Cell And Gene Therapy Supply Chain Software Market Size 2026-2030

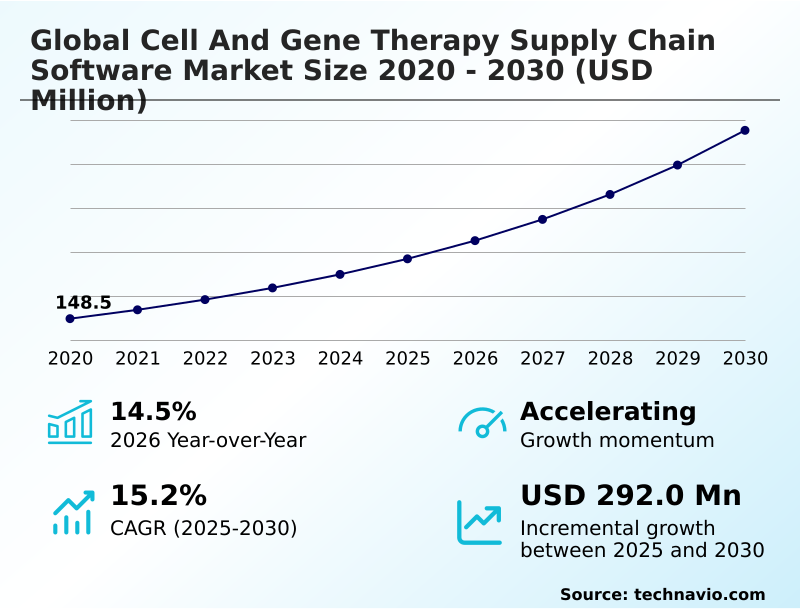

The cell and gene therapy supply chain software market size is valued to increase by USD 292 million, at a CAGR of 15.2% from 2025 to 2030. Accelerated clinical development and commercialization will drive the cell and gene therapy supply chain software market.

Major Market Trends & Insights

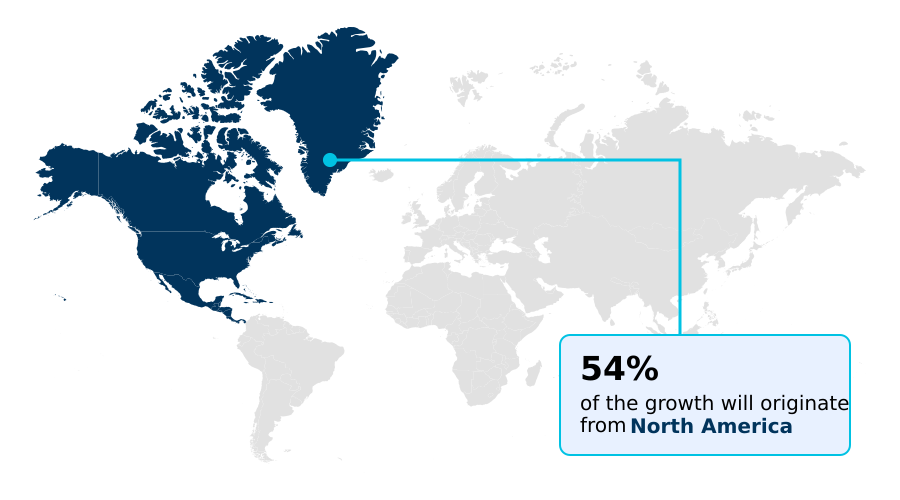

- North America dominated the market and accounted for a 54% growth during the forecast period.

