Cloud Security Solutions Market Size 2026-2030

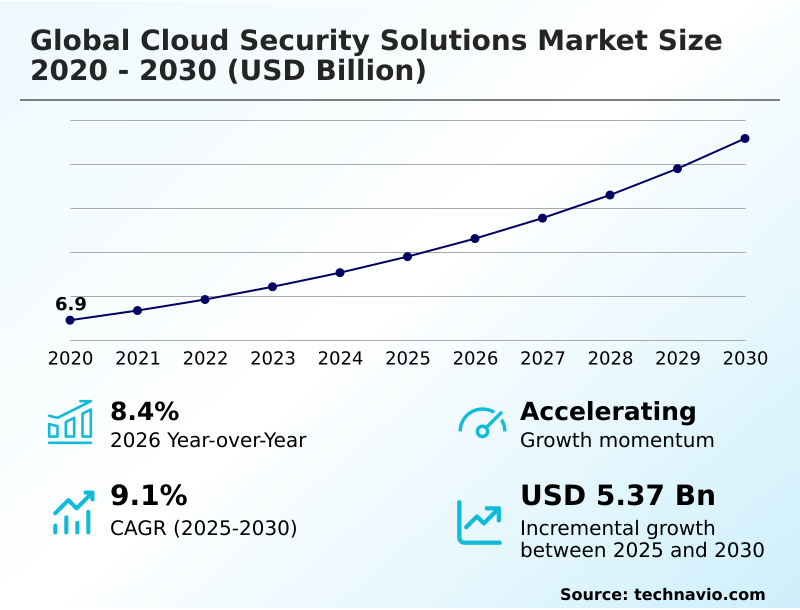

The Cloud Security Solutions Market size was valued at USD 9.79 billion in 2025, growing at a CAGR of 9.1% during the forecast period 2026-2030.

Major Market Trends & Insights

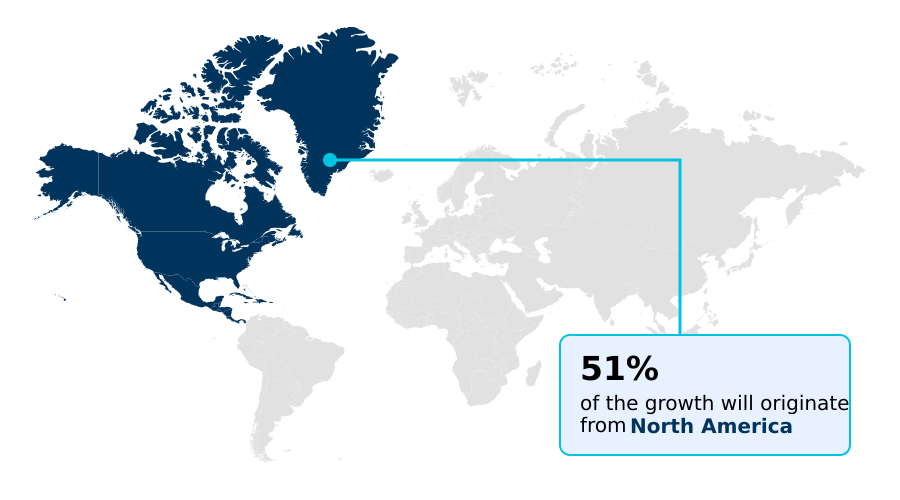

- North America dominated the market and accounted for a 51.1% growth during the forecast period.

