India Contact Lens Market Size 2026-2030

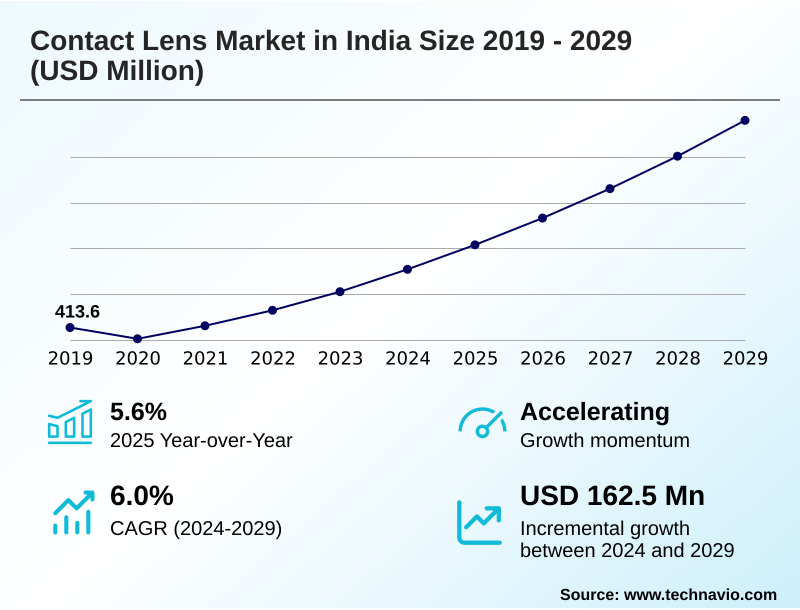

The India Contact Lens Market size was valued at USD 503.8 million in 2025, growing at a CAGR of 6.1% during the forecast period 2026-2030.

Major Market Trends & Insights

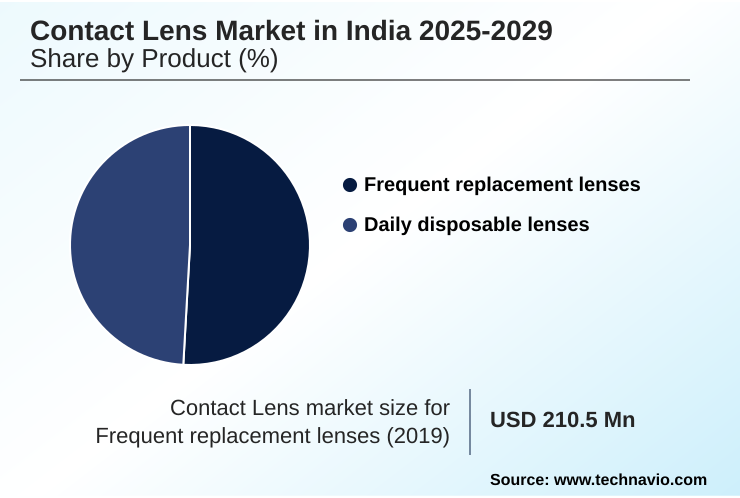

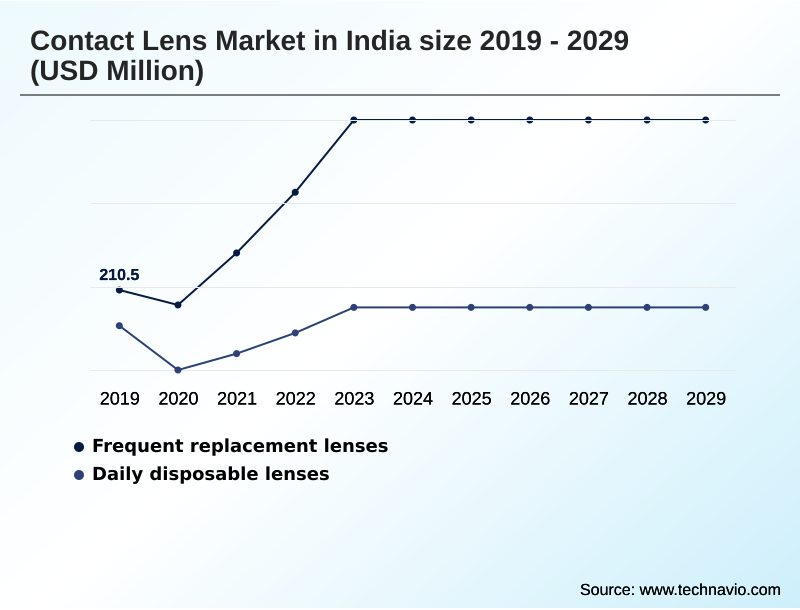

- By Product - Frequent replacement lenses segment was valued at USD 263.5 million in 2024