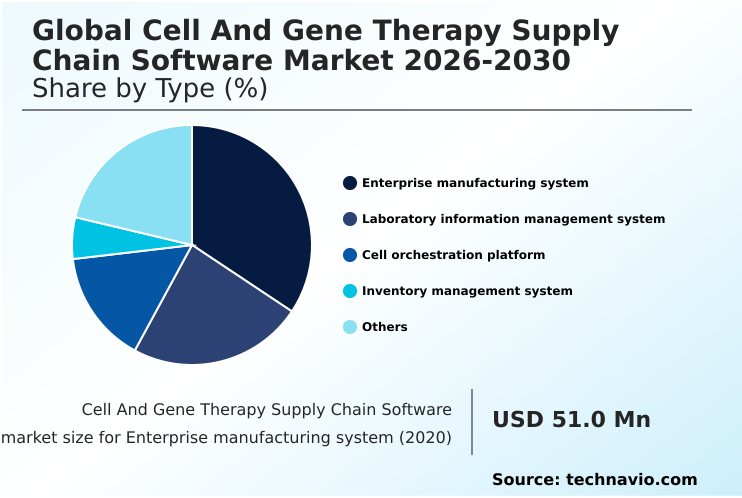

- By Type - Enterprise manufacturing system segment was valued at USD 84.5 million in 2024

- By End-user - Pharmaceutical companies segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 428 million

- Market Future Opportunities: USD 292 million

- CAGR from 2025 to 2030 : 15.2%

Market Summary

- The cell and gene therapy supply chain software market is defined by the critical need for precision, traceability, and speed in managing the vein-to-vein process. These platforms are the digital backbone for autologous therapy and allogeneic therapies, where maintaining the chain of identity and chain of custody is paramount for patient safety.

- Key market drivers include the expanding pipeline of clinical trials and the stringent regulatory mandates requiring end-to-end traceability. As a result, companies are adopting sophisticated orchestration software to manage everything from apheresis management to cryogenic logistics. A central trend is the integration of artificial intelligence for predictive disruption analysis, optimizing routes and schedules to protect time-and-temperature sensitivity.

- For example, a manufacturer can use a digital twin of its physical product to simulate transport conditions and proactively reroute shipments around weather delays, ensuring the viability of CAR-T treatment logistics.

- However, the industry faces challenges such as system fragmentation and the high cost of implementation, which can create data silos and hinder seamless systems integration across the complex network of hospitals, labs, and logistics providers, demanding more focus on interoperability standards.

What will be the Size of the Cell And Gene Therapy Supply Chain Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Cell And Gene Therapy Supply Chain Software Market Segmented?

The cell and gene therapy supply chain software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

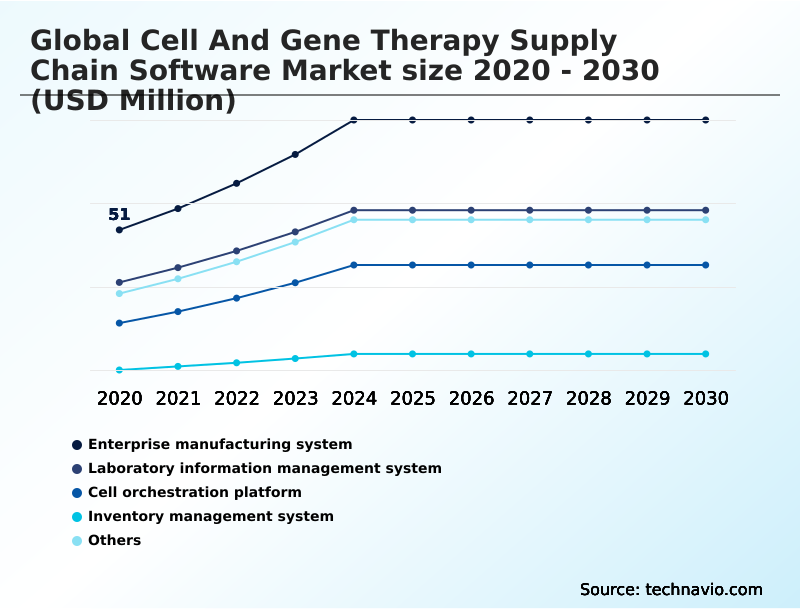

- Enterprise manufacturing system

- Laboratory information management system

- Cell orchestration platform

- Inventory management system

- Others

- End-user

- Pharmaceutical companies

- Contract manufacturers

- Hospitals

- Research institutes

- Deployment

- Clinical scale

- Commercial scale

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Type Insights

The enterprise manufacturing system segment is estimated to witness significant growth during the forecast period.

