Battery For Energy Storage Systems (ESS) Market Size 2026-2030

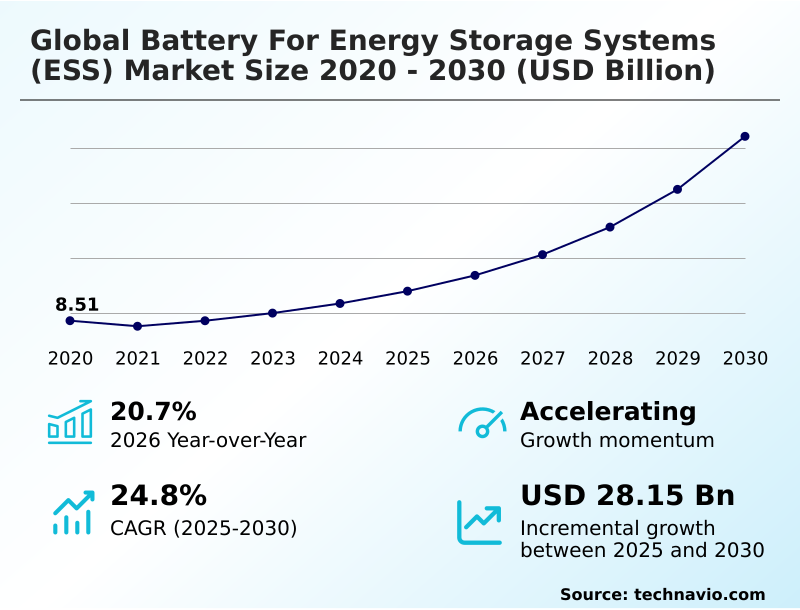

The battery for energy storage systems (ess) market size is valued to increase by USD 28.15 billion, at a CAGR of 24.8% from 2025 to 2030. Institutionalization of grid modernization and utility scale renewable integration will drive the battery for energy storage systems (ess) market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 52.7% growth during the forecast period.

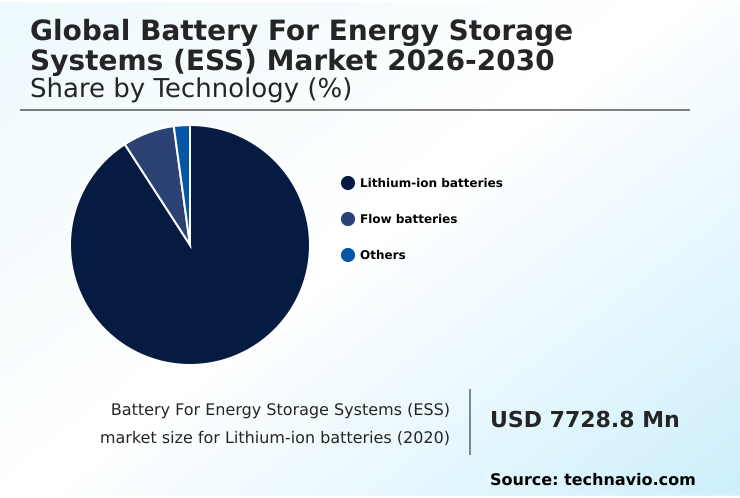

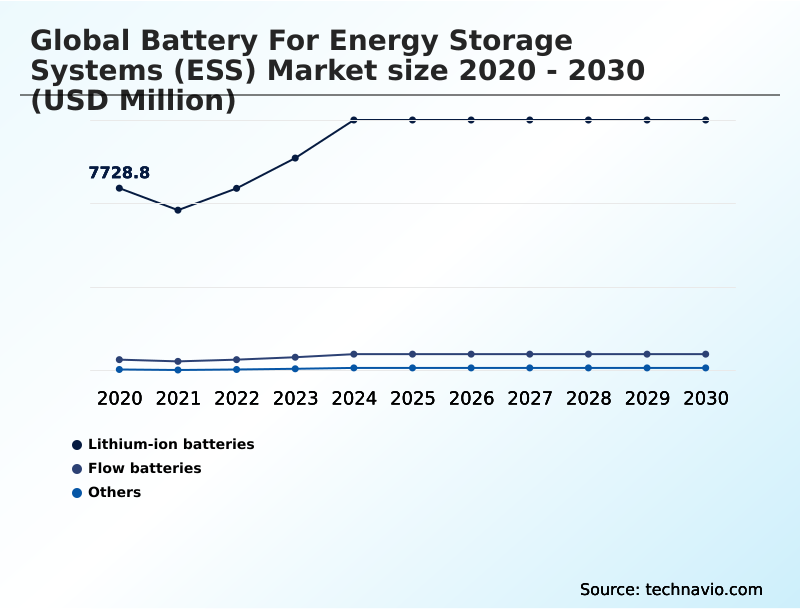

- By Technology - Lithium-ion batteries segment was valued at USD 10.57 billion in 2024