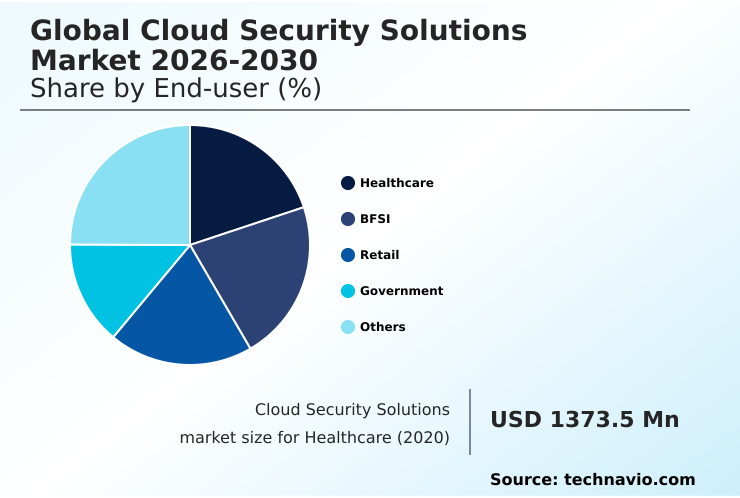

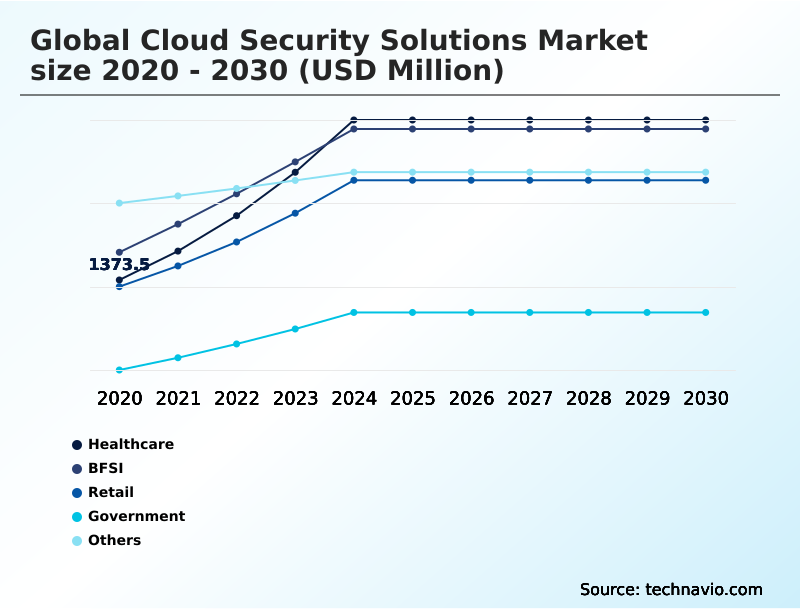

- By End-user - Healthcare segment was valued at USD 2.10 billion in 2024

- By Component - Cloud IAM segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 8.26 billion

- Market Future Opportunities 2025-2030: USD 5.37 billion

- CAGR from 2025 to 2030 : 9.1%

Market Summary

- The cloud security solutions market is defined by a rapid investment cycle, with organizations increasing their security budgets by an average of 12% annually to counter evolving threats. This spending is a direct response to the rising sophistication of cyberattacks, which now leverage AI to bypass traditional defenses.

- For example, a retail business migrating to a multi-cloud environment for its e-commerce platform must secure customer data across AWS and Azure, a task complicated by a 30% rise in cross-platform attacks. The primary driver is the low cost of ownership for cloud-native security, which can reduce total security expenditure by up to 20% compared to on-premise solutions.

- However, a major challenge is the persistent cybersecurity skills gap, which leaves many organizations unable to manage these advanced tools effectively, thereby increasing their risk exposure despite higher spending. This necessitates a move towards managed detection and response services.

What will be the Size of the Cloud Security Solutions Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Cloud Security Solutions Market Segmented?

The cloud security solutions industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Healthcare

- BFSI

- Retail

- Government

- Others

- Component

- Cloud IAM

- Cloud e-mail security

- Cloud DLP

- Cloud IDS or IPS

- Cloud SIEM

- Deployment

- Private

- Public

- Hybrid

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

How is the Cloud Security Solutions Market Segmented by End-user?

The healthcare segment is estimated to witness significant growth during the forecast period.

The healthcare segment's adoption of cloud security solutions is driven by data protection mandates, with 95% of organizations prioritizing compliance automation to meet regulatory requirements.

In this sector, protecting patient data within multi-cloud environments has led to a 15% improvement in breach prevention through the deployment of advanced cloud IAM and privileged access management systems.

This contrasts with other industries where the focus might be on cost reduction.

Consequently, healthcare providers are investing in specialized cloud workload protection platforms that offer robust data encryption standards and continuous security monitoring, ensuring that security policy enforcement aligns with stringent healthcare laws and reduces the risk of non-compliance penalties by over 20%.

The use of a web application firewall is now standard practice.

The Healthcare segment was valued at USD 2.10 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Cloud Security Solutions market is rising in the leading region?

North America is estimated to contribute 51.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cloud Security Solutions Market demand is rising in North America Request Free Sample

Regional disparities define the cloud security solutions market, with North America representing 51.1% of the incremental growth, a share nearly 2.5 times larger than Europe's 21.51%.