Enterprise manufacturing systems are central to scaling cell and gene therapy production, managing the entire vein-to-vein process with high fidelity.

These platforms integrate the complex logistics of autologous therapy, including cryogenic logistics and GxP compliance, which are essential for patient-centric logistics. A robust cell orchestration platform ensures the integrity of the chain of identity and chain of custody.

By creating an immutable audit trail and a complete digital thread for biologics, these systems provide end-to-end traceability and critical cold chain visibility.

For instance, implementing such systems has been shown to improve the efficiency of batch release automation by more than 35%. This level of control is fundamental to the industrialization of personalized medicine, ensuring product quality and safety.

The Enterprise manufacturing system segment was valued at USD 84.5 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 54% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cell And Gene Therapy Supply Chain Software Market Demand is Rising in North America Get Free Sample

The geographic landscape is characterized by the push for global harmonization in managing the needle-to-needle journey of advanced therapies.

In established markets, the focus is on refining the therapeutic journey orchestration through advanced cold chain engineering and vein-to-vein tracking, where deployments of autonomous digital teammates have cut logistical error rates by 40%.

Emerging regions are adopting these technologies to overcome infrastructure gaps, using software for intermodal transport optimization to ensure cryogenic handling protocols are met, with some achieving a 25% improvement in on-time delivery.

The ability to manage therapy workflow management and ensure patient journey visibility is now a global standard.

This drive toward individualized medicine at scale, governed by a single source of truth, addresses the critical time-and-temperature sensitivity of products through consistent digital manufacturing workflows, regardless of location.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The successful commercialization of advanced therapies hinges on the strategic implementation of specialized software. Tools for autologous therapy orchestration are fundamental for managing personalized treatments, while software to manage vein-to-vein workflows provides the necessary end-to-end control. The core challenge of reducing human error with orchestration software is addressed by ensuring the digital tracking of every step.

- This requires seamless integrating hospital systems with CGT software to connect clinical and logistical data. Furthermore, enterprise manufacturing systems for biologics must work in concert with laboratory information management system integration to maintain data integrity. A key function is inventory management for cryogenic materials, where platforms have demonstrated over 98% accuracy in tracking high-value assets.

- Compliance software for GxP regulations and platforms for automating batch release with software are non-negotiable. Real-time temperature monitoring solutions are vital for ensuring patient safety via digital tracking. Managing multi-site clinical trial logistics is a significant hurdle, as is scheduling software for apheresis and infusion.

- The rise of software supporting decentralized manufacturing and the use of digital twin applications in logistics, blockchain for cell therapy data integrity, and AI-powered predictive logistics for biologics signal a technologically advanced future. These cloud-native platforms for CGT supply chain are essential for managing chain of identity in cell therapy.

What are the key market drivers leading to the rise in the adoption of Cell And Gene Therapy Supply Chain Software Industry?