- By Connectivity - On-grid segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 33.52 billion

- Market Future Opportunities: USD 28.15 billion

- CAGR from 2025 to 2030 : 24.8%

Market Summary

- The Battery For Energy Storage Systems (ESS) Market is defined by a rapid technological evolution driven by global decarbonization mandates and the need for enhanced grid resilience. Key trends include the shift toward safer, more durable chemistries like lithium iron phosphate and the development of long-duration energy storage solutions, such as vanadium redox flow battery systems, to support intermittent renewables.

- A primary driver is the institutionalization of grid modernization, compelling utilities to adopt battery systems for frequency regulation and peak shaving. However, the industry faces significant hurdles from a volatile critical mineral supply chain and persistent grid interconnection bottlenecks, which can delay projects and inflate costs.

- For instance, a utility provider deploying a large-scale solar project must integrate a BESS with advanced battery management systems to ensure grid frequency is maintained, thereby avoiding both costly transmission upgrades and penalties for grid destabilization.

- The advancement of AI-driven battery optimization and zero-capex energy storage models are creating new opportunities for commercial and industrial users, further expanding market applications beyond traditional utility-scale installations and enhancing mission-critical power reliability.

What will be the Size of the Battery For Energy Storage Systems (ESS) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Battery For Energy Storage Systems (ESS) Market Segmented?

The battery for energy storage systems (ess) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Technology

- Lithium-ion batteries

- Flow batteries

- Others

- Connectivity

- On-grid

- Off-grid

- Ownership

- Utility owned

- Third-party owned

- Customer owned

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Technology Insights

The lithium-ion batteries segment is estimated to witness significant growth during the forecast period.

Lithium-ion batteries, predominantly using lithium iron phosphate chemistry, continue to command the market due to their high energy density and mature manufacturing ecosystems. These electrochemical storage solutions are central to both utility-scale installations and behind-the-meter storage applications.

The technology’s value is enhanced by advanced battery management systems that optimize performance for services like frequency regulation and peak shaving, improving cycle life by up to 40% under ideal conditions.

The emphasis on grid modernization and demand-side flexibility is driving further innovation in modular storage designs.

While facing competition from emerging technologies, the established supply chain for lithium-ion and its integration with grid-forming inverters solidifies its current market position, especially as commercial and industrial users adopt these systems.

The Lithium-ion batteries segment was valued at USD 10.57 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 52.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Battery For Energy Storage Systems (ESS) Market Demand is Rising in APAC Get Free Sample

The market's geographic landscape is characterized by distinct regional drivers and growth trajectories. APAC is poised to contribute over 52% of the market's incremental growth, fueled by massive domestic manufacturing incentives and national decarbonization targets.

In this region, stand-alone configurations for microgrids are as critical as grid-tied storage for industrial hubs.

North America demonstrates a robust expansion, with its market projected to grow at a rate exceeding 25% annually, driven by investments in high-density data centers and grid modernization.

Europe prioritizes regulatory frameworks like carbon footprint labeling, promoting circular economy innovations and the use of non-flammable electrolytes.

The focus on energy sovereignty and vehicle-to-grid protocols is accelerating the deployment of advanced battery technologies across all major economic zones, addressing everything from energy-intensive desalination in the Middle East to transmission network constraints in mature grids.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the battery for energy storage systems market requires a granular understanding of diverse operational scenarios. For instance, evaluating the cost comparison of lithium-ion vs flow batteries is crucial; while the former is prevalent, the latter offers advantages for long-duration storage in grid stability applications.

- As enterprises deploy battery energy storage for AI data centers, they must consider not just cost but also the protocols for managing thermal runaway in containerized battery systems. The role of long-duration storage in grid stability is a frequent topic, especially when planning to integrate BESS with intermittent renewable sources.