- By Distribution Channel - Online segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 276.2 million

- Market Future Opportunities 2025-2030: USD 173.7 million

- CAGR from 2025 to 2030 : 6.1%

Market Summary

- The contact lens market in India is defined by a structural shift from corrective eyewear as a necessity to a lifestyle choice, with adoption rates in urban centers increasing by over 20%.

- This expansion is driven by a surge in myopia and rising aesthetic consciousness, but it is concurrently constrained by high user discontinuation rates, where nearly 40% of new wearers stop within the first year due to discomfort.

- A key business scenario involves supply chain localization, where manufacturers establish domestic facilities to produce high-volume frequent replacement lenses, reducing import reliance by up to 50% and better serving price-sensitive Tier-2 and Tier-3 cities. This strategy directly addresses the challenge of affordability while capitalizing on the growing demand for vision correction.

- The market's trajectory is thus shaped by the interplay between a growing addressable population and the critical need for product innovations that improve wearer comfort and long-term compliance.

What will be the Size of the India Contact Lens Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the India Contact Lens Market Segmented?

The india contact lens industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Frequent replacement lenses

- Daily disposable lenses

- Distribution channel

- Online

- Offline

- Application

- Corrective lens

- Therapeutic lens

- Cosmetic lens

- Geography

- APAC

- India

- APAC

How is the India Contact Lens Market Segmented by Product?

The frequent replacement lenses segment is estimated to witness significant growth during the forecast period.

The frequent replacement lenses segment, while mature, remains a cornerstone of the market, accounting for over 55% of total volume due to a favorable replacement schedule for price-sensitive consumers.

This category is undergoing a significant internal shift, with a clear migration from older materials to advanced silicone hydrogel options that mitigate the risk of corneal hypoxia.

These newer lenses, which demonstrate up to five times greater oxygen transmissibility, are increasingly positioned as the standard for initial refractive error correction.

Growth is supported by expanding private label brands and practitioner education focused on balancing cost with long-term wearer comfort.

As prescription verification becomes more stringent, this segment adapts by emphasizing the clinical benefits of its evolving polymer chemistry and superior lens deposit resistance.

The Frequent replacement lenses segment was valued at USD 263.5 million in 2024 and showed a gradual increase during the forecast period.

What are the key Drivers, Trends, and Challenges in the India Contact Lens Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the contact lens market in India requires a nuanced understanding of consumer priorities, which increasingly weigh the benefits of different modalities and materials against cost. When considering the best contact lens for digital eye strain, for example, consumers are learning to prioritize features like advanced moisture retention and a stable tear film over initial price.

- The daily disposable vs monthly contact lens comparison is a central decision point, with daily lenses offering a 90% reduction in risks associated with lens case contamination but at a higher annual cost. For those with specific vision needs, the cost of toric lenses for astigmatism is a key consideration, though improved fitting success rates are making them more accessible.

- Effectively managing dry eye with contact lenses remains a significant challenge, prompting a search for solutions that go beyond standard lens care. As consumers research how to improve contact lens comfort, they encounter a complex landscape of materials, replacement schedules, and care regimens, making practitioner education and clear digital resources critical for market growth and user retention.

What are the key market drivers leading to the rise in the adoption of India Contact Lens Industry?