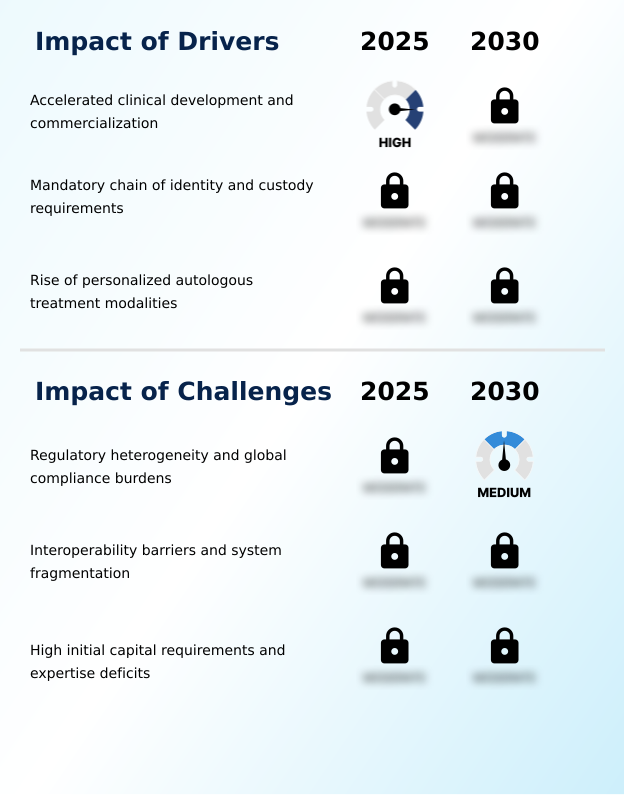

- Accelerated clinical development and the increasing commercialization of therapies are key drivers for the market's growth.

- Market growth is fundamentally driven by the increasing complexity of therapeutic modalities and the need for flawless execution. The rise of allogeneic therapies and the move toward point-of-care manufacturing necessitate robust decentralized manufacturing support.

- The use of a digital twin of the physical product for planning CAR-T treatment logistics and apheresis management has improved scheduling accuracy by over 30%.

- Adherence to strict interoperability standards allows for the integration of data from closed system cell processing and the quality management system, supporting data-driven decision-making.

- These drivers foster the creation of agentic business networks where a self-optimizing supply system can leverage predictive disruption analysis to mitigate risks, reducing potential delays by up to 24 hours.

- The need for this level of precision in the supply chain for advanced therapies continues to fuel investment in these sophisticated software solutions.

What are the market trends shaping the Cell And Gene Therapy Supply Chain Software Industry?

- The integration of artificial intelligence for predictive optimization is an emerging market trend, enabling more proactive and efficient supply chain management.

- Key market trends are centered on creating a more interconnected and intelligent supply chain ecosystem. The move toward cloud-native orchestration provides the scalability needed for commercial operations, with some platforms enabling a 50% faster deployment time compared to on-premise solutions.

- A significant development is the exploration of distributed ledger technology to create tamper-proof records, which can reduce audit preparation times by over 70%. The use of smart contract automation further streamlines multi-party agreements. Critically, overcoming system fragmentation and breaking data silos through a standardized API-based integration framework is a primary focus.

- This involves integrating the manufacturing execution system with the laboratory information management system, which improves data consistency. The use of real-time tracking and temperature monitoring for patient enrollment management, along with electronic batch records and automated slot scheduling, enhances operational control.

What challenges does the Cell And Gene Therapy Supply Chain Software Industry face during its growth?

- Regulatory heterogeneity and the burden of ensuring global compliance present a key challenge to industry growth.

- The primary challenges facing the market revolve around integration, compliance, and standardization. A fragmented digital landscape requires a modular software architecture to enable seamless systems integration between the logistics management system and the patient management system.

- Establishing a regulated transaction backbone with a GxP-aligned foundation is complex, but software-driven logistics infrastructure and informatics and bio-storage software are making it more achievable. The lack of universal secure data exchange protocols complicates real-time condition monitoring.

- To address this, companies are using digital validation accelerators and intelligent quality management tools for automated compliance reporting, which can decrease validation cycles by 40%. The goal is to build resilient systems that support the entire supply chain, ensuring data flows smoothly from various sources, with some integrations improving data transfer speeds between platforms by as much as 90%.