- Meanwhile, regulatory compliance for battery recycling programs and navigating grid interconnection queue delays are significant operational hurdles. Businesses are exploring behind-the-meter storage for commercial peak shaving and leveraging second-life EV batteries for stationary storage to improve ROI. Understanding the impact of the mineral supply chain on BESS costs and exploring financing models for zero-capex energy storage are vital.

- Furthermore, optimizing ROI with AI-driven energy arbitrage and addressing vehicle-to-grid integration challenges and opportunities define the competitive frontier. Advanced diagnostics for predicting battery degradation are becoming standard, with systems in remote mining operations showing 20% better predictive accuracy than previous-generation models.

What are the key market drivers leading to the rise in the adoption of Battery For Energy Storage Systems (ESS) Industry?

- The institutionalization of grid modernization and the mandated integration of utility-scale renewables are key drivers propelling market expansion.

- Grid modernization and the institutionalization of renewable energy mandates are the primary drivers propelling the market. Governments are investing heavily in decentralized smart grid infrastructure, making battery storage essential for managing grid frequency and providing voltage support.

- Utility-scale renewable integration has driven demand for large-scale BESS by over 200% in leading regions. The explosive growth of high-density data centers has created a new, high-value segment demanding uninterrupted power, which only on-site BESS can guarantee.

- Furthermore, the persistent decline in battery costs, particularly for lithium iron phosphate, has made BESS 25% more economically competitive than traditional gas peaker plants for peak shaving and load shifting.

- This economic viability, coupled with strong policy support, ensures a robust growth trajectory for both front-of-the-meter assets and distributed energy resources.

What are the market trends shaping the Battery For Energy Storage Systems (ESS) Industry?

- The industrialization of AI-driven battery optimization is an emerging market trend. This involves leveraging advanced algorithms to enhance performance, predict degradation, and extend operational lifecycles.

- A primary trend is the rapid industrialization of AI-driven battery optimization, which leverages sophisticated algorithms for predictive maintenance and enhanced performance. This move toward intelligent systems is enabling more effective wholesale market participation and firm power capacity. For example, AI-driven platforms can increase energy arbitrage revenue by over 20% by predicting price fluctuations with greater accuracy.

- Concurrently, the evolution toward a diversified chemistry portfolio is accelerating, with solid-state electrolytes and sodium-ion battery chemistries gaining traction. This shift addresses the critical mineral supply chain vulnerabilities associated with nickel manganese cobalt, with new materials offering improved thermal regulation and longer cycle life.

- These advancements are crucial for the expansion of long-duration energy storage and mission-critical power reliability, pushing the boundaries of what electrochemical storage solutions can achieve.

What challenges does the Battery For Energy Storage Systems (ESS) Industry face during its growth?

- Structural volatility within the critical mineral supply chain represents a significant challenge impacting industry growth and project economics.

- The market's growth is tempered by significant structural challenges, primarily the persistent grid connection bottlenecks and regulatory friction. In many developed markets, interconnection queues can delay project commissioning by an average of 36 months, rendering initial financial models obsolete.

- This is compounded by the structural volatility within critical mineral supply chains, where price spikes for materials like lithium and cobalt have inflated project capital expenditures by over 50% in a single year. Furthermore, the intensification of mandatory circularity and battery recycling compliance, such as the digital product passport in Europe, introduces significant administrative and logistical overhead.

- These challenges create a high-risk environment, particularly for developers of utility-scale installations who must navigate a complex web of technical standards, offtake agreements, and financial uncertainties.

Exclusive Technavio Analysis on Customer Landscape

The battery for energy storage systems (ess) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the battery for energy storage systems (ess) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Battery For Energy Storage Systems (ESS) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, battery for energy storage systems (ess) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

BYD Co. Ltd. - Offers grid-scale and distributed lithium iron phosphate-based storage solutions engineered for seamless renewable energy integration and enhanced grid stability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BYD Co. Ltd.

- Contemporary Amperex Ltd.

- EnerSys

- EOS Energy Enterprises Inc.

- ESS Tech Inc.

- EVE Energy Co. Ltd.

- Fluence Energy LLC

- Invinity Energy Systems plc

- LG Energy Solution Ltd.

- Northvolt AB

- Panasonic Holdings Corp.

- Powin Inc.

- Saft Groupe SAS

- Samsung SDI Co. Ltd.