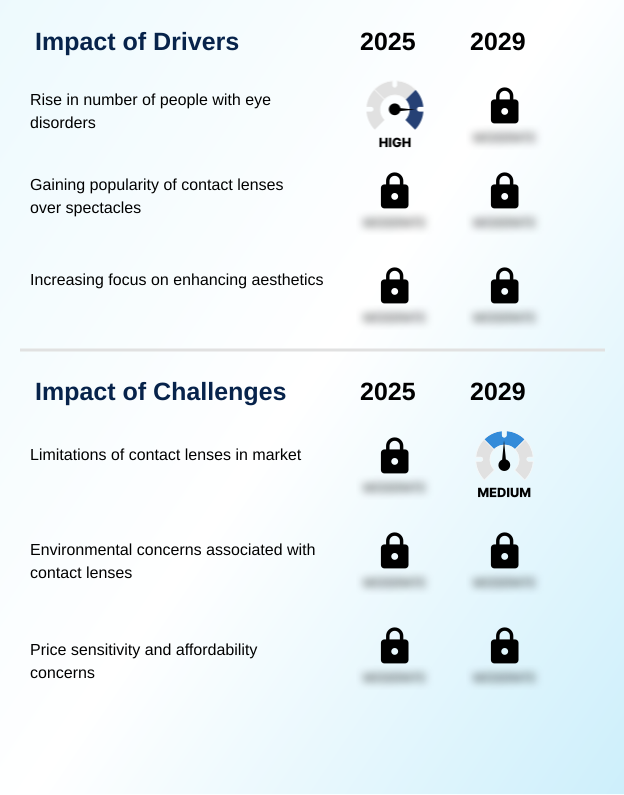

- The primary market driver is the significant surge in myopia prevalence and digital eye strain, particularly among younger demographics, linked to increased screen time and changing lifestyles.

- The primary driver fueling the contact lens market in India is the escalating prevalence of refractive errors, with myopia rates among adolescents in urban areas having increased by over 30% in the last decade.

- This surge is directly linked to lifestyle changes, including a significant rise in digital eye strain from prolonged screen use.

- As a result, there is a growing demand not just for vision correction but for solutions that actively manage eye health, such as lenses designed for myopia control or those offering enhanced comfort for computer users.

- This has spurred a 20% increase in consultations focused on advanced lens options.

- The market is responding with specialized products, including multifocal optics and orthokeratology solutions, supported by robust practitioner education to improve fitting success rates and overall visual acuity for users.

What are the market trends shaping the India Contact Lens Industry?

- A predominant trend is the accelerating consumer migration toward silicone hydrogel daily disposables, driven by a growing prioritization of ocular health, comfort, and convenience over the cost advantages of older modalities.

- A defining trend in the contact lens market in India is the accelerated consumer upgrade to lenses offering superior ocular health benefits, with sales of products featuring UV blocking filters growing by 25%. This shift is driven by increasing awareness of long-term eye health and a demand for higher-performance materials.

- The adoption of the daily disposable modality, particularly in urban areas, is a direct response to consumer demand for convenience and hygiene, significantly reducing risks tied to improper lens care. This trend has compelled manufacturers to innovate in polymer chemistry, leading to the introduction of advanced silicone hydrogel and water gradient technology that enhances wearer comfort and oxygen transmissibility.

- Consequently, the industry's supply chain is adapting with investments in cold chain distribution to protect the integrity of these advanced, high-moisture products during transit.

What challenges does the India Contact Lens Industry face during its growth?

- A key challenge is the high rate of user discontinuation, largely due to ocular health complications such as discomfort and dryness, which are often exacerbated by environmental factors and non-compliance with care routines.

- The most significant challenge constraining the contact lens market in India is the high user discontinuation rate, with studies indicating that nearly 40% of new wearers cease usage within the first year.

- This is primarily caused by contact lens intolerance issues like dry eye syndrome and discomfort, which are often worsened by the country's prevalent air quality impact, leading to increased lens deposit resistance issues. A secondary factor is poor patient compliance with recommended replacement schedules and lens care solution protocols, leading to a higher incidence of complications such as microbial keratitis.

- These negative experiences, which can cause epithelial abrasion, create a substantial barrier to sustained market growth, as the rate of user churn counteracts the influx of new wearers, limiting the expansion of the user base by an estimated 15% annually.