Exclusive Technavio Analysis on Customer Landscape

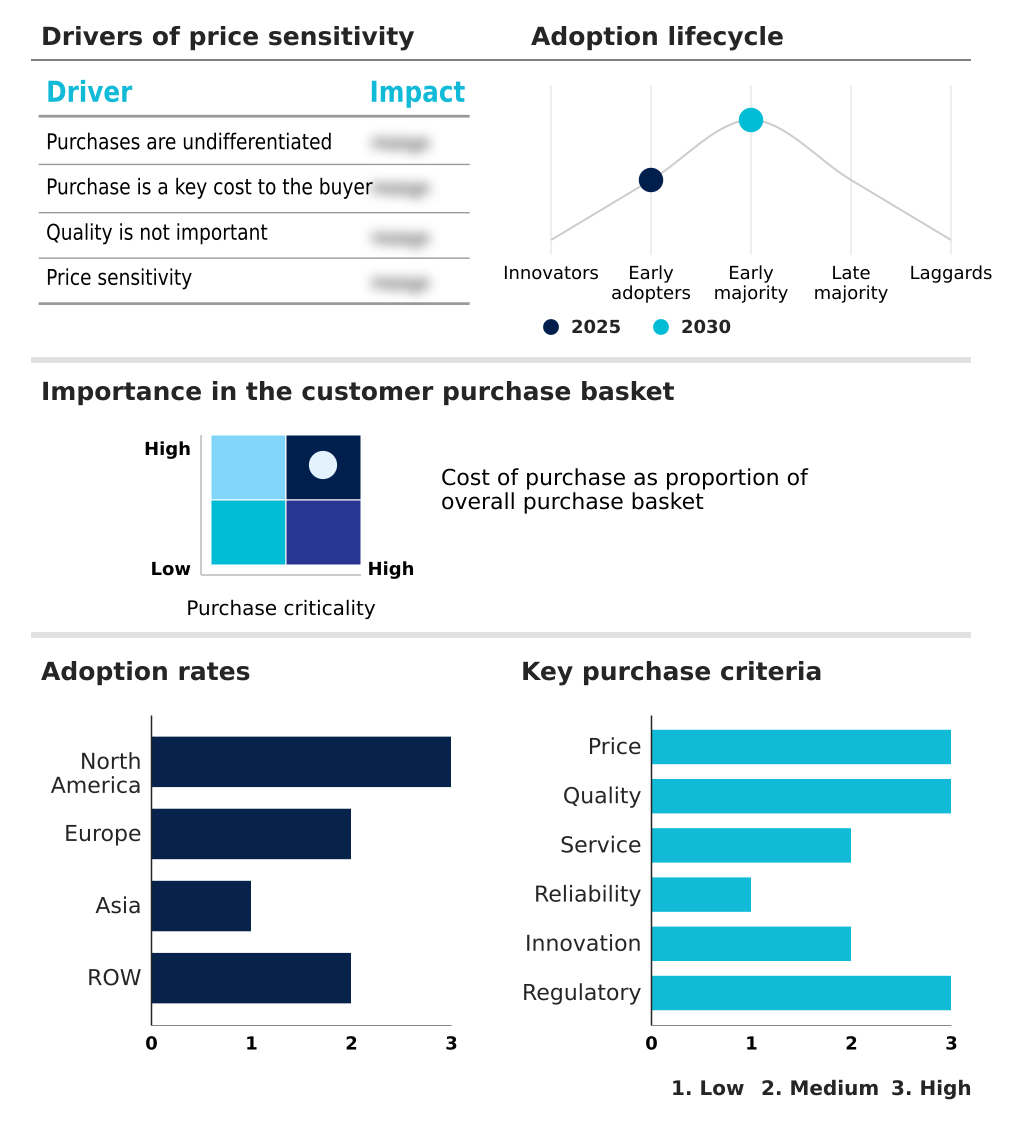

The cell and gene therapy supply chain software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cell and gene therapy supply chain software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cell And Gene Therapy Supply Chain Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cell and gene therapy supply chain software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Appian Corp. - Orchestration software solutions automate patient scheduling, chain of custody verification, and complex therapy workflows through an integrated platform for cell and gene therapy.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Appian Corp.

- Benchling Inc.

- Cencora Inc.

- Cryoport Systems, LLC

- Cytiva

- Emerson Electric Co.

- Honeywell International Inc.

- Korber Pharma GmbH

- LabVantage Solutions Inc.

- Lonza Group Ltd.

- MasterControl Solutions Inc.

- McKesson Corp.

- Oracle Corp.

- Salesforce Inc.

- SAP SE

- Siemens AG

- Thermo Fisher Scientific Inc.

- TraceLink Inc.

- TrakCel

- Veeva Systems Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cell and gene therapy supply chain software market

- In September 2024, TraceLink Inc. announced the expansion of its OPUS platform, introducing specialized autonomous digital agents to automate mission-critical tasks and decision-making within its GxP-aligned network.