- Sonnen GmbH

- Sungrow Power Supply Co. Ltd.

- Tesla Inc.

- VARTA AG

- Xiamen Hithium Energy Co. Ltd.

- Zhejiang Narada Power Source Co

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Battery for energy storage systems (ess) market

- In May, 2025, ABB officially launched its Battery Energy Storage Systems-as-a-Service, a zero-CapEx solution to accelerate clean energy adoption for industrial users.

- In April, 2025, Invinity Energy Systems received formal approval to install a 20.7-megawatt-hour vanadium redox flow battery system in the United Kingdom, the nation's largest of its kind.

- In January, 2025, Northvolt AB announced a strategic partnership with a major European automotive manufacturer to develop and scale vehicle-to-grid (V2G) technology, creating a 50 GWh virtual power plant pilot.

- In October, 2024, Fluence Energy LLC secured $500 million in a new funding round to expand its domestic manufacturing capacity for its latest generation of modular, grid-forming energy storage systems in the US.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Battery For Energy Storage Systems (ESS) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 296 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 24.8% |

| Market growth 2026-2030 | USD 28152.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 20.7% |

| Key countries | China, India, Japan, Australia, South Korea, Indonesia, US, Canada, Mexico, Germany, UK, Italy, France, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Chile and Argentina |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is advancing beyond simple hardware deployment toward integrated, software-defined energy assets. The adoption of advanced battery management systems and grid-forming inverters is now standard for utility-scale installations, ensuring ancillary services like frequency regulation and voltage support are reliably delivered.

- Chemistries are diversifying, with lithium iron phosphate for grid-tied storage, vanadium redox flow battery systems for long-duration needs, and emerging sodium-ion battery chemistries and zinc-based energy storage solutions targeting specific applications. In the boardroom, the focus has shifted to lifecycle value, where second-life utilization, the digital product passport, and circular economy principles directly impact ESG compliance and long-term asset valuation.

- For instance, firms deploying advanced state of charge monitoring report a 15% reduction in unscheduled maintenance. As distributed energy resources become more common, mastering grid interconnection protocols and power purchase agreements for behind-the-meter storage and stand-alone configurations is critical for maintaining a competitive edge and ensuring high round-trip efficiency.

What are the Key Data Covered in this Battery For Energy Storage Systems (ESS) Market Research and Growth Report?

-

What is the expected growth of the Battery For Energy Storage Systems (ESS) Market between 2026 and 2030?

-

USD 28.15 billion, at a CAGR of 24.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (Lithium-ion batteries, Flow batteries, and Others), Connectivity (On-grid, and Off-grid), Ownership (Utility owned, Third-party owned, and Customer owned) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Institutionalization of grid modernization and utility scale renewable integration, Structural volatility within critical mineral supply chain

-

-

Who are the major players in the Battery For Energy Storage Systems (ESS) Market?

-

BYD Co. Ltd., Contemporary Amperex Ltd., EnerSys, EOS Energy Enterprises Inc., ESS Tech Inc., EVE Energy Co. Ltd., Fluence Energy LLC, Invinity Energy Systems plc, LG Energy Solution Ltd., Northvolt AB, Panasonic Holdings Corp., Powin Inc., Saft Groupe SAS, Samsung SDI Co. Ltd., Sonnen GmbH, Sungrow Power Supply Co. Ltd., Tesla Inc., VARTA AG, Xiamen Hithium Energy Co. Ltd. and Zhejiang Narada Power Source Co

-

Market Research Insights

- The market's momentum is shaped by a confluence of financial innovation and technical necessity. The adoption of zero-capex energy storage models allows commercial and industrial users to gain mission-critical power reliability without significant initial investment, improving access to demand-side flexibility.

- This is critical as grid modernization initiatives advance, requiring automated grid management and wholesale market participation to manage transmission network constraints. AI-driven battery optimization is proven to enhance renewable energy load balancing and supports the formation of virtual power plants, achieving up to a 95% reduction in systemic grid failures in some deployments.

- Efforts to mitigate the volatile critical mineral supply chain through sustainable material sourcing, end-of-life battery recycling, and domestic manufacturing incentives are central to achieving national decarbonization targets and energy sovereignty. These strategies improve firm power capacity and enable a more resilient decentralized smart grid.

We can help! Our analysts can customize this battery for energy storage systems (ess) market research report to meet your requirements.

RIA -

RIA -