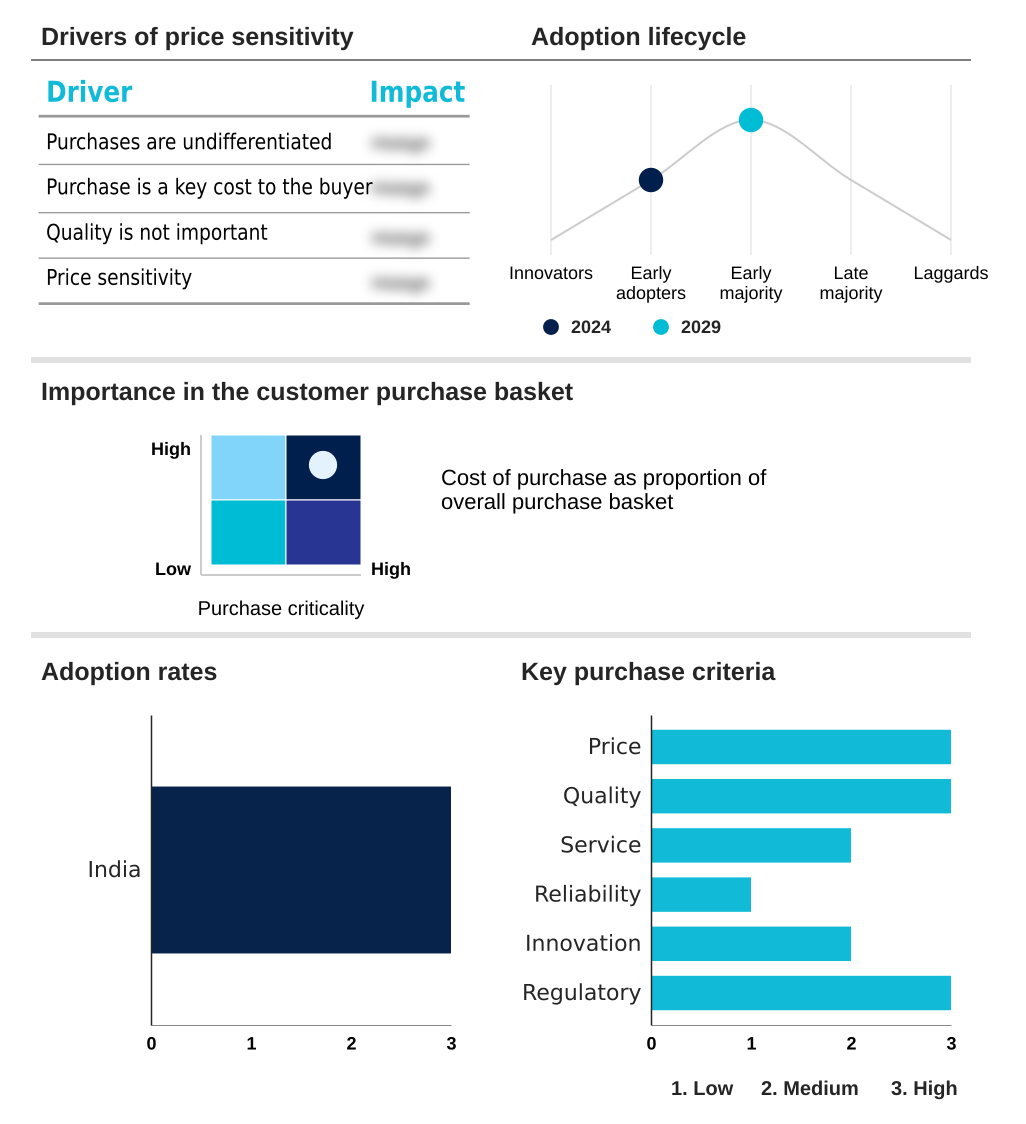

Exclusive Technavio Analysis on Customer Landscape

The india contact lens market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the india contact lens market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of India Contact Lens Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, india contact lens market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Optical Group LLC - Key offerings encompass a wide portfolio of vision correction products, including specialized and custom optical solutions designed to address diverse patient needs and clinical requirements.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Optical Group LLC

- Accurate Optics India

- Alcon Inc.

- Aqualens

- Bausch and Lomb Pvt Ltd.

- Care Group Sight Solution Pvt. Ltd.

- Carl Zeiss AG

- Cooper Vision Inc.

- Excellent Hi Care Pvt. Ltd.

- GKB HI-TECH PRIVATE LIMITED

- Himalaya Opticals

- Johnson and Johnson Services

- SEED Co. Ltd.

- STAAR Surgical Co.

- Titan Co. Ltd.

- Transe Vision Care Pvt Ltd.

