analysis, which can be difficult to model accurately. Furthermore, the persistent threat to cybersecurity for pathology data necessitates significant and ongoing expenditure on security infrastructure to comply with stringent regulations like GDPR, adding another layer of cost and complexity to full-scale digital adoption.

Explore Full Market Dynamics Analysis Request Free Sample

Digital Pathology Workflow Software Market Segmentation

The digital pathology workflow software industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Deployment Segment Analysis

The cloud based segment is estimated to witness significant growth during the forecast period.

The market's segmentation reflects a decisive shift toward cloud-based deployment, which is projected to constitute over 61% of the market by 2025.

This model offers procurement decision-makers enhanced scalability for pathology data storage solutions and facilitates the adoption of SaaS pathology solutions, aligning with operational expenditure budget models.

Cloud-native pathology platforms are critical for enabling multi-site workflow orchestration and supporting telepathology network setups.

These architectures provide the necessary framework for centralized image management systems and robust cybersecurity for pathology data, which are essential for compliance with regulations like HIPAA.

This approach simplifies the deployment of AI-powered diagnostics while addressing the total cost of ownership implications associated with on-premises pathology servers, making it a strategic choice for institutions pursuing a modern enterprise imaging strategy.

The Cloud based segment was valued at USD 95.5 million in 2024 and showed a gradual increase during the forecast period.

Digital Pathology Workflow Software Market by Region: North America Leads with 40.2% Growth Share

North America is estimated to contribute 40.2% to the growth of the global market during the forecast period.

The geographic landscape of the digital pathology workflow software market is characterized by mature adoption in North America, which accounts for 40.2% of the incremental growth, and accelerated expansion in APAC, which exhibits the highest regional CAGR of 15.1%.

In North America, growth is sustained by large-scale health systems implementing advanced enterprise imaging strategies and telepathology network setups to address pathologist shortages.

Meanwhile, APAC's rapid growth is fueled by government-led healthcare modernization and the adoption of digital pathology for clinical trials.

The successful deployment of these technologies globally hinges on adherence to interoperability standards like DICOM and the establishment of scanner-agnostic software ecosystems.

This ensures that data from whole slide image viewers and other systems can be shared seamlessly across international research collaborations and clinical networks.

Customer Landscape Analysis for the Digital Pathology Workflow Software Market

The digital pathology workflow software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the digital pathology workflow software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Digital Pathology Workflow Software Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the digital pathology workflow software market industry.

3DHISTECH Ltd. - AI-driven computational pathology platforms are enabling quantitative biomarker analysis and predictive diagnostics, enhancing precision oncology workflows and informing therapeutic decisions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3DHISTECH Ltd.

- Aiforia Technologies PLC

- Corista

- Dedalus Group

- F. Hoffmann La Roche Ltd.

- FUJIFILM Holdings Corp.

- Gestalt Diagnostics

- Hamamatsu Photonics KK

- Huron Digital Pathology

- Ibex Medical Analytics

- Indica Labs LLC.

- Koninklijke Philips NV

- Leica Biosystems Nussloch GmbH

- Mikroscan Technologies Inc.

- Paige AI Inc.

- PathAI Inc.

- Proscia Inc.

- Sectra AB

- Tribun Health

- Visiopharm AS

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Digital Pathology Workflow Software Market

- In May 2025, PathAI introduced an upgraded version of its AISight platform featuring enhanced deep-learning algorithms for predictive biomarker quantification, designed to assist clinicians in selecting appropriate targeted therapies.

- In April 2025, Fujifilm Healthcare Americas Corporation launched an updated version of its Synapse pathology platform, which focused specifically on cloud-native capabilities to support the growing requirements of distributed laboratory networks.

- In July 2025, Philips announced a strategic partnership with several molecular biology firms to integrate genomic profiling data directly into its digital pathology viewer, enabling a combined analysis of cellular patterns and genetic markers.

- In October 2025, Sectra introduced a new module for its digital pathology platform that utilizes an open application programming interface (API) to facilitate the rapid deployment of third-party clinical algorithms across its user base.

Research Analyst Overview: Digital Pathology Workflow Software Market

The strategic migration toward cloud-native pathology platforms is redefining laboratory infrastructure, with this deployment model accounting for over 61% of the market. This shift forces boardroom-level decisions regarding CAPEX versus OPEX, influencing the long-term enterprise imaging strategy and total cost of ownership.

The adoption of SaaS pathology solutions streamlines updates and enhances accessibility but introduces rigorous data governance challenges, particularly under regulations like Europe's IVDR, which mandates strict diagnostic algorithm validation for any regulatory-cleared AI modules used in an anatomic pathology workflow.

Consequently, a key vendor qualification criterion is the provider's ability to demonstrate a clear pathway for validating its computational pathology tools. This includes ensuring their image management system adheres to interoperability standards and can be integrated into a compliant, high-throughput slide scanning environment, which is fundamental for modern histopathology image analysis.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Digital Pathology Workflow Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 308 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 14.1% |

| Market growth 2026-2030 | USD 167.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 13.6% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Digital Pathology Workflow Software Market: Key Questions Answered in This Report

-

What is the expected growth of the Digital Pathology Workflow Software Market between 2026 and 2030?

-

The Digital Pathology Workflow Software Market is expected to grow by USD 167.7 million during 2026-2030, registering a CAGR of 14.1%. Year-over-year growth in 2026 is estimated at 13.6%%. This acceleration is shaped by technological advancements and integration of ai, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud based, and On premises), Application (Disease diagnosis, Drug discovery and development, Academic research and training, and Others), End-user (Hospitals and reference laboratories, Clinical laboratories, Pharmaceutical companies, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa). Among these, the Cloud based segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, South America and Middle East and Africa. North America is estimated to contribute 40.2% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is technological advancements and integration of ai, which is accelerating investment and industry demand. The main challenge is high initial capital expenditure and sustained infrastructure demands, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Digital Pathology Workflow Software Market?

-

Key vendors include 3DHISTECH Ltd., Aiforia Technologies PLC, Corista, Dedalus Group, F. Hoffmann La Roche Ltd., FUJIFILM Holdings Corp., Gestalt Diagnostics, Hamamatsu Photonics KK, Huron Digital Pathology, Ibex Medical Analytics, Indica Labs LLC., Koninklijke Philips NV, Leica Biosystems Nussloch GmbH, Mikroscan Technologies Inc., Paige AI Inc., PathAI Inc., Proscia Inc., Sectra AB, Tribun Health and Visiopharm AS. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Digital Pathology Workflow Software Market Research Insights

The market dynamics are heavily influenced by the strategic choice between cloud vs on-premise pathology deployments. The decision impacts not only data accessibility but also compliance with security frameworks like those mandated for pathology EMR integration. A key factor shaping procurement is the availability of FDA-approved pathology AI, which is transforming diagnostic capabilities.

For example, a clinical laboratory's decision to adopt a specific platform is increasingly tied to the software's ability to integrate regulatory-cleared AI modules for specific tasks such as prostate cancer grading.

This move toward AI-assisted cancer diagnosis requires robust pathology data storage solutions and a clear strategy for diagnostic algorithm validation to meet stringent standards like those set by the FDA for Software as a Medical Device (SaMD), ultimately impacting pathology lab automation and overall workflow efficiency.

We can help! Our analysts can customize this digital pathology workflow software market research report to meet your requirements.

RIA -

RIA -