This dominance is propelled by the United States, which constitutes over 82% of the North American market, driven by stringent regulations that mandate advanced API security and compliance automation.

In contrast, the APAC market, contributing 19.58% to growth, exhibits a different adoption pattern centered on mobile device management for its expanding e-commerce sector, where security misconfiguration is a primary concern.

This results in a 20% higher investment in data encryption standards and cloud IAM tools in North America compared to APAC, where scalable, cost-effective solutions are prioritized to support rapid digitalization and address the cybersecurity skills gap.

What are the key Drivers, Trends, and Challenges in the Cloud Security Solutions Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprise adoption of cloud security solutions is driven by the need to manage complex digital ecosystems, with a notable 15% year-over-year increase in spending on tools for multi-cloud environments. As organizations navigate digital transformation, understanding the best practices for cloud data protection is paramount to preventing breaches that have seen a 25% rise in sophistication.

- A key strategy involves implementing a zero trust security model, a framework that has been shown to reduce lateral movement by attackers within a network by over 80%. This approach requires robust cloud IAM and privileged access management. Automating cloud compliance and governance has become essential, with businesses using these tools to reduce audit preparation time by up to 40%.

- This is especially critical for managing security risks in hybrid cloud architectures, where the attack surface is inherently larger. The total cost of cloud security solutions is a major consideration, but the expense is increasingly viewed as a necessary investment to mitigate the far greater financial and reputational damage from a potential security incident.

What are the key market drivers leading to the rise in the adoption of Cloud Security Solutions Industry?

- Favorable regulatory requirements that encourage the use of security solutions are a key driver of market growth.

- Favorable regulatory requirements are a key driver, with mandates like GDPR leading to a 35% increase in demand for cloud security solutions that offer compliance automation and data residency rules.

- This legal pressure makes security spending non-negotiable, as non-compliance fines often exceed implementation costs by more than tenfold.

- Consequently, organizations are prioritizing solutions with built-in regulatory compliance frameworks, such as those offering automated security auditing, which can reduce audit preparation times by over 50%.

- This driver ensures a steady demand cycle, independent of economic fluctuations, as businesses invest in advanced data loss prevention (DLP) and cloud SIEM systems to meet their legal obligations and avoid severe financial penalties.

What are the market trends shaping the Cloud Security Solutions Industry?

- The increasing prevalence of remote work arrangements is significantly accelerating the expansion of the market. This shift necessitates robust security measures to protect decentralized data and access points.

- The growth of the remote workforce is a primary trend boosting market expansion, compelling a 40% rise in the adoption of zero trust network access architectures. This shift decentralizes security, focusing on identity as the new perimeter.

- As a result, businesses are investing in identity as a service (IDaaS) and secure access service edge platforms, leading to a 25% improvement in secure access for distributed employees. This evolution reflects a broader move away from traditional, centralized security models toward more agile, user-centric protection strategies.

- The integration of mobile device management has become critical for securing corporate data on a proliferating number of personal and company-owned devices, directly addressing risks associated with bring-your-own-device policies and ensuring continuous security monitoring.

What challenges does the Cloud Security Solutions Industry face during its growth?

- A significant lack of awareness among end-users regarding cloud security solutions is a key challenge that affects industry growth.

- A significant lack of awareness among end-users about the shared responsibility model remains a major market challenge, contributing to a 60% higher rate of security misconfiguration incidents in small and medium-sized enterprises compared to large corporations.

- This knowledge gap leads to underinvestment in essential tools like cloud workload protection and security posture management, as many businesses mistakenly assume the cloud provider handles all security. The complexity of modern multi-cloud environments further exacerbates this issue, with IT teams reporting a 30% increase in difficulty maintaining consistent security policy enforcement across different platforms.

- This challenge is compounded by the cybersecurity skills gap, hindering the effective deployment and management of sophisticated defense systems like privileged access management.

Exclusive Technavio Analysis on Customer Landscape

The cloud security solutions market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cloud security solutions market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cloud Security Solutions Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cloud security solutions market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Akamai Technologies Inc. - Offerings include advanced security solutions such as web application protection and enterprise threat defense, focusing on safeguarding digital assets against a wide range of cyber threats.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Akamai Technologies Inc.

- Amazon.com Inc.

- Broadcom Inc.

- Cisco Systems Inc.

- Cloudflare Inc.

- CrowdStrike Inc.

- Dell Technologies Inc.

- Fortinet Inc.

- IBM Corp.

- Intel Corp.