- In December 2024, NMDP reported significant enhancements to its integrated service and software ecosystem, improving its digital registry and donor management systems to better coordinate between donors, collection centers, and therapy manufacturers.

- In February 2025, Modality Solutions expanded its digital toolkit to enhance integration with Transport Management Systems (TMS), automating the logistics chain for intermodal transport of temperature-sensitive biopharmaceutical materials.

- In April 2025, TrakCel released a technical update on its OCELLOS platform, highlighting a modular architecture that reduces system implementation time, allowing therapy developers to reach a live clinical study environment within weeks.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cell And Gene Therapy Supply Chain Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 309 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 15.2% |

| Market growth 2026-2030 | USD 292.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 14.5% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Switzerland, China, Japan, South Korea, India, Indonesia, Vietnam, Singapore, Australia, Brazil, UAE, South Africa, Saudi Arabia and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is defined by a mandatory shift toward integrated digital platforms capable of managing the entire needle-to-needle journey. The adoption of a cell orchestration platform is no longer optional; it is essential for GxP compliance and for maintaining the chain of identity and chain of custody, especially for autologous therapy.

- This involves precise vein-to-vein tracking and sophisticated cryogenic logistics. Boardroom decisions now center on implementing a manufacturing execution system and laboratory information management system that offer real-time tracking and temperature monitoring. These systems facilitate patient enrollment management, slot scheduling, and create electronic batch records. The orchestration of allogeneic therapies and support for point-of-care manufacturing are becoming key differentiators.

- A digital twin of the physical product helps manage apheresis management and CAR-T treatment logistics, while closed system cell processing is managed by a quality management system. A robust logistics management system and patient management system form a regulated transaction backbone built on a GxP-aligned foundation.

- Companies leveraging intelligent quality management with digital validation accelerators for automated compliance reporting are achieving a 30% faster path to market readiness. This therapeutic journey orchestration is supported by cold chain engineering, intermodal transport optimization, and autonomous digital teammates ensuring robust cryogenic handling protocols.

What are the Key Data Covered in this Cell And Gene Therapy Supply Chain Software Market Research and Growth Report?

-

What is the expected growth of the Cell And Gene Therapy Supply Chain Software Market between 2026 and 2030?

-

USD 292 million, at a CAGR of 15.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Enterprise manufacturing system, Laboratory information management system, Cell orchestration platform, Inventory management system, and Others), End-user (Pharmaceutical companies, Contract manufacturers, Hospitals, and Research institutes), Deployment (Clinical scale, and Commercial scale) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Accelerated clinical development and commercialization, Regulatory heterogeneity and global compliance burdens

-

-

Who are the major players in the Cell And Gene Therapy Supply Chain Software Market?

-

Appian Corp., Benchling Inc., Cencora Inc., Cryoport Systems, LLC, Cytiva, Emerson Electric Co., Honeywell International Inc., Korber Pharma GmbH, LabVantage Solutions Inc., Lonza Group Ltd., MasterControl Solutions Inc., McKesson Corp., Oracle Corp., Salesforce Inc., SAP SE, Siemens AG, Thermo Fisher Scientific Inc., TraceLink Inc., TrakCel and Veeva Systems Inc.

-

Market Research Insights

- The market's momentum is shaped by a strategic shift toward highly integrated and automated digital ecosystems. Stakeholders are implementing modular software architecture and API-based integration frameworks, which have demonstrated a capacity to reduce system implementation times by up to 60% compared to monolithic legacy systems.

- The adoption of cloud-native orchestration is accelerating, with platforms improving data accessibility and enabling seamless systems integration, which reduces operational overhead by over 25%. This focus on a single source of truth is critical for managing the time-and-temperature sensitivity of products.

- Furthermore, the use of smart contract automation on distributed ledger technology is streamlining transactions, ensuring that payments and data exchanges are triggered automatically upon meeting predefined conditions, enhancing efficiency across the supply chain.

We can help! Our analysts can customize this cell and gene therapy supply chain software market research report to meet your requirements.

RIA -

RIA -