- Truviz Ophthalmic

- UltraVision CLPL

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Personal Care Products industry, the widespread adoption of direct-to-consumer (DTC) e-commerce platforms has fundamentally altered distribution strategies, directly enabling contact lens brands to bypass traditional retail and engage consumers through subscription models, which enhances patient compliance.

- A heightened focus on personalization, driven by AI and data analytics, is compelling manufacturers to move beyond mass-market items. This trend pressures the contact lens market to offer more customized solutions, such as lenses tailored for digital eye strain or specific astigmatism correction, moving away from one-size-fits-all products.

- Increasingly stringent regulations on material safety and biocompatibility are forcing a reassessment of polymer chemistry across the sector. For the contact lens market, this translates to higher R&D investment in bio-inspired materials and advanced surface coating technology to meet new health and safety benchmarks, impacting production costs.

- The push toward sustainability and reduced packaging waste is creating new operational challenges. This shift requires contact lens manufacturers to innovate in packaging, such as reducing plastic in blister packs and adopting recycled materials, to align with consumer and regulatory demands for a smaller environmental footprint.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled India Contact Lens Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 170 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.1% |

| Market growth 2026-2030 | USD 173.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.8% |

| Key countries | India |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The contact lens market in India operates within a complex ecosystem where raw material suppliers providing advanced polymers and monomers are critical upstream partners.

- These materials are transformed by manufacturers like Alcon Inc., Johnson and Johnson Services, and Bausch and Lomb Pvt Ltd., who command over 70% of the market share, into a range of products from daily disposables to specialty toric lenses. The value chain is heavily influenced by regulatory bodies that govern medical devices, setting stringent standards for market entry.

- Distribution is bifurcated into offline channels, such as optometrists and optical stores, and a rapidly growing online channel, which has seen a 35% increase in user adoption in urban centers. This channel relies on sophisticated supply chain logistics for prescription verification and fulfillment.

- End-users interact with this ecosystem through eye care practitioners, whose prescribing habits and practitioner education significantly shape market dynamics.

What are the Key Data Covered in this India Contact Lens Market Research and Growth Report?

-

What is the expected growth of the India Contact Lens Market between 2026 and 2030?

-

The India Contact Lens Market is expected to grow by USD 173.7 million during 2026-2030, registering a CAGR of 6.1%. Year-over-year growth in 2026 is estimated at 5.8%%. This acceleration is shaped by surge in myopia prevalence and digital eye strain, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Frequent replacement lenses, and Daily disposable lenses), Distribution Channel (Online, and Offline), Application (Corrective lens, Therapeutic lens, and Cosmetic lens) and Geography (APAC). Among these, the Frequent replacement lenses segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC. Country-level analysis includes India, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is surge in myopia prevalence and digital eye strain, which is accelerating investment and industry demand. The main challenge is ocular health complications and high discontinuation rates, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the India Contact Lens Market?

-

Key vendors include ABB Optical Group LLC, Accurate Optics India, Alcon Inc., Aqualens, Bausch and Lomb Pvt Ltd., Care Group Sight Solution Pvt. Ltd., Carl Zeiss AG, Cooper Vision Inc., Excellent Hi Care Pvt. Ltd., GKB HI-TECH PRIVATE LIMITED, Himalaya Opticals, Johnson and Johnson Services, SEED Co. Ltd., STAAR Surgical Co., Titan Co. Ltd., Transe Vision Care Pvt Ltd., Truviz Ophthalmic and UltraVision CLPL. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape in the contact lens market in India is intensifying, with omnichannel distribution now accounting for over 30% of sales strategies. Throughout the past year, major players like Carl Zeiss, Alcon Inc., and domestic leader Aqualens have focused on deepening their market penetration beyond metropolitan areas.

- Carl Zeiss inaugurated a new capability center to enhance digital transformation, aiming to improve lens fitting precision for optometrists. Similarly, Alcon Inc. launched its Total Vision Academy, a professional education program designed to reduce the new user dropout rate, which currently stands at nearly 40%, by improving fitting protocols for its advanced water gradient lenses.

- Meanwhile, Aqualens commissioned an automated fulfillment hub to reduce delivery timelines for its daily disposable range. These strategic moves highlight a market where competitive advantage is shifting from price alone to supply chain efficiency and professional support infrastructure.

We can help! Our analysts can customize this india contact lens market research report to meet your requirements.

RIA -

RIA -