- Lookout Inc.

- Microsoft Corp.

- NTT DATA Corp.

- Palo Alto Networks Inc.

- Qualys Inc.

- Tenable Holdings Inc.

- Thales Group

- Trend Micro Inc.

- WatchGuard Technologies Inc.

- Zscaler Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Systems Software industry, the increasing complexity of multi-cloud architectures has created a significant demand for unified management platforms, directly boosting the cloud security solutions market by necessitating sophisticated access control governance and security policy enforcement tools to maintain visibility across disparate environments.

- The widespread adoption of agile and DevOps methodologies has shifted security requirements left into the development lifecycle, fueling the need for infrastructure as code security and automated security auditing tools within the cloud security solutions portfolio to address vulnerabilities before deployment.

- Growing enforcement of data privacy regulations, such as GDPR and CCPA, is compelling organizations to invest in solutions that ensure data residency rules and compliance automation, creating a non-discretionary spending category for cloud security solutions that feature advanced data encryption standards and sovereign cloud capabilities.

- The surge in enterprise adoption of containerization and serverless computing technologies has created a new attack surface, driving the development and adoption of specialized container security and serverless security solutions to protect ephemeral workloads, which has become a primary growth area.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cloud Security Solutions Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 322 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.1% |

| Market growth 2026-2030 | USD 5368.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.4% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The cloud security solutions market ecosystem functions through a complex interplay of stakeholders, with technology suppliers providing the core components like encryption algorithms and threat intelligence feeds, which see a 15% annual update cycle.

- Solution providers, such as major software corporations and specialized cybersecurity firms, then integrate these components into comprehensive platforms offering cloud IAM and data loss prevention, which hold a combined 45% share of the market. Regulatory bodies and standards organizations define the compliance frameworks that drive demand.

- Distribution is handled through direct sales teams, managed security service providers (MSSPs), and cloud marketplaces, with MSSPs experiencing a 20% growth in adoption. End-users across healthcare, finance, and retail consume these services to protect their digital assets, while R&D entities continuously innovate to counter emerging threats.

What are the Key Data Covered in this Cloud Security Solutions Market Research and Growth Report?

-

What is the expected growth of the Cloud Security Solutions Market between 2026 and 2030?

-

The Cloud Security Solutions Market is expected to grow by USD 5.37 billion during 2026-2030, registering a CAGR of 9.1%. Year-over-year growth in 2026 is estimated at 8.4%%. This acceleration is shaped by favourable regulatory requirements encouraging use of security solutions, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Healthcare, BFSI, Retail, Government, and Others), Component (Cloud IAM, Cloud e-mail security, Cloud DLP, Cloud IDS or IPS, and Cloud SIEM), Deployment (Private, Public, and Hybrid) and Geography (North America, Europe, APAC, Middle East and Africa, South America). Among these, the Healthcare segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, Middle East and Africa and South America. North America is estimated to contribute 51.1% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is favourable regulatory requirements encouraging use of security solutions, which is accelerating investment and industry demand. The main challenge is lack of awareness about cloud security solutions among end user, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Cloud Security Solutions Market?

-

Key vendors include Akamai Technologies Inc., Amazon.com Inc., Broadcom Inc., Cisco Systems Inc., Cloudflare Inc., CrowdStrike Inc., Dell Technologies Inc., Fortinet Inc., IBM Corp., Intel Corp., Lookout Inc., Microsoft Corp., NTT DATA Corp., Palo Alto Networks Inc., Qualys Inc., Tenable Holdings Inc., Thales Group, Trend Micro Inc., WatchGuard Technologies Inc. and Zscaler Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The cloud security solutions vendor landscape includes over 20 major providers, with the top five controlling approximately 40% of market revenue. Key players like Microsoft Corp. and Palo Alto Networks Inc. are consolidating the market through strategic acquisitions, with at least three major deals in the last fiscal period focusing on AI-driven threat detection.

- This trend addresses enterprise demand for integrated security stacks, which can reduce vendor complexity by up to 25% for a typical large organization. Other companies, including Zscaler Inc. and CrowdStrike Inc., are focusing on organic innovation and partnerships to enhance their secure access service edge (SASE) and endpoint protection platforms.

- This intense competition is a direct response to the increasing sophistication of cyber threats and the need for interoperable security layers to protect distributed corporate networks from complex attacks.

We can help! Our analysts can customize this cloud security solutions market research report to meet your requirements.

RIA -

RIA -